1. I recently had a chance to dig into @MakerDAO statistics for the past 1.5 years since SCD launch (@bennybitcoins pays attention to Maker day-to-day, so he's better for specific Q's)

Anyways, the conclusion of the data set is amazing. Maker is growing at a staggering pace 💯

Anyways, the conclusion of the data set is amazing. Maker is growing at a staggering pace 💯

2. Maker is a DAO, managed by MKR holders, built on Ethereum. It provides a credit factory that allows users to do 3 things:

- Trustlessly take out loans using crypto as collateral

- Instantly add leverage to their existing portfolios

- Produce stable cryptocurrencies called Dai

- Trustlessly take out loans using crypto as collateral

- Instantly add leverage to their existing portfolios

- Produce stable cryptocurrencies called Dai

3. Maker authorizes users to take out loans trustlessly by providing crypto (ETH) as collateral to a smart contract called a Collateralized Debt Position (CDP). The smart contract then issues Dai as debt. These debt instruments are entirely fungible & thus serve as the stablecoin

4. For a user seeking leverage, she can sell $100 worth of Dai on exchange for $100 worth of ETH (after putting $150 collateral ETH in Maker), allowing her to hold $250 of ETH. She now has a higher level of exposure to ETH price movement. She has $250 of Ether & owes $100 of debt

5. Dai is the stablecoin of the Maker system. Its value is pegged to USD, with tentative plans to eventually peg to a currency basket or a consumer price index. Upon locking collateral in a CDP contract, users can draw Dai coins as a loan. Borrowers have generated $323M of debt

6. Dai creators are likely not interested in stability, but rather the option to take out loans, which in some cases will be used to take on leverage. Even through the depths of a historic 2018 bear market, the Dai supply grew tremendously. Today, there is ~81.6M Dai outstanding

7. The stability fee (interest rate APR) has risen fast, now sitting at 17.5%. Many in the community have likened rate hikes to predatory lending. FWIW, I disagree. If you're technical enough to open a CDP, you should be paying attention to fee spikes, & close loans accordingly

8. Right now, there are a limited amount of Dai (100M) that can be minted bc of ETH’s “small” market capitalization (which backs the Dai). As can be seen in the chart below, 'only' 14 *active* funded CDP contracts have drawn >1M Dai. Another 92 CDPs have drawn between 100k-1M Dai

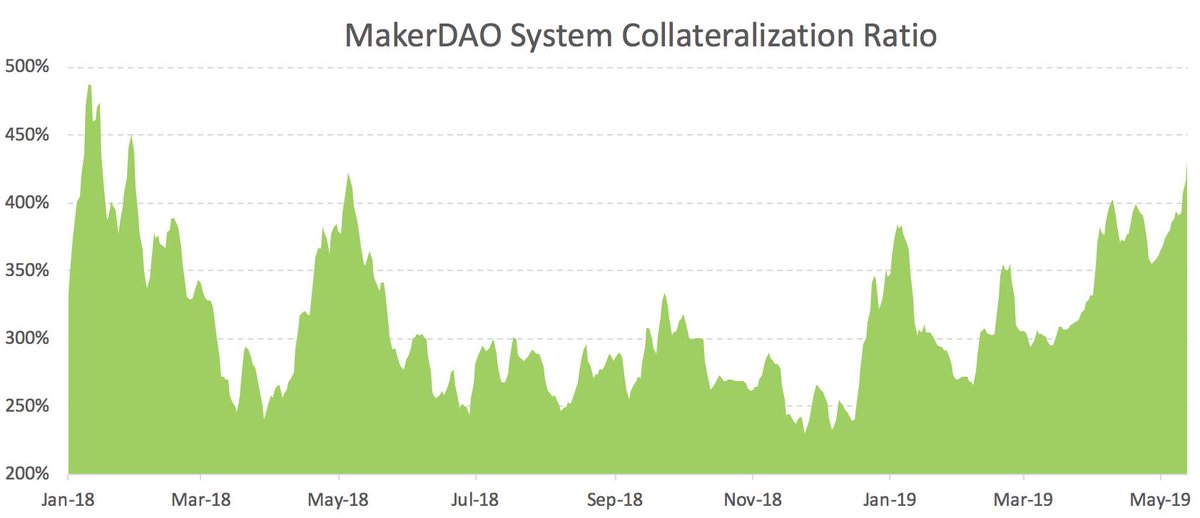

9. Amazingly, since Maker launched on Ethereum’s mainnet, Dai survived a 95% ETH price drawdown. The system remained fully collateralized as a whole the entire time Ether fell. Moving from SCD to MCD will mitigate the protocol impact of ETH idiosyncratically crashing (WBTC, OMG)

10. Even at today's prices with ETH being down 83% from its ATH of ~$1431, the Maker system would still stay solvent in a painful ETH drawdown. At $105 ETH, about 50% of Dai outstanding would be liquidated (assuming zero top ups which is unlikely anyways). TLDR: Dai's backed 🙂

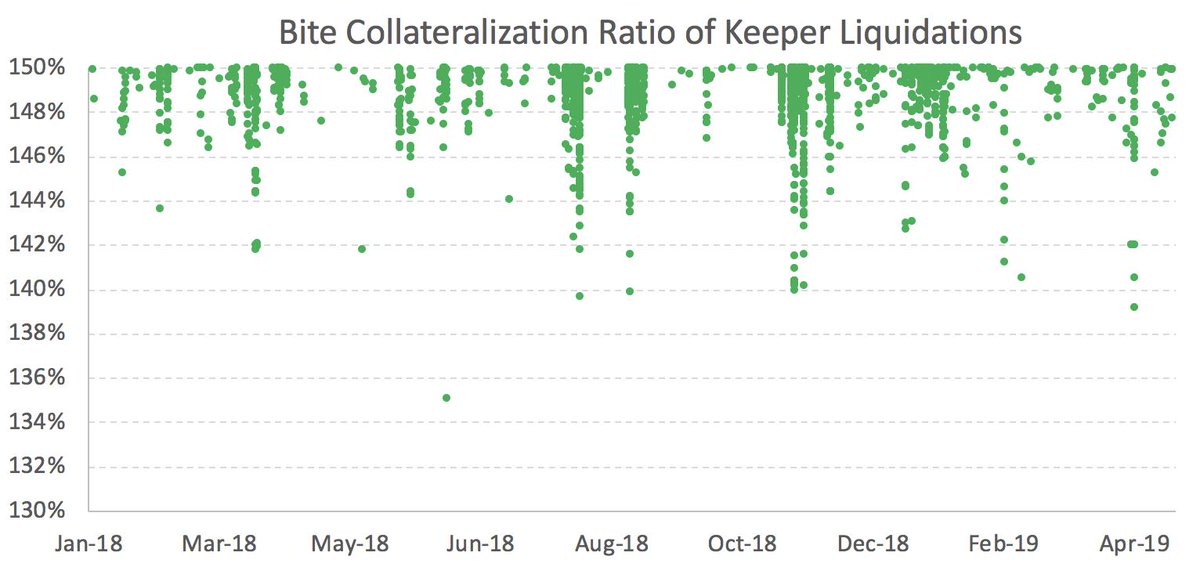

11. Impressively, even though Keeper'ing requires work which professional market makers may not have wanted to do early when arbitrage opportunities were too "small" to justify investment capital & effort ($1.4M total by March 1 per @placeholdervc), Keepers have bid PETH at ~150%

12. Creators incur liquidation penalties for under-collateralized CDPs (13%). In SCD, the penalty is paid to PETH holders via token burn. In MCD, MKR is bought & burned. In fact, liquid. penalties generated ~11x more "potential revenue" for MKR holders in 2018 than stability fees

13. MakerDAO employs a mechanism to liquidate CDPs that are at risk of eventually being underwater. Each separate asset used as collateral in MCD has a different set of risk parameters, voted on by MKR holders. Thus far, ~298k PETH has been liquidated. Yes network stayed whole :)

14. On top of liquidations, CDP participants can close out contracts fully or partially by repaying the debt (burning Dai + paying the stability fee) through a wipe transaction. As expected, since Dai's stability fee has increased throughout 2019, burning of Dai has accelerated

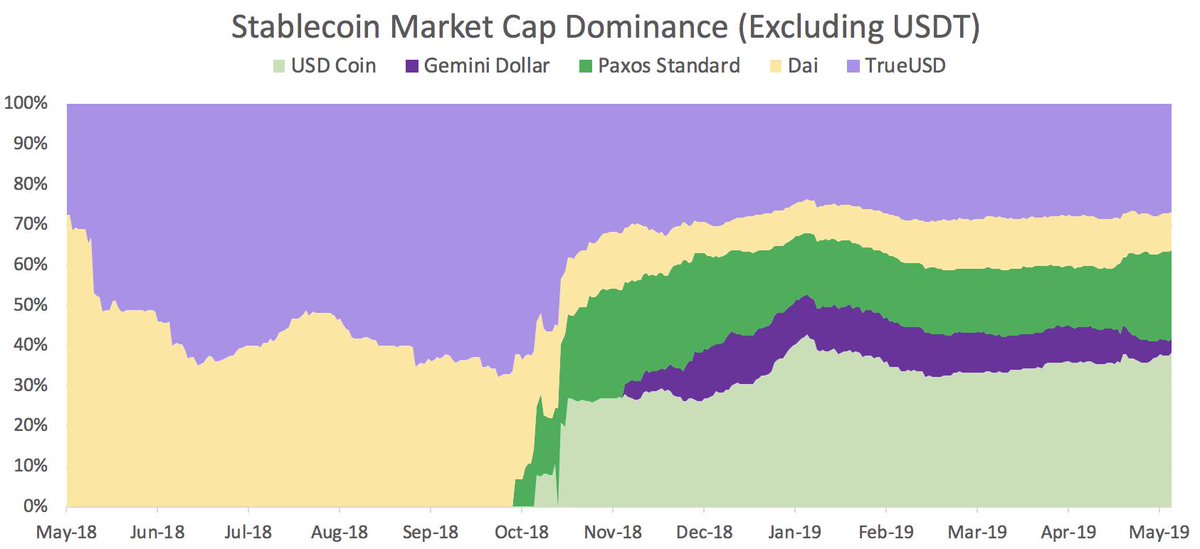

15. The stablecoin space is currently a massively crowded vertical. IOU-based stablecoins like Tether and USD Coin are currently Maker’s largest competitors. Still, even in the space of decentralized stablecoins, Maker has serious competition. List here: stablecoinindex.com/projects

16. Ultimately, the market will decide which stablecoin model wins. I predict centralized IOU models will be too risky to satisfy the use cases of a blockchain-based economy. Within decentralized stablecoins, my guess is the market will value Collateral-backed > Seignorage Shares

17. Dai leverages Global Settlement to offer holders downside protection. Seigniorage Shares OTOH offers a stablecoin that is not backed. The model is exposed since Soros Attacks could send the stablecoin to $0. Talk about an asymmetric short-selling opportunity for hedge funds🤔

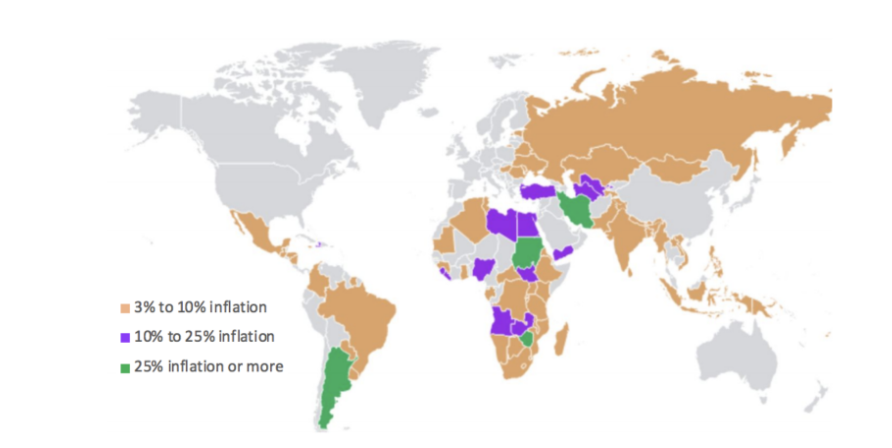

18. Stablecoins present the most likely case for enterprise & consumer adoption of crypto. They offer an effective hedge against inflation, opportunities for cheaper remittances, stable pairs, etc. Stablecoins also enable new use cases for dApps (those that require escrow/lockup)

19. Ethereum is currently poised to make best use of a stablecoin, since it has the largest ecosystem of DeFi & engineers in existence. Maker is a well-designed system that has the best chance of fulfilling the vision for a trustless Ethereum stablecoin media.consensys.net/the-100-projec…

20. Maker is intrinsically risky. While the MKR token has very large upside potential, the system is complex + experimental. Risks: 1. Black swan event in collateral (MCD mitigates); 2. Scalability bc Dai demand/supply curves don't intersect (DSR helps); 3. Governance; 4. Oracles

21. Trustless stablecoins may displace highly inflating government-issued currencies globally. Companies (e.g @BitsparkLtd) already leverage them for remittances. Maker’s dual token model provides the financial incentive for MKR holders to keep the system running correctly + well

22. Control of MKR tokens has proven to be centralized thus far. I trust the passionate group of early supporters (@a16z crypto, @placeholdervc, etc) who own lots of MKR will continue to guide the Maker system skillfully until it reaches critical mass & fully decentralizes

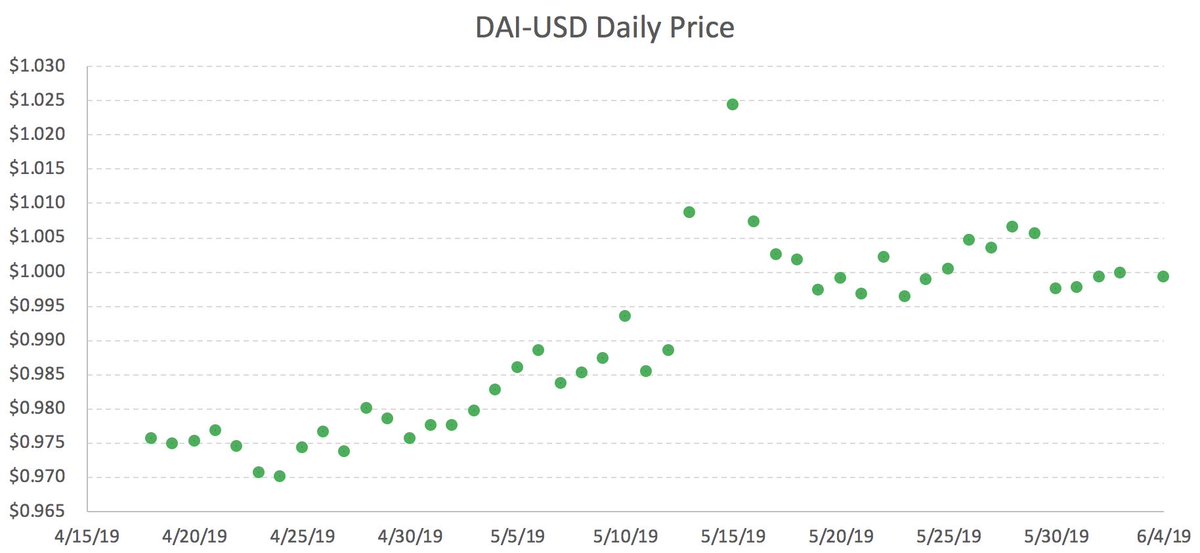

23. In today’s market climate, with hopeful bull market, a launch of Multi-Collateral Dai may coincide directly with large-scale demand for permissionless leverage. For these reasons I've never been more excited r.e. MKR. Congrats to @cyounessi1 + team for returning Dai peg to $1

24. Sources: @visavishesh descipher.io; mkr.tools ; @DaiEmbassy; @CoinMarketCap; @MakerScan; @IMFNews; @bit_kevin; @marcandu 2018 Revenue Analysis; daiprice.info

h/t @placeholdervc + @alexhevans Maker Network Overview for chart inspirations 😀

h/t @placeholdervc + @alexhevans Maker Network Overview for chart inspirations 😀

25. Side note: a couple of the graphs may be a few days old. Fell down the MakerDAO rabbit hole last week & compiled a lot of the data then. Numbers written out in the tweets themselves are up-to-date though