What essay or article have you read that has had a significant impact on how you think about business, markets, entrepreneurship and/or technology?

2/ Thanks for all the generous ideas on essays/articles. Here are the ones I'd personally put into the hall of fame

This one by @spolsky on cannibalizing your complement

joelonsoftware.com/2002/06/12/str…

This one by @spolsky on cannibalizing your complement

joelonsoftware.com/2002/06/12/str…

@spolsky 3/ This podcast with @bgurley and @patrick_oshag and its discussion of network effects

investorfieldguide.com/gurley/

investorfieldguide.com/gurley/

@spolsky @bgurley @patrick_oshag 4/ This one on Evolution & Revolution as Organizations Grow shared by a @CBinsights newsletter subscriber is great in framing the challenges of scaling

hbr.org/1998/05/evolut…

hbr.org/1998/05/evolut…

@spolsky @bgurley @patrick_oshag @CBinsights 5/ summarized the Evolution v Revolution article here

I do recommend reading the whole thing, however

https://twitter.com/asanwal/status/1137361726167486471

I do recommend reading the whole thing, however

@spolsky @bgurley @patrick_oshag @CBinsights 6/ Status-as-a-Service by @eugenewei is 🔥🔥

What makes it special is that it's long AF and detailed & still immensely readable

He's a special writer for the clarity he brings to topics while talking like a human the whole time

eugenewei.com/blog/2019/2/19…

What makes it special is that it's long AF and detailed & still immensely readable

He's a special writer for the clarity he brings to topics while talking like a human the whole time

eugenewei.com/blog/2019/2/19…

@spolsky @bgurley @patrick_oshag @CBinsights @eugenewei 7/ @pmarca with a great reminder abt markets

Reminded of this Warren Buffett maxim

"When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact."

pmarchive.com/guide_to_start…

Reminded of this Warren Buffett maxim

"When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact."

pmarchive.com/guide_to_start…

@spolsky @bgurley @patrick_oshag @CBinsights @eugenewei @pmarca 8/ "Management is (Still) Not Leadership"

very helpful for me as I def conflated the two prior

helped provide some clarity on where to seek help as we scale @CBinsights

hbr.org/2013/01/manage…

thx @nickseguin for flagging this one

very helpful for me as I def conflated the two prior

helped provide some clarity on where to seek help as we scale @CBinsights

hbr.org/2013/01/manage…

thx @nickseguin for flagging this one

@spolsky @bgurley @patrick_oshag @CBinsights @eugenewei @pmarca @nickseguin 9/ Great talk by Peter Kaufman on the Multidisciplinary Approach to Thinking

Discusses Einstein’s 5 ascending levels of cognitive prowess

5: smart

4: intelligent

3: brilliant

2: genius

1: simple

Simple transcends genius

latticeworkinvesting.com/category/peter…

Discusses Einstein’s 5 ascending levels of cognitive prowess

5: smart

4: intelligent

3: brilliant

2: genius

1: simple

Simple transcends genius

latticeworkinvesting.com/category/peter…

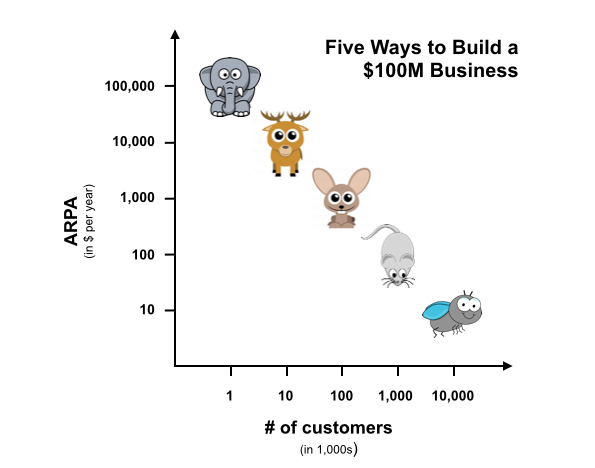

@spolsky @bgurley @patrick_oshag @CBinsights @eugenewei @pmarca @nickseguin 10/ Five ways to build a $100M biz by @chrija featuring his 🐁, 🦌, 🐘 framework was very clarifying in @CBinsights early days (esp in figuring out which markets not to attack)

Also, killer dataviz as you’ll see attached :)

christophjanz.blogspot.com/2014/10/five-w…

Also, killer dataviz as you’ll see attached :)

christophjanz.blogspot.com/2014/10/five-w…

@spolsky @bgurley @patrick_oshag @CBinsights @eugenewei @pmarca @nickseguin @chrija 11/ Going to use this to record concepts I've liked from various sources (to remind myself)

My favorite concept from @AnnieDuke's Thinking in Bets was that of "resulting" - our tendency to equate the quality of a decision with the quality of its outcome

Def been guilty of this

My favorite concept from @AnnieDuke's Thinking in Bets was that of "resulting" - our tendency to equate the quality of a decision with the quality of its outcome

Def been guilty of this

12/ "The 4 Myths of Bundling" by @shishirmehrotra

Very detailed, thoughtful analysis which challenged some preconceptions I had and also taught me a lot about the concept of bundling

coda.io/@shishir/four-…

Very detailed, thoughtful analysis which challenged some preconceptions I had and also taught me a lot about the concept of bundling

coda.io/@shishir/four-…

13/ "The 3 Sides of Risk" by @morganhousel

1. The odds you will get hit

2. The avg consequences of getting hit

3. The tail-end consequences of getting hit

It’s the third that’s hardest to learn, and can often only be learned through experience

collaborativefund.com/blog/the-three…

1. The odds you will get hit

2. The avg consequences of getting hit

3. The tail-end consequences of getting hit

It’s the third that’s hardest to learn, and can often only be learned through experience

collaborativefund.com/blog/the-three…

14/ “Fake activity is great for making yourself feel better, but lousy for actual results“

Loved the examples in this. So easy to confuse activity with progress.

scotthyoung.com/blog/2020/05/0…

Loved the examples in this. So easy to confuse activity with progress.

scotthyoung.com/blog/2020/05/0…

15/ Systems vs goals has been written about a lot but found this by @JamesClear to be among most concise & cogent

"goals are good for planning your progress and systems are good for actually making progress"

jamesclear.com/goals-systems

"goals are good for planning your progress and systems are good for actually making progress"

jamesclear.com/goals-systems

16/ “the better the startup is doing, the more chaos there is...is one of the few startup problems that growth doesn’t solve - in fact, it’s caused by growth.”

Fantastic practical & actionable essay on scaling from 50 to 500 by @DavidSacks

medium.com/craft-ventures…

Fantastic practical & actionable essay on scaling from 50 to 500 by @DavidSacks

medium.com/craft-ventures…

17/ this flies in the face of so much mgmt drivel today which is why it's so great

"Somebody would ask me if he could get back to me about something next week, and I would reply ‘how about tomorrow morning?"

linkedin.com/pulse/amp-up-f…

"Somebody would ask me if he could get back to me about something next week, and I would reply ‘how about tomorrow morning?"

linkedin.com/pulse/amp-up-f…

• • •

Missing some Tweet in this thread? You can try to

force a refresh