@jasonfurman Jason, this is wrong on several levels.

1) As @NathanTankus notes here (), the Fed is ultimately responsible for determining the distribution of long vs short-term govt liabilities in circulation, regardless of what Treasury issues in the first instance.

1) As @NathanTankus notes here (), the Fed is ultimately responsible for determining the distribution of long vs short-term govt liabilities in circulation, regardless of what Treasury issues in the first instance.

@jasonfurman @NathanTankus So financing deficits by issuing long-term bonds does not “lock in” low long-term rates for Tsy, since the Fed can and will always ‘sterilize’ that action by purchasing those bonds and replacing them with short-term reserves to meet its preferred maturity distribution curve,

@jasonfurman @NathanTankus which leaves us back in the exact same position from a consolidated govt perspective.

2) This also ignores the significant psychological and practical effects of transitioning from the current budget process to using overt monetary financing. Presently huge swaths of the public

2) This also ignores the significant psychological and practical effects of transitioning from the current budget process to using overt monetary financing. Presently huge swaths of the public

@jasonfurman @NathanTankus (wrongly) believe that “creating new money and using it to pay for things” is inherently more inflationary than debt-financing, and that in order for the Treasury to run a deficit it must, like a household or business, “borrow” from the lenders (ie the bond market, China) and

@jasonfurman @NathanTankus pay a market-rate of interest for doing so, in the process leaving a huge national debt for our grandkids that needs to be addressed at some point in the future to avoid “fiscal ruin”. By contrast, a system of overt monetary financing, in which interest rates are determined

@jasonfurman @NathanTankus exclusively by the Fed either paying interest on reserves or issuing its own securities (as Rep. Tlaib proposed in the recent #ABCAct proposal to #MintTheCoin, see here: tlaib.house.gov/sites/tlaib.ho…) completely dispels these myths and allows us to have a much more coherent & informed

@jasonfurman @NathanTankus public debate about the limits of fiscal policy and its relationship to monetary policy.

3) It is also wrong to presume that the Fed paying positive interest on its liabilities (reserves or FedSecurities) will have the same impact in a consolidated govt sense as the Tsy paying

3) It is also wrong to presume that the Fed paying positive interest on its liabilities (reserves or FedSecurities) will have the same impact in a consolidated govt sense as the Tsy paying

@jasonfurman @NathanTankus interest directly on its own liabilities. Currently, the Fed remits net profits minus operating expenses back to the Tsy on an ongoing basis, so paying a higher rate of IOR will reduce remittances, which will in turn affect the Treasury’s deficit position. However, this dynamic

@jasonfurman @NathanTankus has an intrinsic limit, which is when the Fed stops earning profit whatsoever, at which point any further losses are recorded indefinitely on the Fed’s balance sheet as a ‘deferred asset’, which means higher losses will have zero additional effect on the Treasury’s balance sheet

@jasonfurman @NathanTankus or deficit-level. This is significant, as it means that beyond a certain limit, any additional costs of maintaining a positive interest rate as part of monetary policy implementation will be born exclusively by the Fed, on its own balance sheet, with no additional impact on Tsy

@jasonfurman @NathanTankus from a consolidated govt perspective.

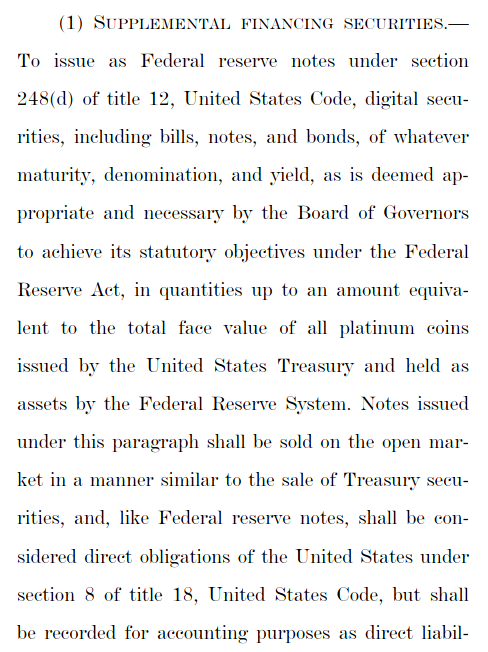

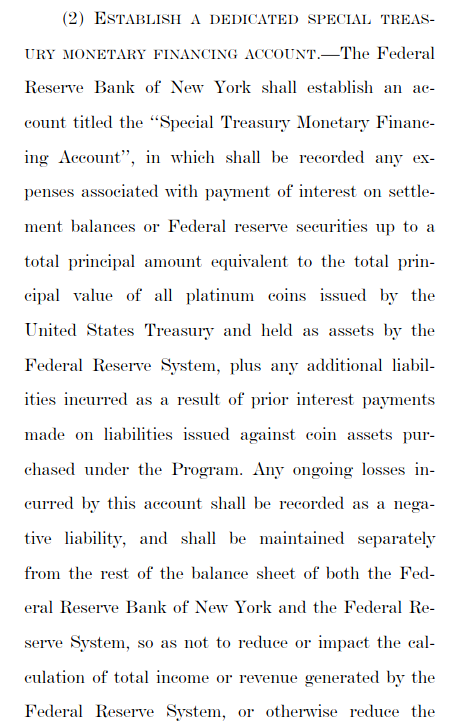

4) Alternatively, it’s entirely possible to change the existing accounting rules to make it so that any interest rate-related expenses are permanently absorbed solely on the Fed’s balance sheet, thereby avoiding any of the popular

4) Alternatively, it’s entirely possible to change the existing accounting rules to make it so that any interest rate-related expenses are permanently absorbed solely on the Fed’s balance sheet, thereby avoiding any of the popular

@jasonfurman @NathanTankus misunderstanding that the Treasury must “borrow and pay interest” when it runs deficits. This is, for example, exactly what we proposed in Rep. Tlaib’s #ABCAct, (see here: tlaib.house.gov/sites/tlaib.ho…) by creating a special ‘monetary financing account’ to record any interest payments

@jasonfurman @NathanTankus on liabilities issued by the Fed against non-interest-earning coins it acquired from the Tsy/Mint. This makes very clear that the Treasury can finance the deficit at zero interest, and any interest payments the Fed chooses to make as part of monetary policy are the responsibility

@jasonfurman @NathanTankus and decision of the Fed alone, and have nothing to do with “borrowing from private markets”.

5) Finally, this entire thread ignores the most basic fact, which is that interest rates paid on government liabilities – Treasury or Fed – are always and everywhere a policy choice,

5) Finally, this entire thread ignores the most basic fact, which is that interest rates paid on government liabilities – Treasury or Fed – are always and everywhere a policy choice,

@jasonfurman @NathanTankus not something that depends on external market conditions. As @StephanieKelton recently noted in the Financial Times (ft.com/content/53cb3f…), we should think very carefully about whether the government *choosing* to pay interest, to specific actors, serves public purpose, or

@jasonfurman @NathanTankus @StephanieKelton whether we could design a better way to give a risk-free return to pensioners and working families while simultaneously managing private investment/credit levels through other tools, such as direct/indirect credit regulation, as we argued here (ftalphaville.ft.com/2019/03/01/155…)

@jasonfurman @NathanTankus @StephanieKelton 6) All of which is to say that the idea overt monetary financing makes no difference relative to the current set up is wrong a) operationally, b) politically, and c) pschologically.

Someone in Jason’s position should know better than to make misleading claims like this.

/fin

Someone in Jason’s position should know better than to make misleading claims like this.

/fin