Remember when dubious home mortgages nearly destroyed the economy in 2008?

Well, a whistleblower contacted me a few months ago with a warning:He said commercial loans based on fraudulently inflated income data appeared to be on the brink of doing something similar.

Here’s how:

Well, a whistleblower contacted me a few months ago with a warning:He said commercial loans based on fraudulently inflated income data appeared to be on the brink of doing something similar.

Here’s how:

Some background:

Falsified paperwork for mortgages helped kick off a cascade of misery during the last financial crisis more than a decade ago. The market collapsed. Banks failed. People lost their homes in droves.

Falsified paperwork for mortgages helped kick off a cascade of misery during the last financial crisis more than a decade ago. The market collapsed. Banks failed. People lost their homes in droves.

After 2008, reforms by Congress and the SEC aimed to shine light on the process of bundling mortgages backed by assets like homes or hotels into bonds — to ensure such a calamity would never happen again.

The SEC passed rules requiring lenders to give investors more info on those assets, so they could gauge risk in pools of mortgages better, and make smarter decisions.

The focus was on the housing market then, but watchdogs condemned commercial lending, too, saying underwriting practices were lax and loans were made that shouldn’t have been.

(Commercial mortgage-backed securities = CMBS)

(Commercial mortgage-backed securities = CMBS)

Financial industry veteran John Flynn watched the crisis unfold back then.

He knew lots of the loans made right before the crash would come due 10 years later.

He knew lots of the loans made right before the crash would come due 10 years later.

Flynn figured property values that had been artificially puffed up would be lowered then, and someone would finally lose money.

He was wrong.

He was wrong.

Again and again, he said, properties with commercial mortgages based on inflated property values from the mid-2000s simply got new mortgages.

Flynn, who has a penchant for combing through dense financial disclosures, quickly spotted odd discrepancies:

Sometimes a property’s address, or name changed -- making it hard to find info on its earlier loan.

Sometimes a property’s address, or name changed -- making it hard to find info on its earlier loan.

Eventually, he realized the name changes often correlated with a more suspicious change:

Properties’ net operating income appeared higher in the new loan docs than it had in the old.

Even though both loans were referring to historical financials for the exact same years.

Properties’ net operating income appeared higher in the new loan docs than it had in the old.

Even though both loans were referring to historical financials for the exact same years.

Let’s slow down on this point:

It means an old loan reported a hotel made, say, $1 million in 2016... but a new loan said that the same hotel made $1.2 million in 2016.

Even that relatively small difference could qualify the property for a significantly larger loan.

It means an old loan reported a hotel made, say, $1 million in 2016... but a new loan said that the same hotel made $1.2 million in 2016.

Even that relatively small difference could qualify the property for a significantly larger loan.

Flynn was shocked. He eventually amassed documentation he said shows such manipulations in $150 billion worth of securities.

He filed a complaint with the SEC last year.

He filed a complaint with the SEC last year.

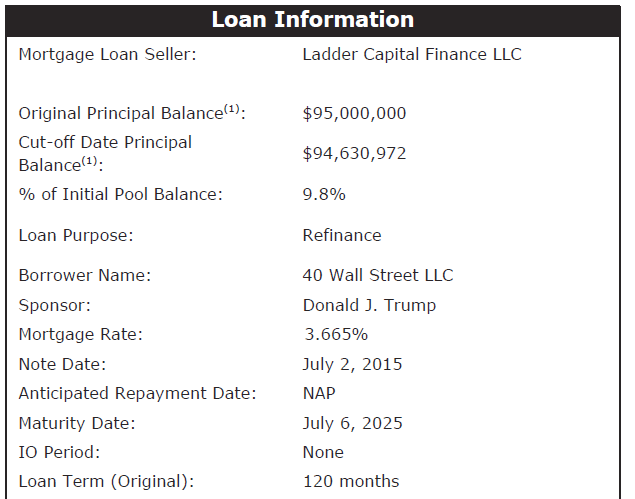

The complaint accused 21 lenders and servicers — including three of the biggest CMBS issuers, @DeutscheBank, @WellsFargo and Ladder Capital — of:

-inflating historical cash flows

-“deceptively and inaccurately” describing loan representations

-other misbehavior.

-inflating historical cash flows

-“deceptively and inaccurately” describing loan representations

-other misbehavior.

It doesn’t say which companies allegedly manipulated each specific number.

Spokespeople for Deutsche Bank and Wells Fargo declined to comment on the record. Ladder defended its actions as appropriate.

Spokespeople for Deutsche Bank and Wells Fargo declined to comment on the record. Ladder defended its actions as appropriate.

We dug into 6 loans from different pools and confirmed the discrepancies.

A hotel in San Diego’s profit for 2013 was 21% higher in new loan docs, than old ones.

An L.A. trailer park’s profit grew 28% from one filing to another, for the very same year.

(Response in next tweet)

A hotel in San Diego’s profit for 2013 was 21% higher in new loan docs, than old ones.

An L.A. trailer park’s profit grew 28% from one filing to another, for the very same year.

(Response in next tweet)

The San Diego hotel’s lender said it believed it was ok to alter historical financials by removing expenses that wouldn't continue in the future. Other lenders said the same.

The SEC declined to comment. But….its rules say financials should come from operating statements:

The SEC declined to comment. But….its rules say financials should come from operating statements:

The discrepancies are a bigger problem now that real estate is under incredible stress b/c of the virus. The Fed is propping up the commercial mortgage market.

“It’s a higher cliff from which they are falling,” Flynn told us. “So the loss severity is going to be greater.”

“It’s a higher cliff from which they are falling,” Flynn told us. “So the loss severity is going to be greater.”

This mess is bad for everyone: If mass defaults happen or fraud is found in loans backed by the Fed’s bailout program, experts told us, taxpayers could be on the hook.

propublica.org/article/whistl…

propublica.org/article/whistl…