1) Get a cup of coffee.

In this thread, I'm going to walk you through "The Kelly Criterion".

In this thread, I'm going to walk you through "The Kelly Criterion".

2) In 1956, John Kelly published a paper titled "A New Interpretation of Information Rate" in the Bell System Technical Journal.

3) In the paper, Kelly described a simple and elegant way for investors to strategically allocate capital in the face of uncertainty.

This is what is now known as the Kelly Criterion.

This is what is now known as the Kelly Criterion.

4) The approach is easiest to understand with an example.

I'll keep it as realistic as possible:

Imagine that you walk into an antique store one day. Due to the persistence of the salesman there, you buy an old lamp from him.

I'll keep it as realistic as possible:

Imagine that you walk into an antique store one day. Due to the persistence of the salesman there, you buy an old lamp from him.

5) You take the lamp home. You rub it. Out comes a genie. Nothing unusual.

6) The genie knows you like investing. So he sets up a @RobinhoodApp account for you, and finances it with a princely sum of ... wait for it ... $1.

He also enrolls you in Robinhood's fractional share trading program, but not in margin or options trading.

He also enrolls you in Robinhood's fractional share trading program, but not in margin or options trading.

7) Then the genie gives you a "stock tip": Aladdin Enterprises (NYSE: ALAD).

ALAD is a very special stock. Each month, the stock either exactly doubles or exactly halves in value. There's a 50/50 chance of either outcome, and no way to predict it in advance.

ALAD is a very special stock. Each month, the stock either exactly doubles or exactly halves in value. There's a 50/50 chance of either outcome, and no way to predict it in advance.

8) At the start of each month, you can rebalance your Robinhood portfolio between cash and ALAD however you like.

At the end of 20 years, all the stock in your account will be liquidated, the account will be closed, and its entire value will be given to you in cash.

At the end of 20 years, all the stock in your account will be liquidated, the account will be closed, and its entire value will be given to you in cash.

9) Your goal, of course, is to maximize the end-value of the Robinhood account (20 years from now).

The only thing within your control is the portfolio rebalancing at the start of each month.

So what should your rebalancing strategy be?

The only thing within your control is the portfolio rebalancing at the start of each month.

So what should your rebalancing strategy be?

10) Let's start by looking at the first month.

During this month, ALAD can either double or halve.

So, for every $1 you invest in ALAD at the beginning of the month, you'll have either $2 or $0.50 at the end.

On average, you'll have ($2 + $0.50)/2 = $1.25.

During this month, ALAD can either double or halve.

So, for every $1 you invest in ALAD at the beginning of the month, you'll have either $2 or $0.50 at the end.

On average, you'll have ($2 + $0.50)/2 = $1.25.

11) That's an average 25% monthly return on whatever money you invest in ALAD, vs 0% for whatever you keep in cash.

This is beginning to look like a no-brainer.

Clearly, the best way to proceed is to go "All In". Put your entire initial $1 in ALAD, and hold it for 20 yrs.

This is beginning to look like a no-brainer.

Clearly, the best way to proceed is to go "All In". Put your entire initial $1 in ALAD, and hold it for 20 yrs.

12) How will this "All In" strategy do over 20 years?

Best case: ALAD doubles every single month. That leaves you with many, many billions of dollars.

Worst case: ALAD gets halved every single month. That leaves you with an insignificant fraction of a penny.

Best case: ALAD doubles every single month. That leaves you with many, many billions of dollars.

Worst case: ALAD gets halved every single month. That leaves you with an insignificant fraction of a penny.

13) But neither the best case nor the worst case are remotely likely.

These are like tossing a coin 240 times (once a month for 20 years) and expecting to get heads (or tails) every single time.

So what does the *average* case look like?

These are like tossing a coin 240 times (once a month for 20 years) and expecting to get heads (or tails) every single time.

So what does the *average* case look like?

14) It turns out, for the "All In" ALAD strategy, the average case is not bad either.

Remember that on average, you make 25% per month? Compounded over 20 years, that turns your $1 into many billions.

So, in all likelihood, you'll make out like a bandit, right?

Not so fast.

Remember that on average, you make 25% per month? Compounded over 20 years, that turns your $1 into many billions.

So, in all likelihood, you'll make out like a bandit, right?

Not so fast.

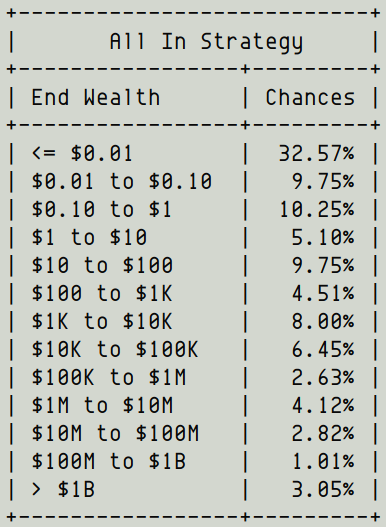

15) Here's a table showing various "wealth brackets", and your chances of ending up in each one at the end of 20 years if you followed the "All In" strategy:

16) As you can see, there's more than a 50% chance that you'll end up with less than $1 at the end of 20 years.

And a 67.4% chance that you'll end up with less than $100.

And only a 3% chance that you'll end up a billionaire.

And a 67.4% chance that you'll end up with less than $100.

And only a 3% chance that you'll end up a billionaire.

17) But how's that possible?

It's because outliers skew the average.

The billion dollar plus outcomes are so good that they lift up the entire average.

Kind of like one winning lottery ticket compensating for thousands of duds.

It's because outliers skew the average.

The billion dollar plus outcomes are so good that they lift up the entire average.

Kind of like one winning lottery ticket compensating for thousands of duds.

18) When you think about it, the *most likely* outcome is that ALAD doubles in some months and gets halved in others.

These doublings and halvings cancel each other, leaving you with roughly the same $1 you started with.

These doublings and halvings cancel each other, leaving you with roughly the same $1 you started with.

19) Key lesson: the *most likely* outcome can be dramatically different from the *average* outcome.

*Most likely* outcomes are not swayed by outliers. *Averages* are.

In this case, you will *most likely* end up with just $1. But *on average*, you expect to end up with billions.

*Most likely* outcomes are not swayed by outliers. *Averages* are.

In this case, you will *most likely* end up with just $1. But *on average*, you expect to end up with billions.

20) So, you need a way to escape this "lottery ticket" situation.

You need a strategy that maybe gives up some of the unlikely billions in potential upside, but buys you a very good chance of turning that $1 into $100K or $1M.

That's the genius of Kelly. He found that strategy.

You need a strategy that maybe gives up some of the unlikely billions in potential upside, but buys you a very good chance of turning that $1 into $100K or $1M.

That's the genius of Kelly. He found that strategy.

21) For this situation, Kelly's strategy is wonderfully simple:

At the start of each month, rebalance your portfolio so that exactly half of it is in cash and the other half is in ALAD stock.

At the start of each month, rebalance your portfolio so that exactly half of it is in cash and the other half is in ALAD stock.

22) So, how does this "Kelly strategy" do in comparison to "All In"?

The difference is night and day.

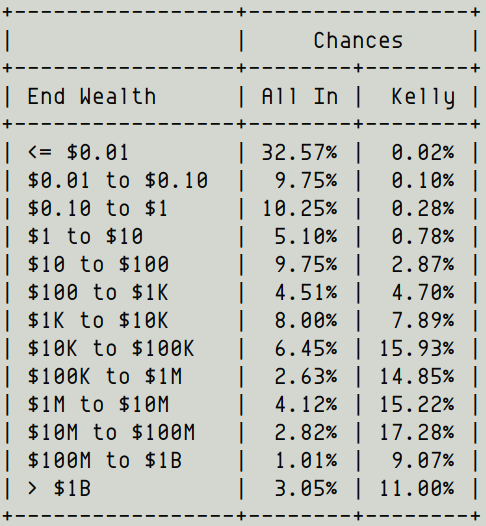

Just take a look at this table:

The difference is night and day.

Just take a look at this table:

23) With "All In", there was a 50+% chance of ending up with less than the original $1. Kelly reduces that to just a 0.4% chance.

Kelly also gives you a 50+% chance of ending up a millionaire, and a 11% chance of ending up a billionaire!

Kelly also gives you a 50+% chance of ending up a millionaire, and a 11% chance of ending up a billionaire!

24) Also, if you follow Kelly, the *most likely* outcome is that you'll end up with north of $1.3M.

The *average* outcome is still in the many billions, although Kelly does sacrifice some of the tail-end mega-billions.

The *average* outcome is still in the many billions, although Kelly does sacrifice some of the tail-end mega-billions.

25) But how did Kelly know to keep exactly 1/2 the portfolio in cash and 1/2 in stock? Why not 2/3 and 1/3? Or 3/5 and 2/5?

26) The answer is that Kelly built an entire mathematical theory to figure out the "best" possible strategy for a variety of situations like this.

When you apply the math to this particular problem, it so happens that you get 1/2 and 1/2 as the optimal strategy.

When you apply the math to this particular problem, it so happens that you get 1/2 and 1/2 as the optimal strategy.

27) Indeed, you can think of more complicated portfolio allocation situations.

What if ALAD could quadruple, double, stay the same, or halve?

What if there was more than 1 stock: Aladdin Enterprises and Jasmine Enterprises?

Kelly's theory is applicable to all this and more.

What if ALAD could quadruple, double, stay the same, or halve?

What if there was more than 1 stock: Aladdin Enterprises and Jasmine Enterprises?

Kelly's theory is applicable to all this and more.

28) I'll close this thread with a few references and resources:

"Fortune's Formula" by @WPoundstone is an excellent non-technical book that covers the Kelly Criterion in some detail.

amazon.com/Fortunes-Formu…

"Fortune's Formula" by @WPoundstone is an excellent non-technical book that covers the Kelly Criterion in some detail.

amazon.com/Fortunes-Formu…

29) "The Dhandho Investor" by @MohnishPabrai has many practical examples of how Mohnish has applied the Kelly Criterion to inform his own investment strategies.

amazon.com/The-Dhandho-In…

amazon.com/The-Dhandho-In…

30) "The Kelly Capital Growth Investment Criterion" by Leonard MacLean, @EdwardOThorp, and William Ziemba is a comprehensive collection of articles about the Kelly Criterion (for the mathematically inclined).

amazon.com/Kelly-Capital-…

amazon.com/Kelly-Capital-…

31) And of course, there's Kelly's original paper. You can read it in full here:

turtletrader.com/kelly.pdf

turtletrader.com/kelly.pdf

32) This thread on ergodicity by @borrowed_ideas is also pretty good; it contains some related ideas on probabilistic thinking, and was one of the inspirations behind my deciding to write this thread.

33) And speaking of ergodicity, @ole_b_peters has some good lecture notes that he's made available for free. His blog and Twitter feed are also pretty good.

…godicityeconomics.files.wordpress.com/2018/06/ergodi…

…godicityeconomics.files.wordpress.com/2018/06/ergodi…

34) If you're still with me, congrats! You have more persistence than most!

/End

/End

A1) Hey, what do you know?

Turns out there’s actually some interest in the core mathematical theory behind the Kelly Criterion.

So, with a shout out to @borrowed_ideas who encouraged me to include this, here’s an appendix to the tweetstorm that gets into the math.

Turns out there’s actually some interest in the core mathematical theory behind the Kelly Criterion.

So, with a shout out to @borrowed_ideas who encouraged me to include this, here’s an appendix to the tweetstorm that gets into the math.

A2) The key mathematical idea that Kelly had was:

Instead of maximizing the wealth you expect to have at the end of each round, maximize the logarithm of this wealth.

Instead of maximizing the wealth you expect to have at the end of each round, maximize the logarithm of this wealth.

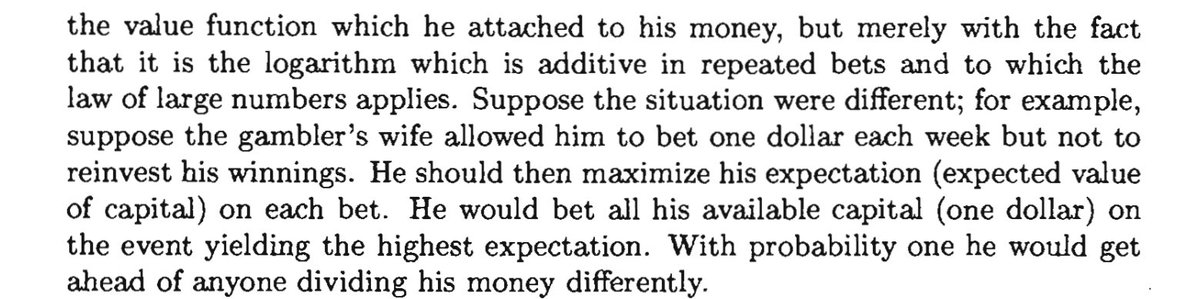

A3) Why logarithm?

It’s a bit involved. I’ll let Kelly take this one:

It’s a bit involved. I’ll let Kelly take this one:

A4) Let’s look at the “cash + ALAD” portfolio rebalancing problem from this angle.

At the start of a particular month, suppose our portfolio is worth $X. We divide this into two fractions: $f*X and $(1-f)*X.

We put $f*X in ALAD and keep $(1-f)*X in cash.

At the start of a particular month, suppose our portfolio is worth $X. We divide this into two fractions: $f*X and $(1-f)*X.

We put $f*X in ALAD and keep $(1-f)*X in cash.

A5) What happens one month later?

If we’re lucky, the ALAD part of our portfolio would have doubled. So the whole portfolio will be worth $f*X*2 + $(1-f)*X.

But if we’re unlucky, the ALAD part would have halved, leaving us with $f*X/2 + $(1-f)*X.

If we’re lucky, the ALAD part of our portfolio would have doubled. So the whole portfolio will be worth $f*X*2 + $(1-f)*X.

But if we’re unlucky, the ALAD part would have halved, leaving us with $f*X/2 + $(1-f)*X.

A6) This simplifies to:

Lucky case: $X*(1+f)

Unlucky case: $X*(1-f/2)

Lucky case: $X*(1+f)

Unlucky case: $X*(1-f/2)

A7) Kelly suggests that we take the logarithm of this. So here goes:

Lucky case: log(X*(1+f))

Unlucky case: log(X*(1-f/2))

Lucky case: log(X*(1+f))

Unlucky case: log(X*(1-f/2))

A8) These cases are 50/50. Equally likely. So, on average, what’s the logarithm expected to be? It’s:

0.5*log(X*(1+f)) + 0.5*log(X*(1-f/2)),

which simplifies to:

log(X) + 0.5*log(1 + f/2 - f^2/2).

0.5*log(X*(1+f)) + 0.5*log(X*(1-f/2)),

which simplifies to:

log(X) + 0.5*log(1 + f/2 - f^2/2).

A9) Kelly suggests we now choose f to maximize this.

That’s the same as maximizing 1 + f/2 - f^2/2, which happens to be:

9/2 - 2*(f - 1/2)^2.

Maximizing this means minimizing (f - 1/2)^2.

And that means choosing f = 1/2.

That’s the same as maximizing 1 + f/2 - f^2/2, which happens to be:

9/2 - 2*(f - 1/2)^2.

Maximizing this means minimizing (f - 1/2)^2.

And that means choosing f = 1/2.

A10) Remember that f was the fraction of our portfolio that we allocated to ALAD stock?

So choosing f=1/2 means we put half the portfolio in ALAD stock.

The other half, (1-f), goes to cash.

And that’s how you do the math behind the Kelly Criterion.

So choosing f=1/2 means we put half the portfolio in ALAD stock.

The other half, (1-f), goes to cash.

And that’s how you do the math behind the Kelly Criterion.

A11) For more complicated probabilistic outcomes, it’s usually a good idea to use a computer to figure out the Kelly strategy.

But the key idea is the same: maximize the expectation of the logarithm of your wealth at every step.

But the key idea is the same: maximize the expectation of the logarithm of your wealth at every step.

A12) If you got this far, you’re even more persistent than the readers who got to the end of the original thread. Kudos!

/End

/End