In our paper, @LHSummers and I argue that the *decline in worker power* is behind many of the major trends that have shaped the American economy in recent decades [1/N]

(WP out w/ @nberpubs and presented at @BrookingsEcon Spring 2020 BPEA. Ungated link scholar.harvard.edu/stansbury/rese…)

(WP out w/ @nberpubs and presented at @BrookingsEcon Spring 2020 BPEA. Ungated link scholar.harvard.edu/stansbury/rese…)

We argue that the decline in worker power in the U.S. economy can explain:

(1) the entirety of the decline in the labor share,

(2) much of the increase in corporate valuations, profitability, & measured markups,

(3) a large share of the fall in the NAIRU

[2/N]

(1) the entirety of the decline in the labor share,

(2) much of the increase in corporate valuations, profitability, & measured markups,

(3) a large share of the fall in the NAIRU

[2/N]

Of course, our focus on the decline of worker power is not new: we build on a long history of progressive institutionalist work in econ, sociology, and political science, which identifies the decline of worker power as one of the major structural trends in the U.S. economy [3/N]

But falling worker power has been *under-emphasized* as a cause of these trends in recent macro debates - relative to explanations based on globalization, tech change, or rising monopoly/monopsony power. The declining worker power explanation is –we think– more compelling [4/N]

How could declining worker power explain these trends?

If firms have some monopoly power & earn rents, worker power means workers receive a share of rents. As worker power falls, rents are redistributed from labor to capital, leading to ⬇️labor share, ⬆ profitability & Q [5/N]

If firms have some monopoly power & earn rents, worker power means workers receive a share of rents. As worker power falls, rents are redistributed from labor to capital, leading to ⬇️labor share, ⬆ profitability & Q [5/N]

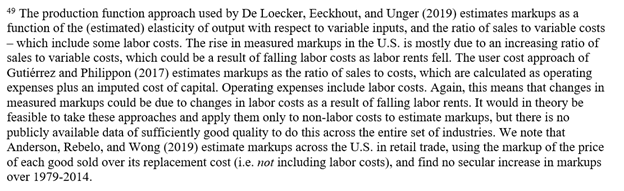

Falling worker power could also explain rising measured markups: commonly-used markup measures are based on some ratio of sales to costs, where costs includes labor costs. As rents to labor fall, measured labor costs fall - w/o any change in underlying product market power [6/N]

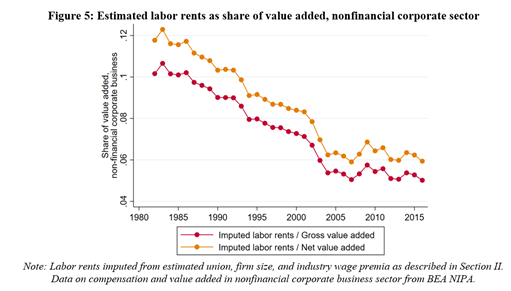

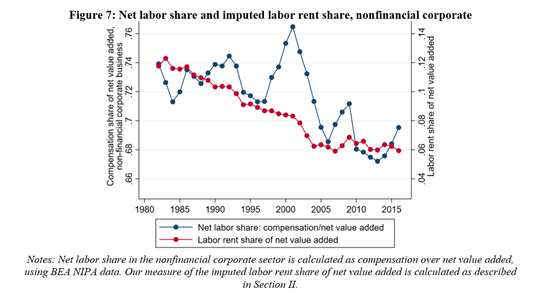

We roughly quantify the decline in labor rents, using estimates of wage premia for workers in unions, large firms, and high-paying industries.

We estimate that labor rents fell by half over 1982-2016: from 12% to 6% of net value added in the nonfinancial corporate sector [7/N]

We estimate that labor rents fell by half over 1982-2016: from 12% to 6% of net value added in the nonfinancial corporate sector [7/N]

The decline in labor rents we estimate – caused by the decline in worker power – is big enough to explain the *entire fall in the U.S. labor share* since the 1980s [8/N]

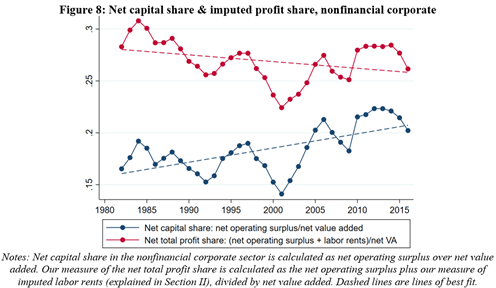

Note that labor rents, in our framework, come from firms’ profits. Some profits go to capital, some go to labor.

So while it looks like the aggregate profit share has risen, the *underlying* profit share (profits to capital + labor rents) may have stayed pretty constant [9/N]

So while it looks like the aggregate profit share has risen, the *underlying* profit share (profits to capital + labor rents) may have stayed pretty constant [9/N]

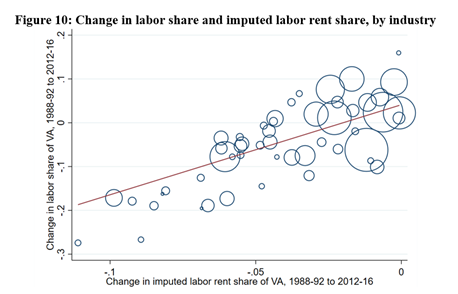

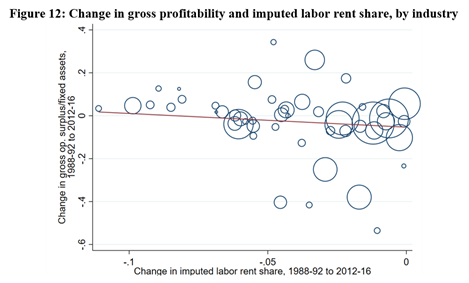

This holds up at the more disaggregated level too.

Industries and states with bigger declines in our measure of labor rents also saw bigger falls in their labor shares.

And industries with bigger falls in labor rents saw bigger increases in profitability and Tobin’s Q [10/N]

Industries and states with bigger declines in our measure of labor rents also saw bigger falls in their labor shares.

And industries with bigger falls in labor rents saw bigger increases in profitability and Tobin’s Q [10/N]

A third major macro trend has been the decline in the NAIRU: average unemployment had fallen substantially (until now...) even as inflation has stayed low and stable.

On the basis of most models, you'd expect a decline in worker power to lead to a fall in the NAIRU... [11/N]

On the basis of most models, you'd expect a decline in worker power to lead to a fall in the NAIRU... [11/N]

…And indeed, we find that states and industries with bigger falls in labor rents also had bigger falls in unemployment since the 1980s.

A simple extrapolation of the coefficients from the state-level analysis predicts a fall in the NAIRU of 0.75pp since the 1980s. [12/N]

A simple extrapolation of the coefficients from the state-level analysis predicts a fall in the NAIRU of 0.75pp since the 1980s. [12/N]

Finally, some argue that falling investment/fundamentals could have been caused by monopoly power.

But (1) real investment has fallen much less than nominal, and (2) investment relative to *underlying profits* (profits to capital + rents to labor) has fallen very little [13/N]

But (1) real investment has fallen much less than nominal, and (2) investment relative to *underlying profits* (profits to capital + rents to labor) has fallen very little [13/N]

At the start of this thread, we wrote that declining worker power had been under-emphasized relative to other explanations based on globalization, technological change, and monopoly or monopsony power.

What about those explanations? [14/N]

What about those explanations? [14/N]

While globalization & tech change are clearly important:

(1) the labor share decline has been bigger in US than other countries, & (2) trends in Q, profitability, markups are hard to explain under perfect comp, suggesting a role for country-specific non-competitive factors [15/N]

(1) the labor share decline has been bigger in US than other countries, & (2) trends in Q, profitability, markups are hard to explain under perfect comp, suggesting a role for country-specific non-competitive factors [15/N]

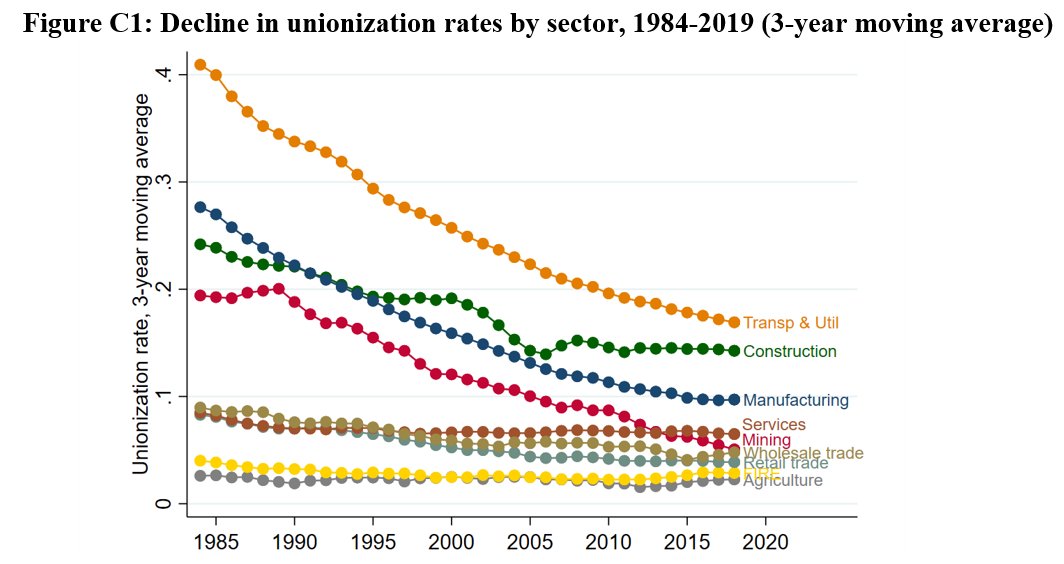

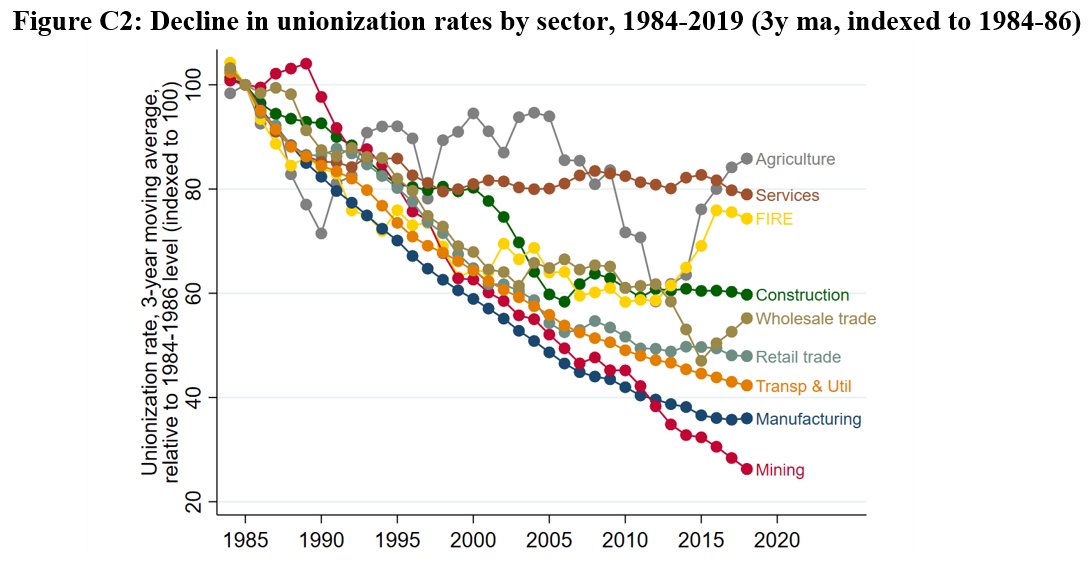

Ofc, unionization was affected by globalization and tech change (increasing elasticity of labor demand)- but this can't be the whole story. A similar proportional fall in unionization occurred across industries, & cross-country trends in unionization have been v different [16/N]

While monopoly and monopsony power matter in a static sense, and have likely⬆️in some markets:

(1) declining worker power can explain aggregate trends in labor share, Q, profitability, markups equally well,

[17/N]

*defining monopsony as arising from elasticity of LS to firm

(1) declining worker power can explain aggregate trends in labor share, Q, profitability, markups equally well,

[17/N]

*defining monopsony as arising from elasticity of LS to firm

(2) Declining worker power is more consistent w/ industry level evidence:

- Worker power has more explanatory power than concentration for labor share, profitability & Q

- Much of labor share⬇️was in manufacturing (where, w/ globalization,⬆️monopoly power seems unlikely)

[18/N]

- Worker power has more explanatory power than concentration for labor share, profitability & Q

- Much of labor share⬇️was in manufacturing (where, w/ globalization,⬆️monopoly power seems unlikely)

[18/N]

(3) Declining worker power is more consistent with the fall in the NAIRU,

(4) There is more direct evidence of a broad-based decline in worker power than of a large aggregate increase in monopoly or monopsony power

[19/N]

(4) There is more direct evidence of a broad-based decline in worker power than of a large aggregate increase in monopoly or monopsony power

[19/N]

(What do we actually mean by "decline in worker power"? Falling unionization & union power, falling real min wage, & increased shareholder empowerment & activism of shareholders have all disempowered workers in recent decades. Lots of work demonstrating and studying this [20/N])

What does this all mean?

The evidence is quite compelling that institutional changes, causing a decline in worker power, have been at the root of many of the major macro trends in the American economy over recent decades....

[21/N]

The evidence is quite compelling that institutional changes, causing a decline in worker power, have been at the root of many of the major macro trends in the American economy over recent decades....

[21/N]

... And if falling worker power has indeed been a major cause of rising inequality & low wage growth,

& if these problems can't be addressed by making markets more competitive,

it would strongly suggest that more should be done to promote workers' countervailing power. [/End]

& if these problems can't be addressed by making markets more competitive,

it would strongly suggest that more should be done to promote workers' countervailing power. [/End]