In case you missed it, yesterday Goldman published a research piece on inflation, gold, and bitcoin.

*deep breath*

Some thoughts...

*deep breath*

Some thoughts...

When I worked at Goldman the running joke amongst those around me was that I spent more time on bitcoin than the bonds I was supposed to be trading. 7 years later I didn't expect Goldman's attitude to have changed much. Even with that mindset going in, I was disappointed.

The report begins with the state of the U.S. economy and projections as to what it may look like in a post-COVID-19 world. In particular, the report emphasizes that inflation is unlikely to be something to worry about anytime soon. I tend to agree.

coindesk.com/how-i-learned-…

coindesk.com/how-i-learned-…

Goldman’s research then goes on to make a largely data-driven argument against investing in gold. Not only do we not have to worry about inflation, it says, but even if we did, gold would not be a great investment. Gold has not consistently outperformed inflation; equities have.

So far, so reasonable. I expected the Goldman research team to go on to make a similar data-driven argument about bitcoin: the fact that bitcoin, like gold, does not always behave as advertised.

Which, you know, bitcoin doesn't always act as an inflation hedge or a safe haven asset! This would have been a totally valid argument to make. Bitcoin's brief price history and volatile price action prevents us from being able to draw those correlations.

coinmetrics.io/correlation-ch…

coinmetrics.io/correlation-ch…

Rather than make a parallel argument to the one that they made against gold – which would have made for a compelling case – Goldman research launched into a series of non sequiturs about the objectionable traits of and dynamics around bitcoin.

Goldman did exactly what I find the smartest people often do when confronted with bitcoin: they abandoned all reason.

They ask whether bitcoin is a currency or an asset class. After defining the only features of a sovereign currency, they conclude that due to bitcoin’s failure to meet these criteria it does not qualify as any asset class at all.

This makes so little sense there is not even a name for this kind of logical fallacy.

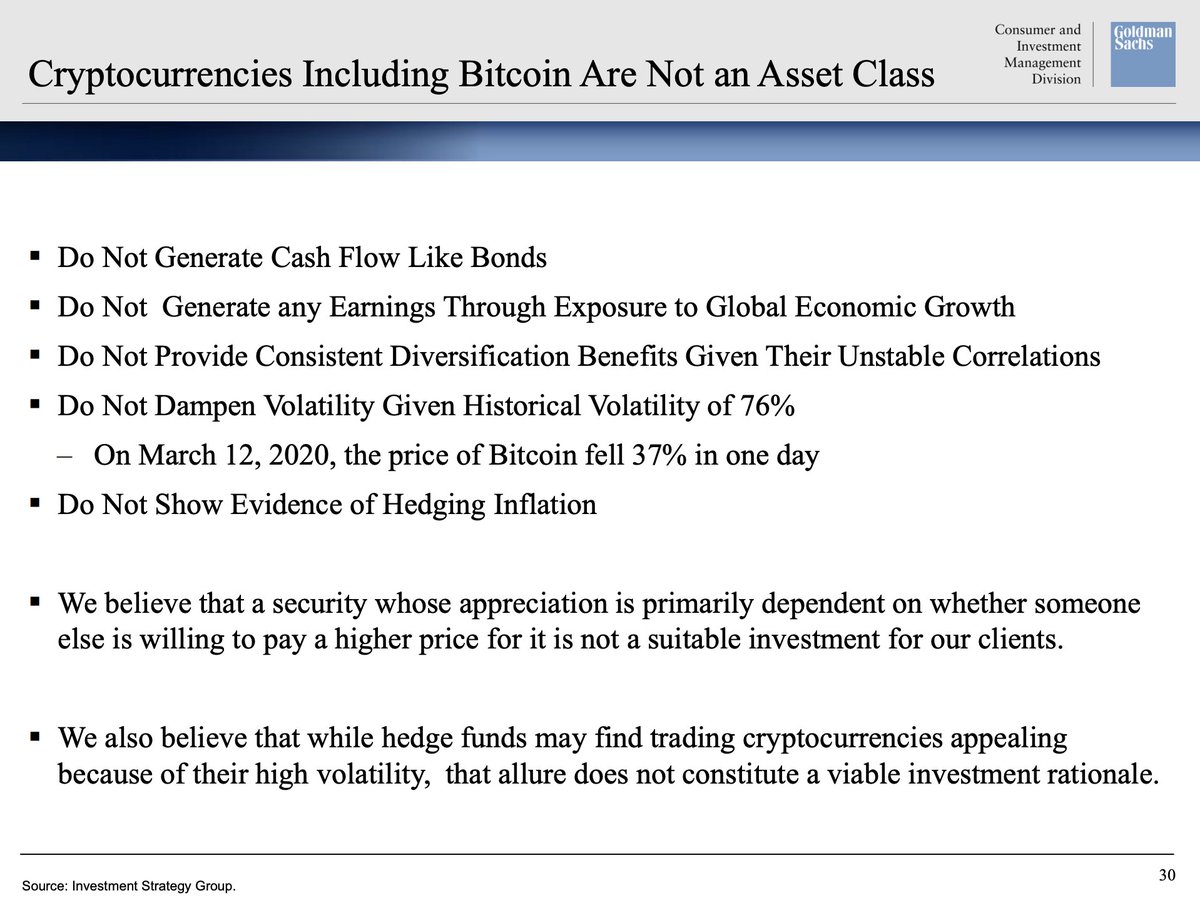

There is so much going on on this slide that I almost can't even.

How many asset classes don't generate cash flow like bonds (including many bonds themselves right now!)?

How many asset classes don't generate earnings?

Since when do asset classes demand stable correlations?

How many asset classes don't generate cash flow like bonds (including many bonds themselves right now!)?

How many asset classes don't generate earnings?

Since when do asset classes demand stable correlations?

This is the real coup de grace, however.

I hate to point out that, really, the fact that someone else is willing to pay a higher price for a given instrument is probably the only criteria necessary to know something is a suitable investment.

I hate to point out that, really, the fact that someone else is willing to pay a higher price for a given instrument is probably the only criteria necessary to know something is a suitable investment.

The reasons why someone else will be willing to pay that higher price are what is interesting and are what people generally look to the likes of Goldman Sachs research to explain and expound upon.

Goldman argues that cryptocurrencies are not a scarce resource due to the ability to fork into “nearly identical clones”, a shocking failure of research into the technical & cultural differences between the 3 examples that they offer (bitcoin, bitcoin cash & bitcoin sv). Come ON.

Goldman raises the possibility that cryptocurrency can be used for illicit activity to further discredit it – failing to address that the U.S. dollar, which is lauded for its strength earlier in the report, is the number one asset in the world used for illicit activity.

Finally, the report says the infrastructure around bitcoin and cryptocurrencies is relatively immature. There is much that is misrepresented on the slide illustrating this contention, including the omission of the option to self-custody assets uniquely offered by cryptocurrency.

For a company that prides itself on being a “technology firm,” the deck demonstrates an unwillingness to break out of traditional ways of thinking and instead look toward the possibilities opened up by bitcoin.

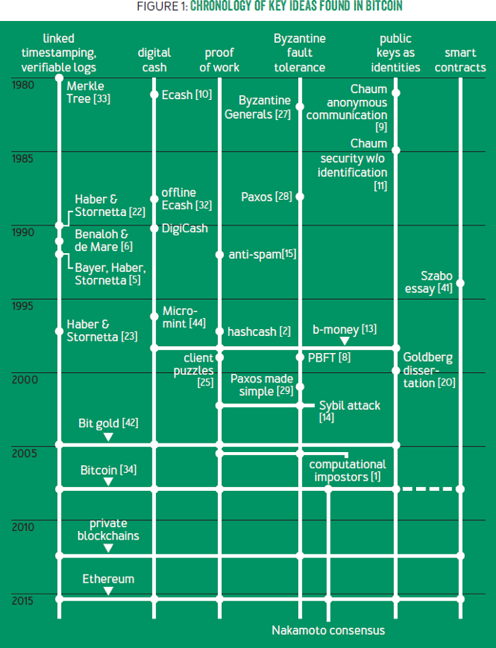

digital.hbs.edu/platform-digit…

digital.hbs.edu/platform-digit…

It would be easy to blame Goldman’s poor arguments against bitcoin on intellectual laziness or a certain strain of stuck-in-the-past thinking. If there is one thing I know from having worked there, however, it is that Goldman Sachs is neither lazy nor slow on the uptake.

Rather, I would posit, the weakness of Goldman’s thesis around bitcoin is due primarily to the weakness of the industry around bitcoin in articulating the defining attributes and uses of this paradigm-shifting technology.

coindesk.com/what-goldman-g…

coindesk.com/what-goldman-g…

One need only look as far as the industry’s recent failed attempts to sell J.K. Rowling on the value proposition of bitcoin to know that we need to start finding better ways of communicating.

If we want the likes of Goldman Sachs to buy into bitcoin, or if we even just want it to be able to make coherent arguments as to why not to buy into bitcoin, then we as an industry ought to look at the coherence of our own arguments first.

coindesk.com/what-goldman-g…

coindesk.com/what-goldman-g…