MSME - Facts, Reforms & Current Situation - A Thread

According to government numbers, there were about 65 million plus MSME units accounting for about 28% of the GDP and 30% of India’s labour force.

As report by TransUnion CIBIL- SIDBI of April, the total on-balance sheet commercial lending exposure in India stood at ₹64.45 lakh crores as of January 2020 compared to ₹64.04 lakh crores in December 2019. MSME Segment is at ₹17.75 lakh crore credit exposure as of Jan2020.

Government move of 3 lakh crore guaranteed loan to MSME is a good move as it will be amortized over 4 years. More such moves creatively and non stress balance sheet ones should be done from these angle where lender and borrower can survive and benefit well.

History tells increase in decade about such govt guarantee schemes. But current 3 lakh crore is 10 times the last year.

Though in case someone defaults, a 30-day review period begins after a borrower defaults on his repayments. However, the government has recently said there will be no fresh insolvency cases for up to a year now, a move that bankers have said will disrupt recoveries.

There are options like recast , but procedures and rules if required should be modified in advance to protect from mishaps. At present, all debt recasts are downgraded to the non-performing asset (NPA) category and banks have requested RBI to relax this criterion.

Worried banks have started testing the moratorium book for stress. They are analysing borrowers based on past default, age, leverage, company profile (level of Covid impact), geography (green, orange, red or containment zone). These are opportunities for survey n analytics tech

State Bank of India Chairman Rajnish Kumar said that the bank has released ₹2,300 crore to 22,000 MSME loan accounts on a single day. As on 31 December 2019, SBI had an SME loan book of ₹2.78 lakh crore or 14% of the total loan book

Moratorium bank wise

SBI 23%

ICICI Bank 30%

Kotak 26%

Axis Bank 28%

Indus Ind 5%

bank of baroda 65%(13% of its corporate loan)

Federal bank35%

SBI 23%

ICICI Bank 30%

Kotak 26%

Axis Bank 28%

Indus Ind 5%

bank of baroda 65%(13% of its corporate loan)

Federal bank35%

Outstanding term loan book was Rs 59.52 lakh crore on December 31, 2019. As per RBI estimates, Rs 38.68 lakh crore is under the six-month moratorium.

However, no provisioning is needed for a large part of the Rs 40 lakh crore moratorium book.

However, no provisioning is needed for a large part of the Rs 40 lakh crore moratorium book.

NBFC have more worries as cost of borrowing on liability is there with exposure to MSME working capital loans. Indian banks have lent ₹8.07 trillion to non-bank financiers as on 27 March, up 26% from the same period last year, showed data from the Reserve Bank.

Revised definition, combining mfg -service MSMEs investment less than Rs 1 cr and turnover under Rs 5 cr will be defined as micro while small will be categorized based on investment less than Rs 10 cr and TO under Rs 50 cr. Medium defined investment < Rs 20 cr turnover < 250 cr.

20000 crore package for distressed MSME debt subordinate and 50000 cr equity infusion through Fund of funds. Global tenders disallowed upto Rs 200 crore. These are reforms so far.

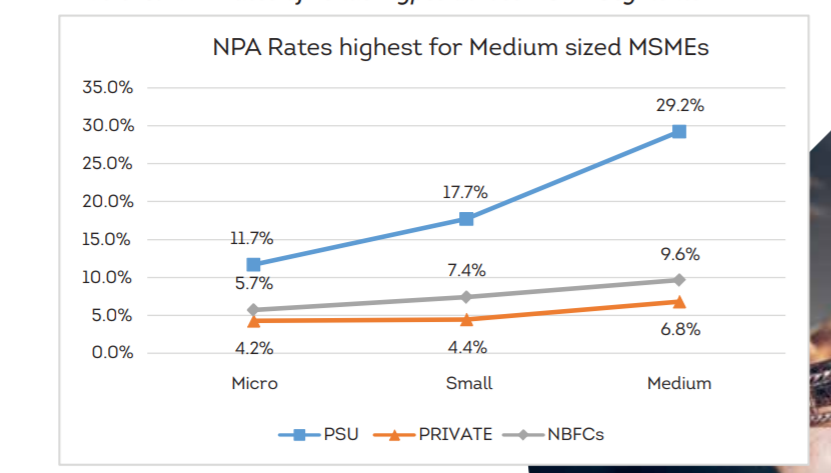

Situation on NPA though data bit old , remains quite similar before covid month.

By size wise credit growth was declining earlier due to diff issues. More focus on retail , higher growth in credit card and non secured personal loans, non secured consumer retail and less of business growth or expansion phases.

It looks like PSU banks may need recapitalization in future if defaults rise by December. Estimates are lenders need to raise $20 bn of capital, of which PSBs will require $13 bn, to strengthen buffers against potential loan defaults.

Indian Companies have raised a record 3.83 trillion rupees ($50.7 billion) via bonds so far this year, compared with 3.62 trillion rupees a year ago. Equity issuance has been more muted at 678 billion rupees.

We believe that if banks and NBFC raise funds even now, it would act better, via equity. offcouse not all be in position to do so but those who can , would be better off.

We also feel , worries on retail loan, housing loans and even corporate are over anticipated. outstanding loans amounting to 68,607 crores are from top 50 willful bank loan defaulters. Estimated FY21 corporate slippages alone at Rs 3.4 lakh crore.

We think that write backs can also happen in 2 year from now with recovery and paybacks.

Weightage wise Finance is now 33% of Nifty , way low from near 50%. Remembers time when IT was 50% in 2001 and then reduced to 25. Offcourse banks are backbone of system and Kotak , HDFC weight is way big enough in this 33. We think Finance sector will consolidate.

"In the long run, John Keynes is Dead... We live, face , improve and survive .. then Grow"

-Wealthyvia

-Wealthyvia

MSME share of lending by PSU PVT and NBFCs

share of NPA in MSME among lender types

Within MSME , Medium one are at higher side of NPAs