Notes on PEL AR 19-20 contd

In our last tweet thread on PEL, we covered the first part of AR19-20, i.e. the Strategic Overview

This thread is on the second part: Management Discussion & Analysis

@suru27 @finbloggers

In our last tweet thread on PEL, we covered the first part of AR19-20, i.e. the Strategic Overview

This thread is on the second part: Management Discussion & Analysis

@suru27 @finbloggers

1/

Equity: FY19: 27.2K Cr, FY20: 30.5K Cr

(+): Pref issue, Right Issue, Sale of Analytic

(-): DTA write-off, MAT credit reversal, ECL prov, Div, Stake sale in STFC & MTM losses.

Fin Service: Equity: 15.6K Cr, Debt: 40k Cr

Pharma: Equity: 4.5k Cr

Unallocated: 10.5 Cr

Equity: FY19: 27.2K Cr, FY20: 30.5K Cr

(+): Pref issue, Right Issue, Sale of Analytic

(-): DTA write-off, MAT credit reversal, ECL prov, Div, Stake sale in STFC & MTM losses.

Fin Service: Equity: 15.6K Cr, Debt: 40k Cr

Pharma: Equity: 4.5k Cr

Unallocated: 10.5 Cr

2/

Performance:

•Consol Rev grew 10% YoY (FS-8% growth, Pharma 13%)

•ECL increased from 324 CR to 1875 Cr due to COVID-19

•High borrowing cost led to inc in finance cost (from 4100 Cr to 5321 Cr)

•Depn from 401 Cr to 520 Cr.

•PAT down drastically from 1464 Cr to 21 Cr

Performance:

•Consol Rev grew 10% YoY (FS-8% growth, Pharma 13%)

•ECL increased from 324 CR to 1875 Cr due to COVID-19

•High borrowing cost led to inc in finance cost (from 4100 Cr to 5321 Cr)

•Depn from 401 Cr to 520 Cr.

•PAT down drastically from 1464 Cr to 21 Cr

3/

NBFC

•NBFCs were in liquidity stress due to rating downgrades & defaults post the IL&FS event

•Slowdown more pronounced in case of non-deposit taking NBFC.

•RBI & GOI measures had eased conditions to some extent.

•But due to COVID-19, the condition has got worse.

NBFC

•NBFCs were in liquidity stress due to rating downgrades & defaults post the IL&FS event

•Slowdown more pronounced in case of non-deposit taking NBFC.

•RBI & GOI measures had eased conditions to some extent.

•But due to COVID-19, the condition has got worse.

4/

NBFCs with:

•sufficient on-balance sheet liquidity

•access to long-term funding

•healthy provisioning

•a diversified loan portfolio &

•adequate capital buffers with low leverage

are relatively well placed in the current stage

NBFCs with:

•sufficient on-balance sheet liquidity

•access to long-term funding

•healthy provisioning

•a diversified loan portfolio &

•adequate capital buffers with low leverage

are relatively well placed in the current stage

5/

PEL’s position

•Improved CAR and deleveraging

•Reduce large single borrower

•Higher provisions due to COVID-19

•Adequate liquidity & increasing long term loans

•Reducing CP exposure

•Building a multi-product retail lending platform

•Building fund-based platform

PEL’s position

•Improved CAR and deleveraging

•Reduce large single borrower

•Higher provisions due to COVID-19

•Adequate liquidity & increasing long term loans

•Reducing CP exposure

•Building a multi-product retail lending platform

•Building fund-based platform

6/

RE: COVID Impact

A.Residential RE

•Sales through digital platforms

•Disc to boost sales.

•Focus on CF

B.Commercial RE

•WFH, the new norm

•Investments by global funds

C.Hospitality

•Adverse impact due to lockdowns

•Marquee brands relatively better positioned

RE: COVID Impact

A.Residential RE

•Sales through digital platforms

•Disc to boost sales.

•Focus on CF

B.Commercial RE

•WFH, the new norm

•Investments by global funds

C.Hospitality

•Adverse impact due to lockdowns

•Marquee brands relatively better positioned

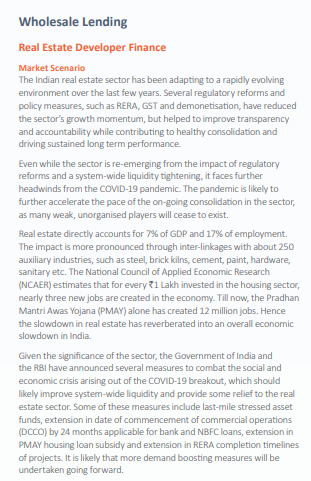

7/

PEL’s positioning in Wholesale Lending:

•Operational Performance

•Commercial RE

•Selectively tap superior ‘risk-reward’ opportunities in wholesale financing

•Granularisation of the developer financing loan book

PEL’s positioning in Wholesale Lending:

•Operational Performance

•Commercial RE

•Selectively tap superior ‘risk-reward’ opportunities in wholesale financing

•Granularisation of the developer financing loan book

8/

Corporate Lending

•Corporate Finance Group

•Emerging Corporate Lending

Corporate Lending

•Corporate Finance Group

•Emerging Corporate Lending

9/

Retail

•Low penetration (~15% of GDP), China: 66%&USA: 81%

•HF- a sizable portion for retail facing NBFCs

•Key providers of HF: banks- 57.8% & HFCs- 42.2%

•85% of HFC loans in top 5 players

•PEL aspires to grow Home loan book & build retail lending platform

Retail

•Low penetration (~15% of GDP), China: 66%&USA: 81%

•HF- a sizable portion for retail facing NBFCs

•Key providers of HF: banks- 57.8% & HFCs- 42.2%

•85% of HFC loans in top 5 players

•PEL aspires to grow Home loan book & build retail lending platform

10/

Asset Quality

•Review and governance mechanism

•GNPA and Risk Mitigation Actions

•Examples of mitigation actions taken during the year

•Details of stage-wise provisioning

Asset Quality

•Review and governance mechanism

•GNPA and Risk Mitigation Actions

•Examples of mitigation actions taken during the year

•Details of stage-wise provisioning

11/

•Borrowing Mix by type of Instrument

•Borrowing Mix by type of investor

•Avg cost of borrowing: 11.2%

•ALM Profile

•Key performance metrics

•Borrowing Mix by type of Instrument

•Borrowing Mix by type of investor

•Avg cost of borrowing: 11.2%

•ALM Profile

•Key performance metrics

12/

Pharma

•Contract Development and Manufacturing business (͞CDMO”)

•Complex Hospital Generics business (͞CHG”) business

•Consumer Healthcare business in India (͞CHD”).

Pharma

•Contract Development and Manufacturing business (͞CDMO”)

•Complex Hospital Generics business (͞CHG”) business

•Consumer Healthcare business in India (͞CHD”).

13/

Key Highlights

•Consistent long term track record of growth in Revenue & EBITDA

•Focus on Quality & Compliance

•Differentiated Business Model

•Integrated Model in CDMO

•Differentiated product portfolio of CHG

Key Highlights

•Consistent long term track record of growth in Revenue & EBITDA

•Focus on Quality & Compliance

•Differentiated Business Model

•Integrated Model in CDMO

•Differentiated product portfolio of CHG

14/

Performance of

•CDMO

•CHG

•CHD

Performance of

•CDMO

•CHG

•CHD

15/

Growth Drivers and Future Outlook in

•CDMO

•CHG

•CHD

Growth Drivers and Future Outlook in

•CDMO

•CHG

•CHD

16/

This is the end Part2 of notes on PEL AR 19-20

Management Discussion & Analysis

Stay tuned. We will be releasing Part 3 soon for your benefit.

End

This is the end Part2 of notes on PEL AR 19-20

Management Discussion & Analysis

Stay tuned. We will be releasing Part 3 soon for your benefit.

End