We didn't learn a whole lot about the Fed's forward guidance strategy aside from the fact that it will be related to the conclusion of the Fed's framework review. If the Fed needs some suggestions for how to proceed with state-contingent forward guidance

medium.com/@skanda_97974/…

medium.com/@skanda_97974/…

For those wondering, yes, these suggestions overlap with @employamerica's proposed #FloorGLI framework in that the goal is to achieve a baseline rate of employment and wage growth: medium.com/@skanda_97974/…

The Evans Rule had a number of flaws from which Sudiksha Joshi and I hope the Fed learns the right lessons...

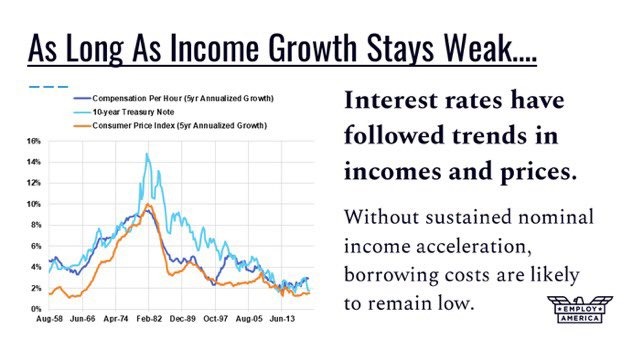

To start with, the Fed really should look beyond consumer price inflation if they want to escape the asymmetric costs posed by the zero lower bound...

To start with, the Fed really should look beyond consumer price inflation if they want to escape the asymmetric costs posed by the zero lower bound...

@darioperkins recently released a nice piece on the incoherence of economists' understanding of what guides inflation. This really shouldn't be a surprise if you're aware of how the inflation sausage is actually made....

blogs.tslombard.com/road-to-inflat…

blogs.tslombard.com/road-to-inflat…

As the BLS tries to capture quality-adjustments within price indices, the methodology evolves. But the components of headline/core inflation measures do not follow a single consistent methodology, nor does each component's methodology remain fixed through time....

The result is almost necessarily incoherent. About the most we can say about consumer price inflation is that over long time periods, it bears a loose correlation with nominal income growth (which makes sense since b/c nominal spending growth is necessarily correlated).

Unlike consumer price inflation, nominal wage growth actually does follow some meaningfully predictable patterns. @ernietedeschi and @ModeledBehavior have both documented the sensitivity of wage growth to the prime-age employment rate

We can say with some certainty that nominal wage growth is sensitive to some mix of labor utilization and the growth rate in economic activity. Price inflation OTOH is methodologically messy, slow to respond to economic dynamics, and not really the true objective of accommodation

To speak in terms of 'striving for more inflation' is to confuse the byproduct with the objective. Shifting the focus to wage growth can help clean up some of the Fed's communication nightmares.

Which gets us to our second recommendation: opt for a floor, not a ceiling.

The Evans Rule took a defensive approach to forward guidance but if the Fed wants to sustainably escape the trap of low nominal income growth and inflation, it ought to set an affirmative goal

The Evans Rule took a defensive approach to forward guidance but if the Fed wants to sustainably escape the trap of low nominal income growth and inflation, it ought to set an affirmative goal

Contrary to what FOMC hawks in 2012 were worried about, an inflation ceiling on its own did not lead to overshooting. And after 8 years of missing the Fed's self-adopted target, the systematic policy bias for below-target inflation is increasingly glaring.

Philly Fed president Patrick Harker is already moving in our proposed direction by suggesting the Fed not raise rates at least until inflation is back to the 2% target. The problem with this specific approach is in how easily it can be misinterpreted (byproduct vs objective)

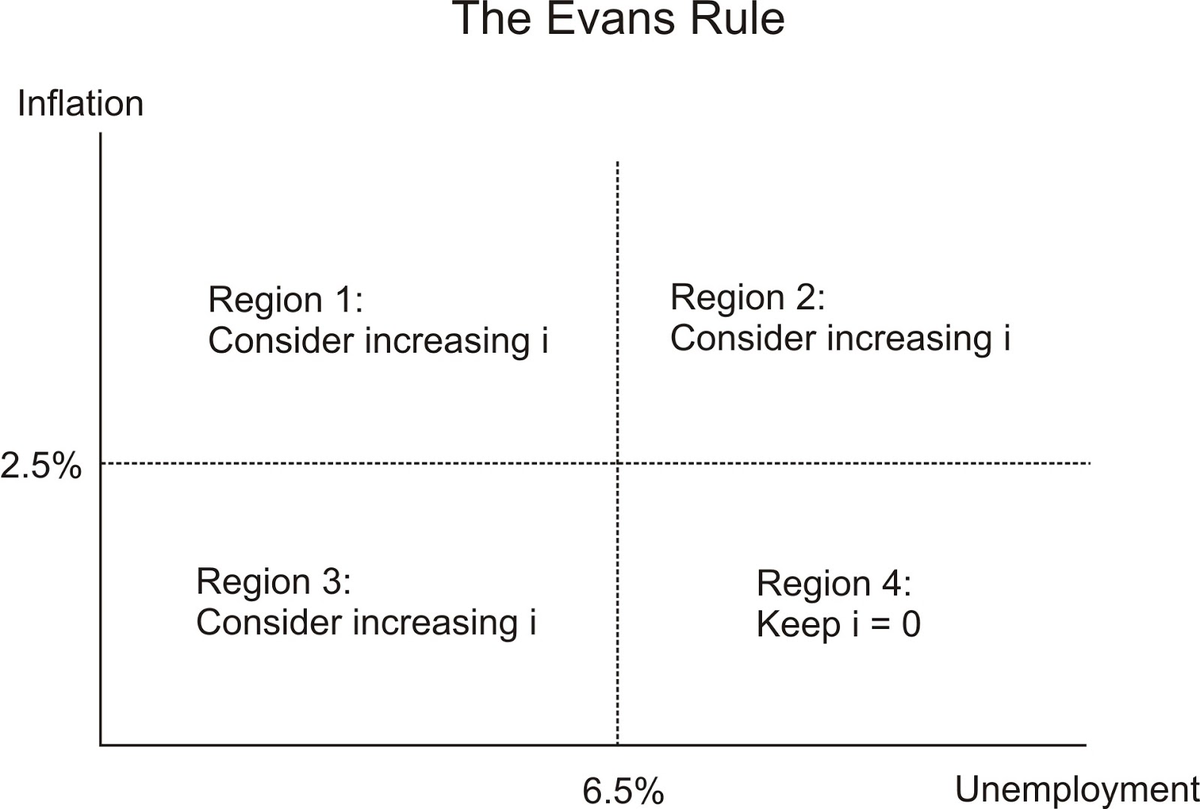

Our third proposed improvement: make the labor utilization threshold a necessary "level target" but not an individually sufficient condition for ending forward guidance. To see why, I'd start with this timely @dandolfa post andolfatto.blogspot.com/2012/12/the-ha…

One of the flaws with the Evans Rule that ultimately led to its premature conclusion was that unemployment rate crossing the 6.5% threshold alone meant the end of state-based forward guidance, even though inflation remained below target and wage growth stayed sluggish

Our solution is to make Regions 2 and 3 of @dandolfa's diagram more like Region 4. This was probably not politically feasible within the FOMC when the Evans Rule was first debated but it seems more feasible now given the evolution of the committee over the last 8 years

For the longest time, Fed officials have thought about labor utilization in terms of its alleged relevance to price inflation and wage growth. The Phillips Curve was supposed to imply that relatively high labor utilization would translate into faster inflation....

The latter years of this expansion give strong reason for skepticism. Historically low unemployment did not result in above-target inflation. The Phillips Curve is not a good rationale for retaining a labor utilization threshold, but there is a much better rationale: context.

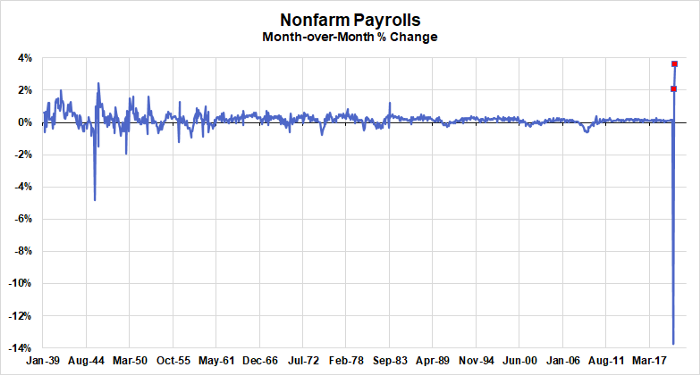

To see the value of using a labor utilization threshold, it helps to consider just how volatile the economic data has been over the past few months. Percentage change of any economic variable (employment, wages, output, prices) can easily mislead right now...see nonfarm payrolls

@Neil_Irwin's piece from back in May captured this point well: "In normal times, percentage change is a helpful guide to what’s happening in the economy. But these are not normal times."

nytimes.com/2020/05/19/ups…

nytimes.com/2020/05/19/ups…

For this reason alone, the rationale for retaining some form of a "level target" seems compelling, and a necessary labor utilization threshold would be an intuitive way of doing so. I would recommend this @DavidBeckworth thread for the full reasoning here:

Making both labor utilization and wage growth necessary conditions for ending forward guidance might seem too aggressive. What if inflation accelerates before labor utilization is close to the threshold? The result would be some inflation overshoot but that's a risk worth taking

The Fed says it is committed to symmetric inflation outcomes; given its systematic downside misses, it should be equally lenient to upside surprises and trying to accommodate as much progress in terms of labor utilization and wage growth as it reasonably can.

Our fourth proposed improvement is for the Fed to choose a better labor utilization indicator than the headline U-3 unemployment rate. This seems long overdue given the deterioration in the household survey's capacity to accurately count the unemployed: econweb.ucsd.edu/~jhamilto/AH2.…

The Evans Rule prematurely concluded because unemployment rate declines were largely driven by the unemployed dropping out of the labor force (not b/c of stellar job growth). If the Evans Rule used prime-age epop instead, it would have been in place for at least another year.

What's most important is that the Fed not allow itself to be fooled by the blurry lines b/w the unemployed and the nonparticipants. The most robust distinction to be made is between those who are employed and those who aren't

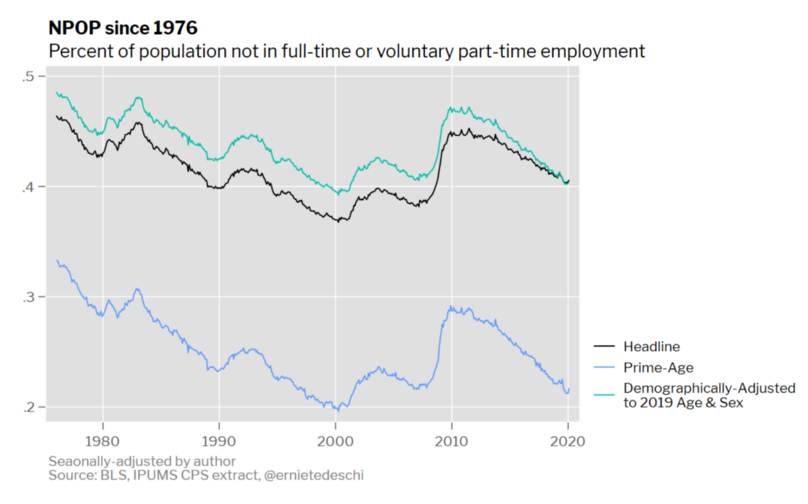

For a more robust measure of labor utilization that captures the surge in part-time underemployment, we would recommend using @ernietedeschi's demographically-adjusted NPOP measure. It's more complicated and but also the most robust way to go.

medium.com/@employamerica…

medium.com/@employamerica…

Our final two proposed improvements are about calibration: how the Fed initially sets thresholds could have an outsized impact on the final outcome. The best solution in our view is to initially presume against structural shifts and simply aim for the pre-COVID-19 labor market

This would mean a wage growth threshold of 3% year-over-year according to the employment cost index and a prime-age employment-to-population ratio threshold of 80.3%.

It's tempting to claim that certain shifts are structural and not cyclical, but the experience of the 2010s shows why it is valuable to resist that temptation, at least not without compelling evidence in terms of accelerating price inflation or wage growth.

The 2019Q4 labor market was not a "hot" labor market but largely one of decent wage growth and still below-target price inflation. To call it a hot labor market, you need to see some heat... cbsnews.com/news/federal-r…

If the Fed chooses more conservative thresholds to start out with, then as a remedy to this second-best approach, the Fed should be willing to dynamically revise their thresholds if more labor market progress appears achievable.

The Evans Rule was flawed in terms of its choice of 6.5% for the U-3 threshold, the choice of the U-3 itself, and the choice to make the U-3 threshold a sufficient condition for ending forward guidance but all of these flaws could have been mitigated...

All of these flaws could have been mitigated if the Fed was willing to revise its unemployment threshold down in 2013. The decline in participation and the absence of price/wage acceleration should have been a cue for the Fed to very rationally shift the goalposts...

All indicators and calibrations have their flaws. It wouldn't have been so ridiculous for the Fed to change its mind in the face of this evidence and lower the unemployment threshold accordingly.

If the Fed returns to state-based forward guidance (and we hope that it does), then we hope these suggested improvements are taken into consideration. There is so much at stake and while the monetary policy is far from a panacea, it's not powerless either.