$CVNA Thread on Financing Sales:

$CVNA could easily be using their relationship with DriveTime to offload their Financing products at Premium prices and their Financing Margins improved bc they started securitizing their own loans in 2019 and have since plateaued

$CVNA could easily be using their relationship with DriveTime to offload their Financing products at Premium prices and their Financing Margins improved bc they started securitizing their own loans in 2019 and have since plateaued

1) Before we get into this, you need to understand:

*CVNA CEO's dad is Ernest Garcia II, he owns and runs DriveTime & owns 38% of CVNA

*CVNA was originally a subsidiary of DriveTime prior to a spin-out and IPO

*CVNA is located next door to DriveTime

*DriveTime is Private

*CVNA CEO's dad is Ernest Garcia II, he owns and runs DriveTime & owns 38% of CVNA

*CVNA was originally a subsidiary of DriveTime prior to a spin-out and IPO

*CVNA is located next door to DriveTime

*DriveTime is Private

2) What financing do they actually sell? Its all the bullshit insurancy stuff car dealers try to sell you when you are buying a car.

VSCs = Vehicle Servicing Contracts = Extended Warranties

GAP Waiver Coverage = Coverage in case the car is totaled

Loan Receivables

VSCs = Vehicle Servicing Contracts = Extended Warranties

GAP Waiver Coverage = Coverage in case the car is totaled

Loan Receivables

3) $CVNA financing profit includes selling their loan receivables on loans they originate or the "commissions" they earn on selling others financing or servicing products (VSCs).

The VSCs are sold through the Master Service Agreement $CVNA has with DriveTime

The VSCs are sold through the Master Service Agreement $CVNA has with DriveTime

4) It's important to note the term "Recognize" in the language, as they don't actually receive the cash from DriveTime for these VSCs/GAP Waivers at the time of sale, they just recognize them as revenue and hand them off to DriveTime, so they increase working capital

5) So the VSCs and GAP Waiver Coverage go to DriveTime for a commission fee through the Master Service Agreement, but the loans are Securitized or Sold.

They either securitize loans themselves or sell them through Forward Flow Agreements to one financier, at "Premium Pricing"

They either securitize loans themselves or sell them through Forward Flow Agreements to one financier, at "Premium Pricing"

6) So who are these Finance Partners that buy through Flow Agreements?

Ally Financial

They do this through a Master Transfer Agreement which is been renewed on a yearly basis.

Pretty normal stuff, no big deal, other then the premium pricing part.

Ally Financial

They do this through a Master Transfer Agreement which is been renewed on a yearly basis.

Pretty normal stuff, no big deal, other then the premium pricing part.

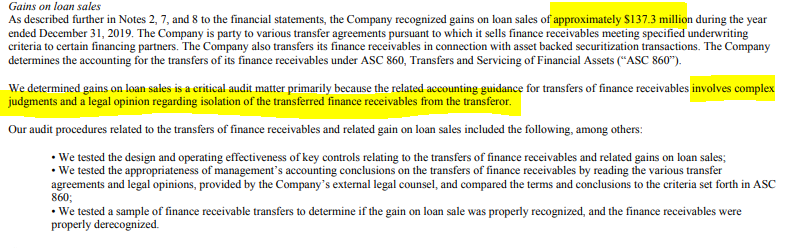

7) In 2019 $CVNA switched to the "We are going to Securitize our loans" model. This caused:

-a one time shift in Gross Profit Unit

-they had to retain 5% of their loan balances to comply with Risk Retention Rules

-uncertainty who the buyers were

-a one time shift in Gross Profit Unit

-they had to retain 5% of their loan balances to comply with Risk Retention Rules

-uncertainty who the buyers were

8) The securitization are done via Securitization Trusts (VIEs), in which $CVNA book Revenue at the time Loans receivables are sold into these Trusts (which they are the administrators of). The Trust then issue asset backed debt against the receivables.

9) All of the VIEs are off balance sheet, but they note their exposure in the 10K.

Kinda shady move to book revenue before any outside counter party actually pays them, but not illegal, just aggressive accounting, kinda the point of the VIE.

Kinda shady move to book revenue before any outside counter party actually pays them, but not illegal, just aggressive accounting, kinda the point of the VIE.

10) They do retain 5% interest in the VIEs, which can add up when your selling a $500m of Cars a Quarter.

This balance will only grow as they scale and as time progresses as this is just one year of Securitizations.

This increase their risk profile.

This balance will only grow as they scale and as time progresses as this is just one year of Securitizations.

This increase their risk profile.

11) So why did they decide to securitize there own loans. Simple, the Finance Gross Profit per Unit improved.

It was a one time jump in GPU, that is not going to improve from here. GPU Financing is essentially maxed out now.

It was a one time jump in GPU, that is not going to improve from here. GPU Financing is essentially maxed out now.

10) So who is buying these asset backed securities from the VIEs which seem to be yielding CVNA higher Gross Profit than the Ally Financing deal described as "Premium Pricing" by them?

That is the million dollar question.

That is the million dollar question.

11) Could one of the big buyers of the VIE debt be Ernest Garcia II and DriveTime?

Sure. Actually I would say its pretty likely they are involved somehow.

Why are VIE investors willing to pay above "Premium Pricing" for Loan Receivables?

Maybe they own 38% of $CVNA?

Sure. Actually I would say its pretty likely they are involved somehow.

Why are VIE investors willing to pay above "Premium Pricing" for Loan Receivables?

Maybe they own 38% of $CVNA?

12) How do they price these Financing instruments if in most cases they all either go to DriveTime or the VIEs before an actual counter party's steps in?

Well it seems largely based on their own Judgement.

Well it seems largely based on their own Judgement.

13) Note there is no proof that anything they are doing is illegal or even morally wrong, actually it might be a genius legal and business strategy from Ernest's point of view.

These off balance sheet VIEs happen all the time, and can make sense, but are less transparent

These off balance sheet VIEs happen all the time, and can make sense, but are less transparent

14) In Conclusion:

-GPU from Financing is not going up any more from here

-There clearly some advantages that $CVNA has that other competitors don't, (ie Relationship with DriveTime)

-The ability to inflate GPU Financing is there if they want to use it or not

-GPU from Financing is not going up any more from here

-There clearly some advantages that $CVNA has that other competitors don't, (ie Relationship with DriveTime)

-The ability to inflate GPU Financing is there if they want to use it or not