Rarible is a nonfungible token (NFT) marketplace where you can create, buy, and sell digital assets.

While the marketplace only launched in 2020, it’s already garnered ~$6 million in total platform sales. 🧵

While the marketplace only launched in 2020, it’s already garnered ~$6 million in total platform sales. 🧵

The war for NFT supremacy is underway – read the full analysis to find out if RARI is a rare opportunity or an overhyped governance token.

messari.io/article/a-rari…

messari.io/article/a-rari…

Rarible's growth corresponds with the launch of RARI – the platform's governance token – and Rarible's marketplace liquidity mining program.

is designed to reward platform users – buyers and sellers – with the ability to eventually govern the marketplace and trading fees.

is designed to reward platform users – buyers and sellers – with the ability to eventually govern the marketplace and trading fees.

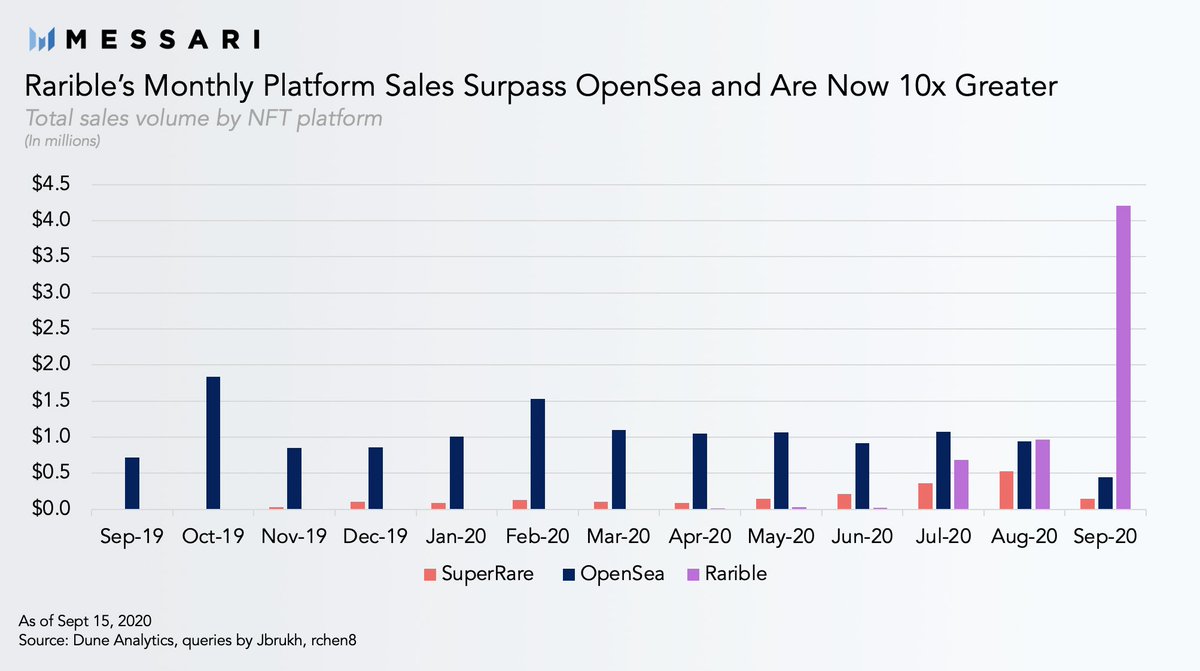

Rarible monthly volumes surpassed SupeRare in July 2020 and edged out OpenSea in August.

Rarible's exceptional growth then went parabolic in September, with a monthly sales volume that is now ten times greater than OpenSea. And we're only halfway through September.

Rarible's exceptional growth then went parabolic in September, with a monthly sales volume that is now ten times greater than OpenSea. And we're only halfway through September.

• • •

Missing some Tweet in this thread? You can try to

force a refresh