1/ Notes from @LTwolfe episode at @InvestLikeBest

I first heard Lauren Taylor (Impactive Co-founder) at Sohn Conference in 2019.

ESG has most certainly become one of the prominent narratives in recent years, and it's good to listen to someone who talks so passionately about it

I first heard Lauren Taylor (Impactive Co-founder) at Sohn Conference in 2019.

ESG has most certainly become one of the prominent narratives in recent years, and it's good to listen to someone who talks so passionately about it

2/ Impactive focuses on quality, valuation, time, and activism. Find businesses where time is your friend.

3/ A study showed activist situations typically settle two years out. So it's just better to avoid the battle and cut to the chase by not having adversarial relationship with management.

4/ "...the more surprises the market gets, the lower your multiple will be."

Owning your narrative, convincing the street, and then finally executing to live up to your narrative has to become a primary responsibility of a public market CEO by now.

Owning your narrative, convincing the street, and then finally executing to live up to your narrative has to become a primary responsibility of a public market CEO by now.

5/ Lauren is not a fan of dual class structure, and that's totally understandable.

But as a shareholder, this also reminds me of the following Zuck quote, "If I didn’t have complete control of Facebook, I would have been fired."

He's right. No perfect answer here I guess.

But as a shareholder, this also reminds me of the following Zuck quote, "If I didn’t have complete control of Facebook, I would have been fired."

He's right. No perfect answer here I guess.

6/ What does a pristine, healthy board look like?

Have a lot of cognitive diversity. Fully agreed.

Have a lot of cognitive diversity. Fully agreed.

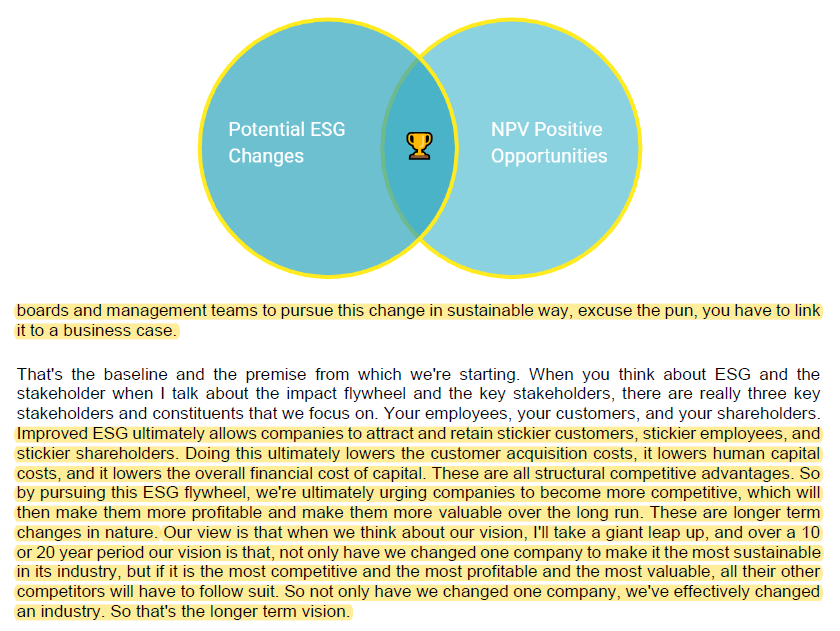

7/ Although there can be tensions in some cases/businesses, I do agree in most cases ESG and long-term shareholders are not at odds, if anything they are companions.

@IntrinsicInv recently wrote a very thoughtful piece on this.

intrinsicinvesting.com/2020/09/03/und…

@IntrinsicInv recently wrote a very thoughtful piece on this.

intrinsicinvesting.com/2020/09/03/und…

8/ Great example how Impactive worked with to unlock value.

9/ Kind of courageous for Patrick to ask whether there is a dark side to D&I focus.

During some one-on-one conversations, some friends acknowledged that there might be unintended consequences to this, but like Lauren, they wouldn't focus too much on that given the greater good.

During some one-on-one conversations, some friends acknowledged that there might be unintended consequences to this, but like Lauren, they wouldn't focus too much on that given the greater good.

10/ My personal opinion is D&I needs to be de-politicized which it unfortunately currently is.

Acknowledging concerns enhance understanding of the other side. Nuance is an underrated tool.

We all would love overnight progress, but it almost never happens.

Acknowledging concerns enhance understanding of the other side. Nuance is an underrated tool.

We all would love overnight progress, but it almost never happens.

End/ Episode: investorfieldguide.com/lauren-taylor-…

Transcript: investorfieldguide.com/wp-content/upl…

All my twitter threads: mbi-deepdives.com/twitter-thread…

Transcript: investorfieldguide.com/wp-content/upl…

All my twitter threads: mbi-deepdives.com/twitter-thread…

• • •

Missing some Tweet in this thread? You can try to

force a refresh