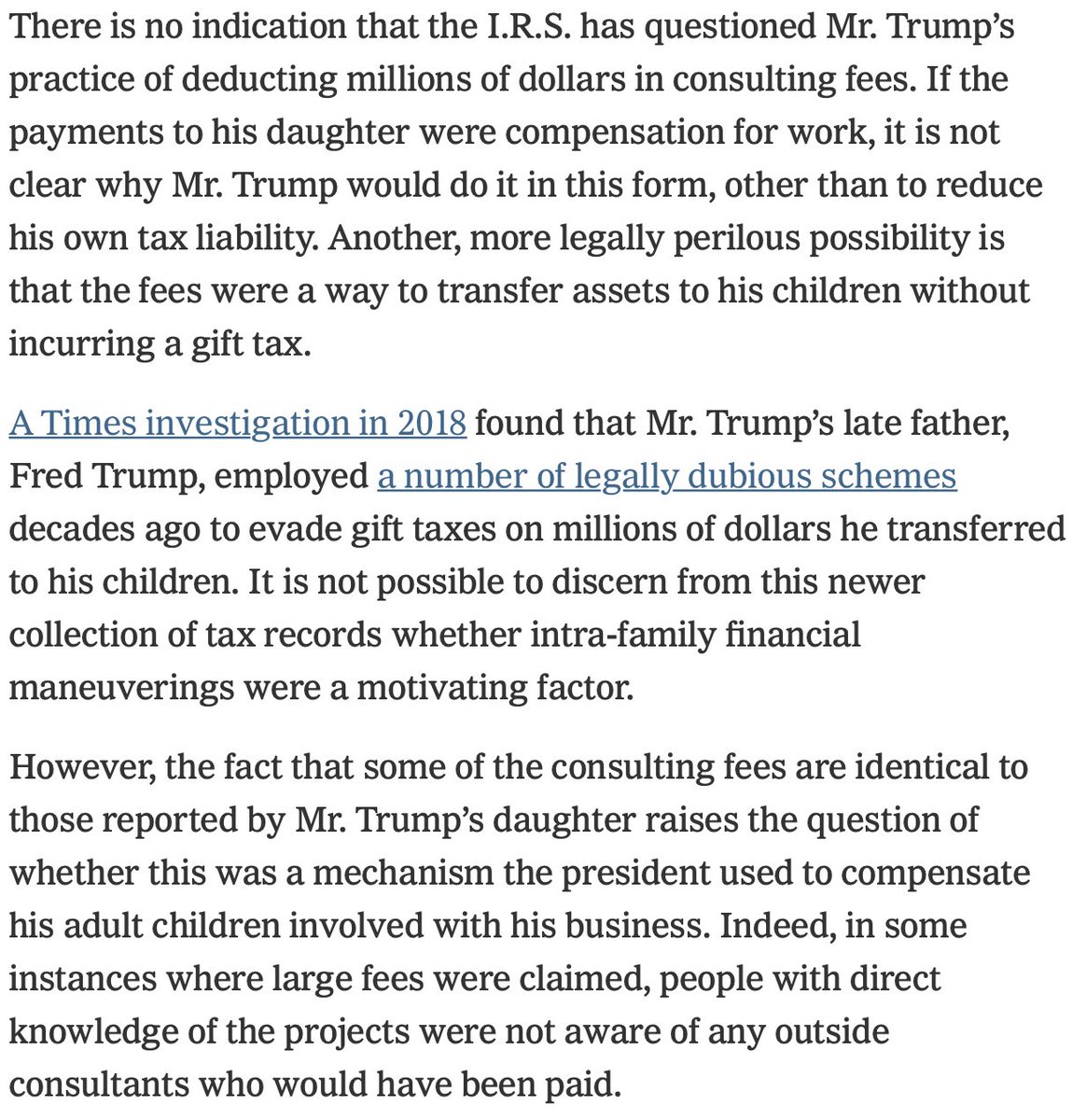

Trump tax thread. I'll start with the smaller stuff. What's with the consulting fees to the kids? 1/x

First, by structuring as a consulting fee instead of a gift, it avoids gift tax (and eventually estate tax). This only works if the fee is legit and market rate, which it certainly wasn't. 2/x

Second, a consulting fee is deductible by the partnership, while a gift is not. If Ivanka's marginal tax rate (consulting fees are includible, gifts are not) is < Donald's marginal tax rate (a big if), then it's a useful arbitrage. 3/x

Third, the kids might try to avoid payroll taxes by taking these consulting fees in lieu of higher salaries. The consulting fees were paid to Delaware LLCs (unclear if these LLCs were LLCs for tax purposes, or checked the box as S Corps). 4/x

The LLCs then distribute the cash as business income instead of salary, avoiding payroll taxes (including uncapped Medicaid at 3.8%). 5/x

Fourth, a (mostly) non tax motive: it spreads the graft around on paper. It's suspicious to pay salaries to your kids; less suspicious to pay consulting fees to LLCs. This might matter to Deutsche Bank and anyone else trying to evaluate the creditworthiness of the enterprise. 6/

Fifth, there is potential avoidance of state taxes if the payments are treated as Delaware business income instead of NY salary. Should pass through to NY either way, but who knows how it was reported. 7/end

• • •

Missing some Tweet in this thread? You can try to

force a refresh