The longer you study a subject, the closer you get to the core laws that govern it.

Here are 10 laws that govern banking, deduced from a decade of studying the industry...

[thread]

Here are 10 laws that govern banking, deduced from a decade of studying the industry...

[thread]

1. Success in banking is foremost about winning a war of attrition.

More than 17,300 banks have failed since the birth of the modern American banking industry in the Civil War.

That’s over three times the number of banks in business today.

More than 17,300 banks have failed since the birth of the modern American banking industry in the Civil War.

That’s over three times the number of banks in business today.

2. Consistency of earnings matters more than amplitude.

@First_Financial has been the highest valued regional bank for six years in a row, but the most profitable for only two.

The key is consistency. Its earnings have grown every year since '86, including in the '08 crisis.

@First_Financial has been the highest valued regional bank for six years in a row, but the most profitable for only two.

The key is consistency. Its earnings have grown every year since '86, including in the '08 crisis.

3. The darlings in one era are often pariahs in the next.

In 1978, Continental Illinois Bank & Trust was selected by Dun’s Review as one of America's five best-managed companies.

Six years later, it was seized by the FDIC due to mismanagement.

In 1978, Continental Illinois Bank & Trust was selected by Dun’s Review as one of America's five best-managed companies.

Six years later, it was seized by the FDIC due to mismanagement.

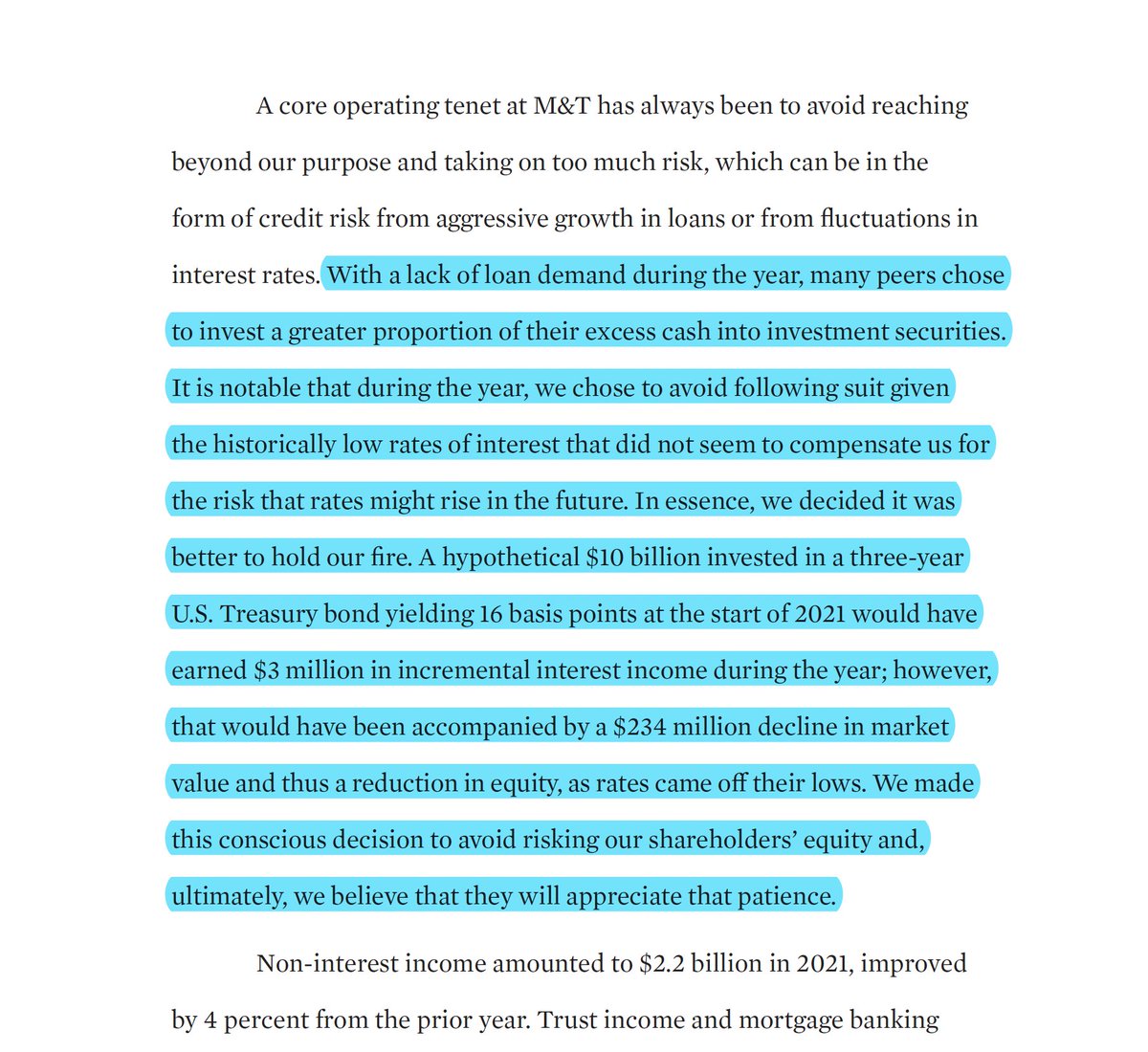

4. The crux of banking is watching what others are doing and then not doing it yourself.

Warren Buffett calls this the institutional imperative: “the tendency of executives to mindlessly imitate the behavior of their peers, no matter how foolish it may be to do so.”

Warren Buffett calls this the institutional imperative: “the tendency of executives to mindlessly imitate the behavior of their peers, no matter how foolish it may be to do so.”

5. Credit quality is a myth until it’s a reality.

Washington Mutual’s nonperforming assets as a % of all assets:

1998: 0.73%

1999: 0.55%

2000: 0.53%

2001: 0.93%

2002: 0.97%

2003: 0.70%

2004: 0.58%

2005: 0.57%

2006: 0.80%

2007: 2.17%

2Q08: 6.62%

4Q08: Failed

Washington Mutual’s nonperforming assets as a % of all assets:

1998: 0.73%

1999: 0.55%

2000: 0.53%

2001: 0.93%

2002: 0.97%

2003: 0.70%

2004: 0.58%

2005: 0.57%

2006: 0.80%

2007: 2.17%

2Q08: 6.62%

4Q08: Failed

6. Leverage is the friend of a good bank, enemy of the mediocre.

Most banks are leveraged by a factor of 10, enabling them to compound value, but leaving little margin for mistakes.

“And mistakes, have been the rule rather than the exception at many major banks," says Buffett.

Most banks are leveraged by a factor of 10, enabling them to compound value, but leaving little margin for mistakes.

“And mistakes, have been the rule rather than the exception at many major banks," says Buffett.

7. Efficiency is more about revenue than expenses.

“Every bank is two parts revenue and one part expenses,” former @usbank CEO Richard Davis once explained. “So if you want to improve efficiency, you’ll get twice as much bang for your buck by increasing revenue.”

“Every bank is two parts revenue and one part expenses,” former @usbank CEO Richard Davis once explained. “So if you want to improve efficiency, you’ll get twice as much bang for your buck by increasing revenue.”

8. All roads lead to skin in the game.

One reason @MandT_Bank has been so successful, its CEO Rene Jones once explained, “is that we could get 60% of our shareholders seated around the coffee table in my predecessor’s office.”

One reason @MandT_Bank has been so successful, its CEO Rene Jones once explained, “is that we could get 60% of our shareholders seated around the coffee table in my predecessor’s office.”

9. The prototype of a great banker rarely matches the stereotype of a great leader.

While the common stereotype of great leaders is aggressive, action-oriented and charismatic, the best bankers tend to be patient, cerebral and reserved.

While the common stereotype of great leaders is aggressive, action-oriented and charismatic, the best bankers tend to be patient, cerebral and reserved.

10. The hardest part of banking is the need to balance opposing forces.

Efficiency vs. employee morale

Revenue growth vs. risk management

Short-term performance vs. long-term solvency

END/

Efficiency vs. employee morale

Revenue growth vs. risk management

Short-term performance vs. long-term solvency

END/

• • •

Missing some Tweet in this thread? You can try to

force a refresh