Social tokens are an intriguing category of cryptoassets.

Using social tokens, creators and entrepreneurs can unlock new monetization opportunities leading to a tremendous amount of value being created by this emerging asset class.

Using social tokens, creators and entrepreneurs can unlock new monetization opportunities leading to a tremendous amount of value being created by this emerging asset class.

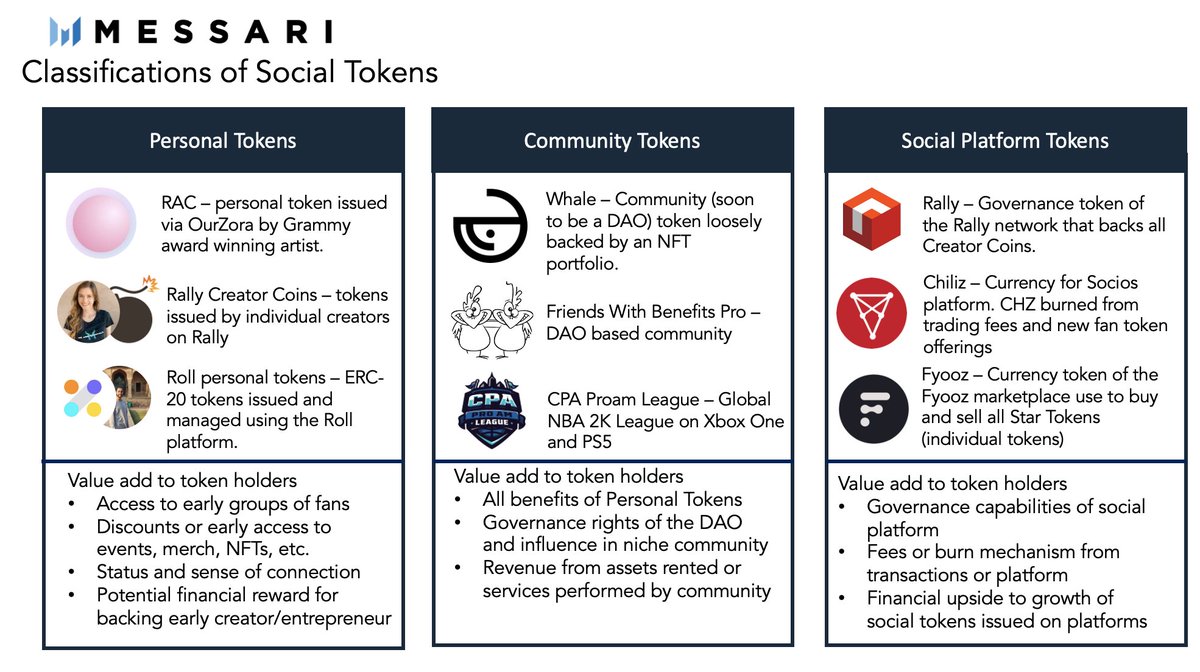

Generally, social tokens can be broadly categorized:

Personal - issued and controlled by a primary individual

Community - issued and controlled by a group, often managed by a DAO

Social Platform - tokens that govern a platform that facilitates social token issuance and exchange

Personal - issued and controlled by a primary individual

Community - issued and controlled by a group, often managed by a DAO

Social Platform - tokens that govern a platform that facilitates social token issuance and exchange

Several social tokens which have slowly developed into communities possess circulating market capitalizations of several million dollars.

Nearly all personal and community tokens (and their subsequent networks) are built on top of issuance platforms, some with their own social tokens.

As the social token landscape develops there will be lots of value captured by token-based networks along with adjacent businesses that support social tokens.

Crypto realigns the connection between creators and their followers into a symbiotic relationship.

While many social tokens will undoubtedly fail, however, a small subset will create immense value for creators and their early followers.

messari.io/article/the-so…

While many social tokens will undoubtedly fail, however, a small subset will create immense value for creators and their early followers.

messari.io/article/the-so…

• • •

Missing some Tweet in this thread? You can try to

force a refresh