Going through our monthly macro housing/econ deck (it's almost 400 slides)! 10 charts that caught my attention.

1/10: Apparently people buy homes even if mortgage rates aren't 3% or below.

1/10: Apparently people buy homes even if mortgage rates aren't 3% or below.

2/10: Looks like mortgage lending is back to pre-COVID norms. Lenders saying 'easy' fell off a cliff in 2Q20 but now back to norm.

3/10: Builders jacked prices 16% YOY in April, about 4x the rate of appreciation pre-COVID.

4/10: Cost of renting a home getting pretty close to cost of owning. With SFR rents shooting higher it'll be interesting to see if/when blue and green lines cross below.

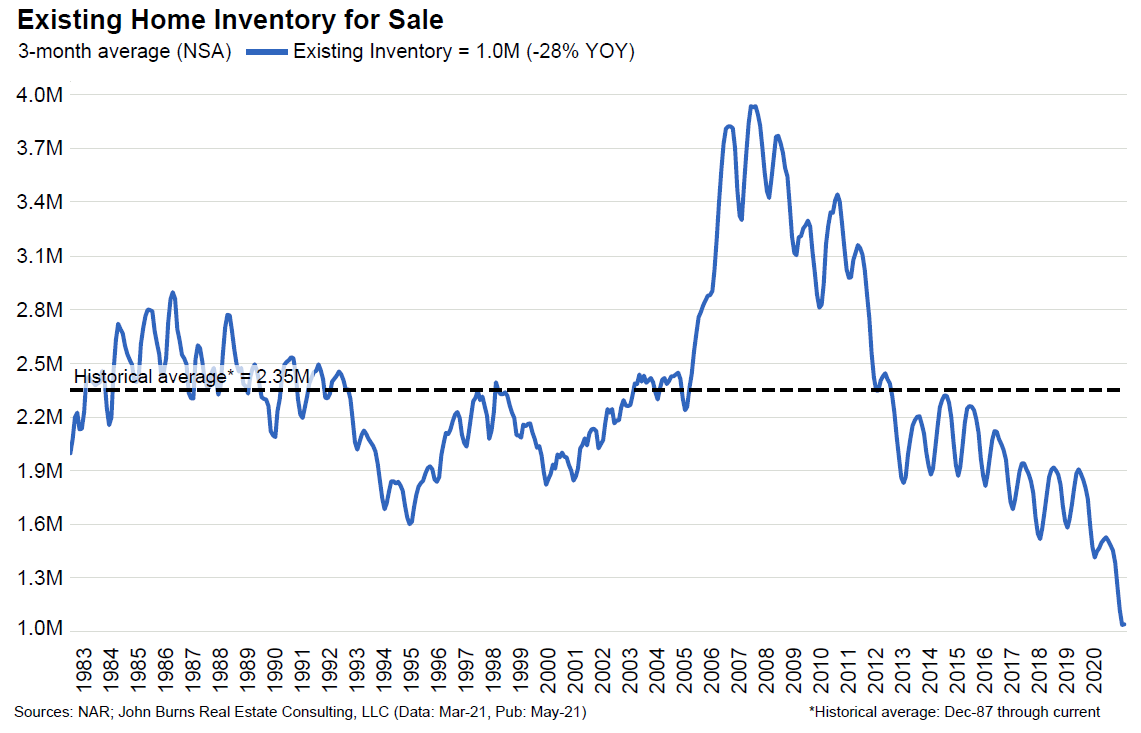

5/10: Good luck finding a home.

6/10: Spread between 'good time to buy home' & 'good time to sell home' has blown out (highest in a decade).

7/10: Average monthly student loan payment = $391. Two people in a household have saved over $9k in the last year if they've deferred payment during COVID. Nice down payment on a home in many parts of the country.

8/10: People REALLY like trucks (orange line). BTW, typically correlates nicely with new home construction trends.

9/10: Commodity prices are rising just a bit. No, lumber is not included in this index.

10/10: Biggest problem for businesses isn't poor sales (orange line), it's quality of labor (blue line).

• • •

Missing some Tweet in this thread? You can try to

force a refresh