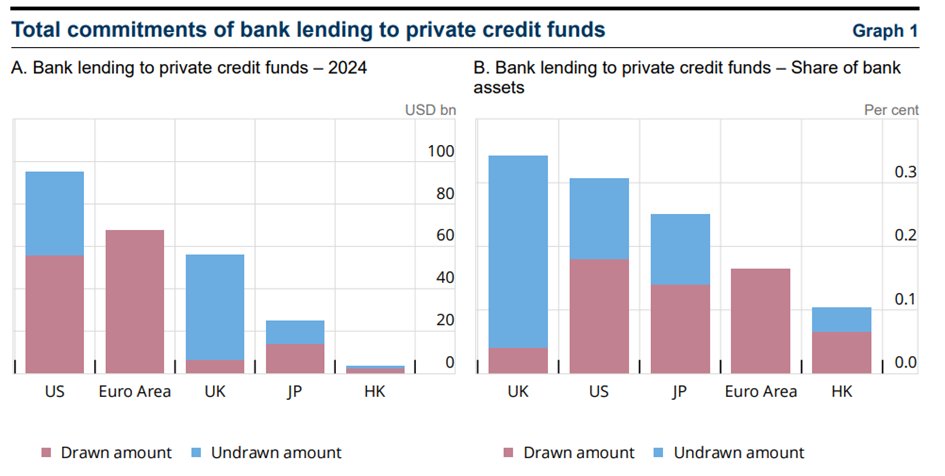

As always, the @ecb 's FSR is a treasure trove of information. Here’s a thread with my top 10 charts in the report and why I think they’re interesting. (No special order). 1/13

Investor sentiment on CRE

What’s interesting here is that the last time sentiment was 20% “at through”... the market was actually at a through! But since 2015, “peak” sentiment has been growing, and so have prices.

What’s interesting here is that the last time sentiment was 20% “at through”... the market was actually at a through! But since 2015, “peak” sentiment has been growing, and so have prices.

Regressing bankruptcies rate and GDP: this spectacular chart tells the economic story of Covid better than 1000 words: losses have been “socialized”, banks & SMEs have been shielded. I think we won’t get back to the regression line simply bc losses have already been transferred.

CFD/Equity TRS volumes. This chart is absolutely insane because, let’s be honest, equity TRS/CFD are widely used by retail investors to take exposure they absolutely don’t understand.

This chart is important because it shows that the ECB is still desperately trying to find reasons to worry about asset quality, despite excellent bank results. This time it’s the uptick in forborne loans. It’s hard to share their concern.

Always nice to have an up to date view on moratorium, this from Feb 2021. The huge default rate in Ireland is worrying and Portugal is clearly the country where risk remains largely unknown.

Let’s look at what contributed positively (in green) to changes in bank profitability and what contributed negatively (in red.) You can’t seen any green? Yeah, me neither. But banks are up 27% this year! Can you spell forward looking?

And the reason for that is in this chart – also a key item for the SSM, the ECB’s supervisory arm: profitability is expected to rise sharply. But look at that big orange bar! Cutting costs will be crucial. Social costs + execution risk = be careful.

This chart is extremely puzzling.

Credit risk RWA increased sharply in Q1.. then fell. This can’t be because ratings improved. Public guarantees were supposed to cover new loans, but I suspect what we see here is that banks have been offloading risks on the governments.

Credit risk RWA increased sharply in Q1.. then fell. This can’t be because ratings improved. Public guarantees were supposed to cover new loans, but I suspect what we see here is that banks have been offloading risks on the governments.

The right part of the chart is really for people who mock internal models: at least, those models didn’t say credit risk is going down during the biggest macro shock in a decade!

Really puzzling difference between IRB/SA

Really puzzling difference between IRB/SA

Just a fun chart on data which is hard to find: what kind of alternative assets do insurers buy?

Real estate, real estate, oh, and real estate. Also a bit of loans. All veryyyy liquid 😊

Real estate, real estate, oh, and real estate. Also a bit of loans. All veryyyy liquid 😊

And the last one, on a major but geeky topic. Banks with a small capital buffer were VERY reluctant to use their buffers, despite reinsurances from supervisors that they could do so.

Maybe they didn’t believe it, maybe they didn’t see a quick path to restore buffers post crisis

Maybe they didn’t believe it, maybe they didn’t see a quick path to restore buffers post crisis

Anyhow, this puts the topic of MDA on the table again – and AT1 investors should really watch this, it could be a game changer.

Go read the whole thing, it's really good!

Go read the whole thing, it's really good!

• • •

Missing some Tweet in this thread? You can try to

force a refresh