1/ Thread: $ADSK FY 1Q’22 Update

ADSK had a pretty decent 1Q, comfortably beating high end of the revenue guidance. 98% of revenue are now recurring, and net revenue retention was in the range of 100-110%.

Topline guidance was raised by ~$40 mn. Here are my notes from the call

ADSK had a pretty decent 1Q, comfortably beating high end of the revenue guidance. 98% of revenue are now recurring, and net revenue retention was in the range of 100-110%.

Topline guidance was raised by ~$40 mn. Here are my notes from the call

2/ Q1 is expected to be trough from growth standpoint and the rest of the year is likely to have some acceleration post-pandemic. ~75% of FCF of this year will be generated in the 2H.

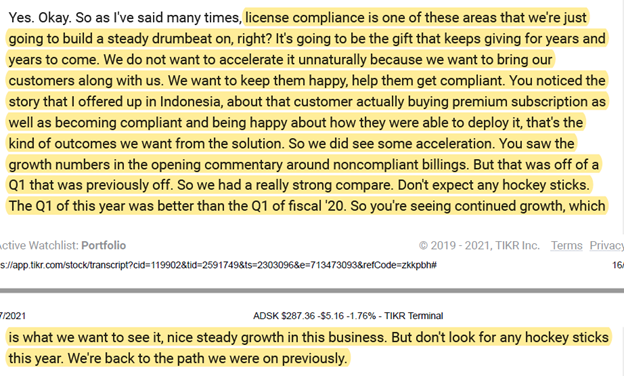

3/ Billings from converting noncompliant users doubled YoY in Q1. In fact, a noncompliant customer converted into one of the largest premium customers.

But don’t expect hockey stick growth from conversion of noncompliant users. ADSK wants to gradually and naturally convert.

But don’t expect hockey stick growth from conversion of noncompliant users. ADSK wants to gradually and naturally convert.

4/ “Fusion 360 has reached an adoption tipping point”.

Why? Network effects and deepening penetration among existing customers.

This is good to see since ADSK has been touting Fusion 360 as an important LT growth lever for the company.

Why? Network effects and deepening penetration among existing customers.

This is good to see since ADSK has been touting Fusion 360 as an important LT growth lever for the company.

5/ Is Fusion 360 cannibalizing Inventor? Not yet, and even when it does, ASP impact will be neutral.

6/ Revenue from direct sales increased 25% YoY and now 33% (vs 30% last yr) of total revenue.

Direct sales lead to greater price realization for ADSK which is another tailwind for topline.

Direct sales lead to greater price realization for ADSK which is another tailwind for topline.

7/ Some comments regarding the most recent acquisition: Upchain, which will be integrated to Fusion 360.

8/ Routine and “mandatory” question from sell-side how ADSK is going to deliver $2.4 Bn FY’23 which implies ~50% YoY.

CFO mentioned conversion of noncompliant users, increased penetration of direct sales, and favorable macro backdrop as the reason for their confidence.

CFO mentioned conversion of noncompliant users, increased penetration of direct sales, and favorable macro backdrop as the reason for their confidence.

9/ If I remember correctly, @SouthernValue95 once mentioned one of the big drivers for FCF is some large multi-year contracts that are up for renewal next year, so ADSK may enjoy more favorable NWC benefit next year which may also explain ~50% ramp up next year.

10/ “Even the infrastructure bill could be a wildcard for us. We're hopeful, although nothing is baked into our numbers at this point.”

ADSK is pretty focused on road, rail, and water when it comes to public infrastructure which it believes to be sweet spot.

ADSK is pretty focused on road, rail, and water when it comes to public infrastructure which it believes to be sweet spot.

End/ My deep dive on $ADSK (paywall): mbi-deepdives.com/adsk/ (Disclosure: I'm long)

Subscribe here: mbi-deepdives.com/plans/subscrib…

Subscribe here: mbi-deepdives.com/plans/subscrib…

• • •

Missing some Tweet in this thread? You can try to

force a refresh