A quick thread on Jay Powell and bank consolidation.

Tl;dr: By waving through bank mergers, Powell has undermined the Biden Administration's professed commitment to enhancing competition. The President should replace him as Fed Chair.

Tl;dr: By waving through bank mergers, Powell has undermined the Biden Administration's professed commitment to enhancing competition. The President should replace him as Fed Chair.

Under Powell's leadership, the Fed has been a rubber stamp for bank mergers.

The Powell Fed approved 95% of merger applications in 2018 (up from ~80% under Obama Admin). The Powell Fed also approved contested mergers at record speed: four months, on average (down from ~1 year).

The Powell Fed approved 95% of merger applications in 2018 (up from ~80% under Obama Admin). The Powell Fed also approved contested mergers at record speed: four months, on average (down from ~1 year).

The Powell Fed has also approved increasingly large mergers.

In 2012, Gov. Tarullo announced a presumption against acquisitions by GSIBs. Powell reversed course, approving Morgan Stanley-E*Trade. Powell also approved Truist and PNC mergers, creating 6 & 7th biggest U.S. banks.

In 2012, Gov. Tarullo announced a presumption against acquisitions by GSIBs. Powell reversed course, approving Morgan Stanley-E*Trade. Powell also approved Truist and PNC mergers, creating 6 & 7th biggest U.S. banks.

Lax bank merger oversight hurts consumers and the economy. Bank mergers increase costs and reduce availability of financial services. They lead to branch closures. Small bus. lending declines. Negative consequences are particularly harmful for LMI areas. theconversation.com/biden-wants-to…

Powell's permissive approach to bank mergers undermines policies promoting full employment.

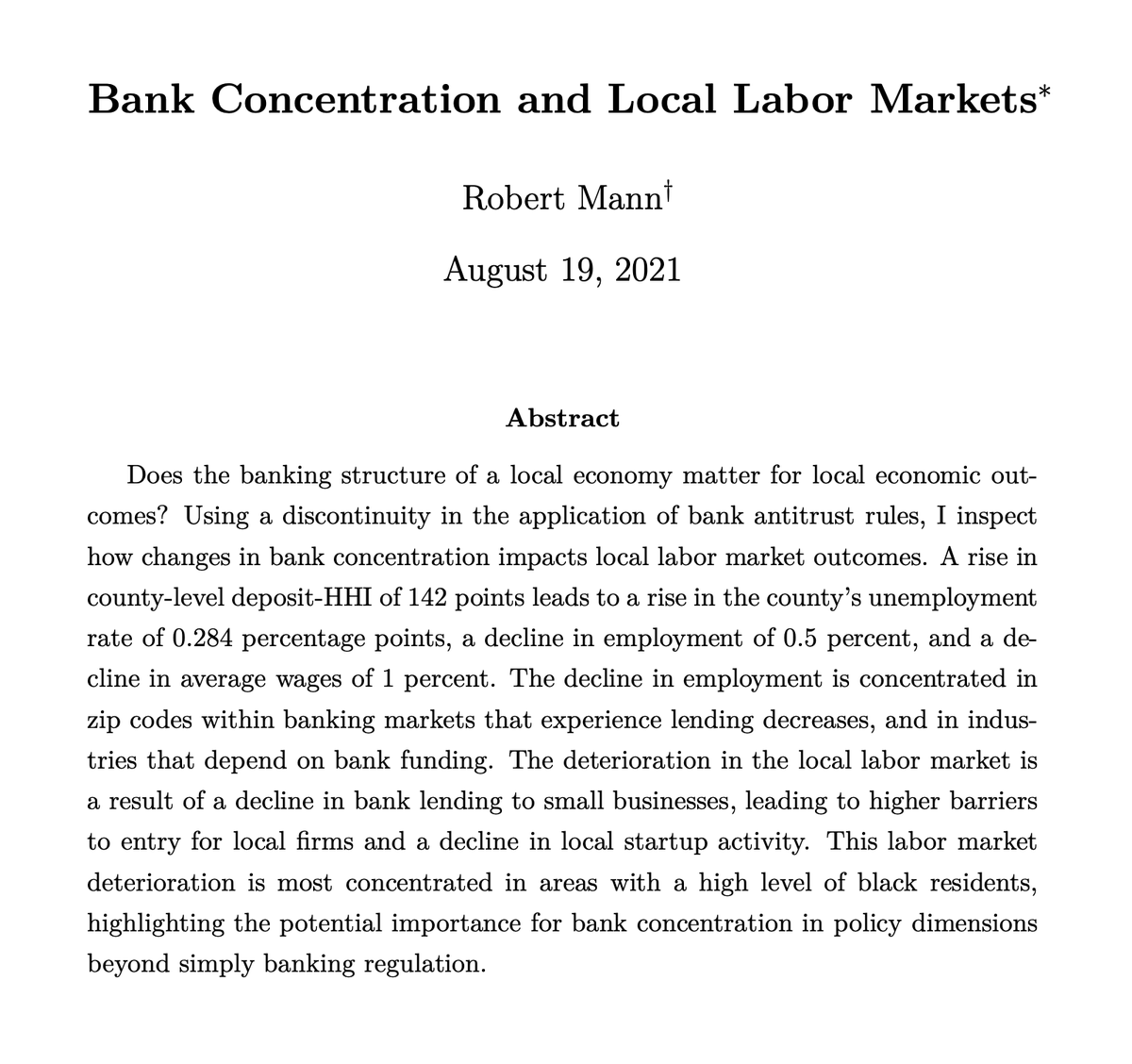

Bank consolidation has been shown to lead to higher unemployment and lower wages. If you care about full employment, you should care about bank mergers!

papers.ssrn.com/sol3/papers.cf…

Bank consolidation has been shown to lead to higher unemployment and lower wages. If you care about full employment, you should care about bank mergers!

papers.ssrn.com/sol3/papers.cf…

The other contender for Fed Chair, Gov. Lael Brainard, has been much better on bank mergers.

She voted against Morgan Stanley-E*Trade and Toronto Dominion-Schwab. She abstained on PNC-BBVA.

In May, she urged the Board to "undertake a broader review" of its merger framework.

She voted against Morgan Stanley-E*Trade and Toronto Dominion-Schwab. She abstained on PNC-BBVA.

In May, she urged the Board to "undertake a broader review" of its merger framework.

The Fed Chair is critical to bank merger policy for two reasons:

1. The Chair sets the agenda.

2. It's a numbers game. The Biden Admin likely needs Powell's seat to have a majority in favor of stronger merger oversight. politico.com/newsletters/mo…

1. The Chair sets the agenda.

2. It's a numbers game. The Biden Admin likely needs Powell's seat to have a majority in favor of stronger merger oversight. politico.com/newsletters/mo…

The White House issued an E.O. in July calling on bank regulators to "revitalize" bank merger oversight. That plan is due early next year.

Given Powell's track record, the White House should look elsewhere for a Fed Chair to lead that rethink.

whitehouse.gov/briefing-room/…

Given Powell's track record, the White House should look elsewhere for a Fed Chair to lead that rethink.

whitehouse.gov/briefing-room/…

• • •

Missing some Tweet in this thread? You can try to

force a refresh