For New Labor Forum I wrote about what’s wrong with funded pensions. It's a crucial question for many countries, and yet the debate is often confused.

I focus on one issue: Pension funds are financialization machines.

Open-access link & a short 🧵

journals.sagepub.com/doi/10.1177/10…

I focus on one issue: Pension funds are financialization machines.

Open-access link & a short 🧵

journals.sagepub.com/doi/10.1177/10…

Some context: The dream of wielding labor’s capital in the interest of workers is old, see Barber/Rifkin 1978.

And it's true that capital stewardship has often delivered results for US workers, see @DavidWebber's excellent Labor’s Last Best Weapon.

hup.harvard.edu/catalog.php?is…

And it's true that capital stewardship has often delivered results for US workers, see @DavidWebber's excellent Labor’s Last Best Weapon.

hup.harvard.edu/catalog.php?is…

But there are structural reasons why, despite the best meso-level efforts, at the macro-level the weapon is bound to misfire.

As @ewaldeng once put it, pension funds are structurally pressured to "push the envelope", investment-wise.

journals.sagepub.com/doi/abs/10.106…

As @ewaldeng once put it, pension funds are structurally pressured to "push the envelope", investment-wise.

journals.sagepub.com/doi/abs/10.106…

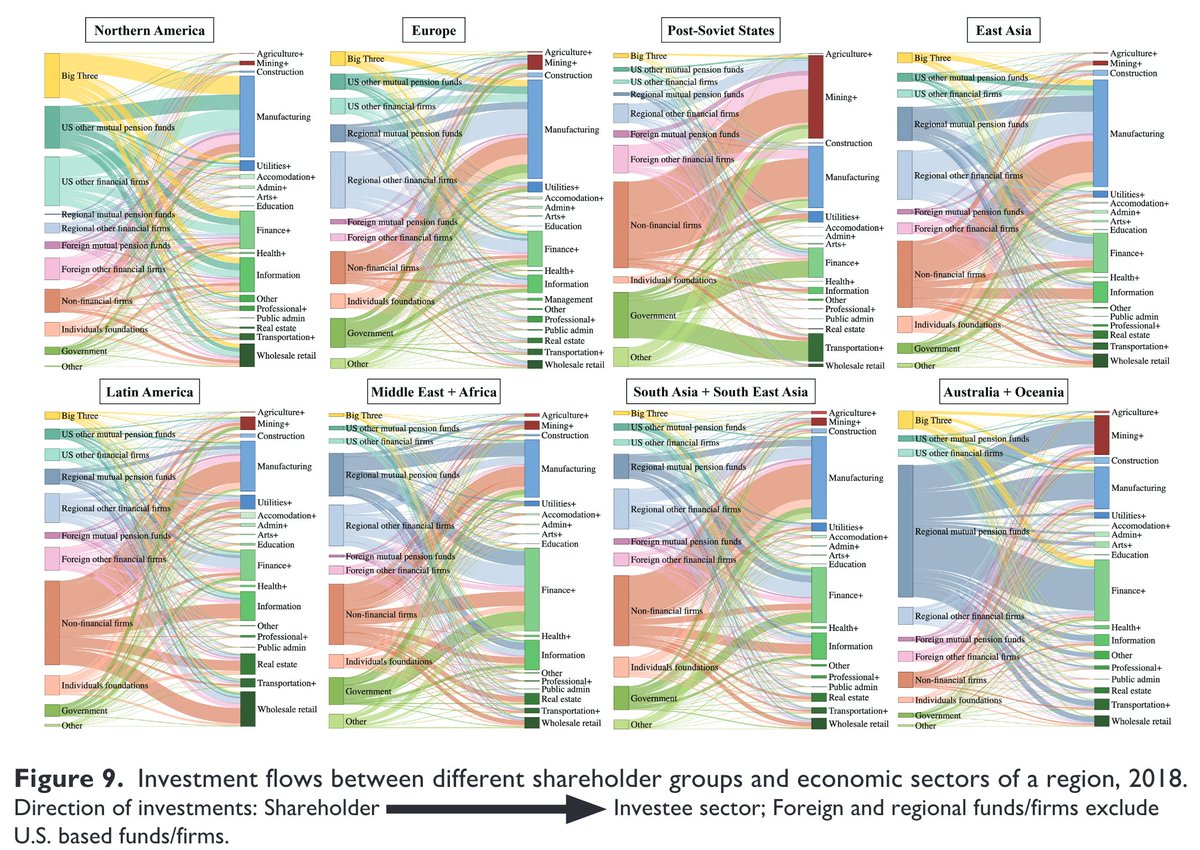

The core of the paper is this stylized history of US pension fund investments.

At every turn, pension funds pushed the envelope: From public to private securities, from direct investment to delegation to asset managers, from mutual funds to predatory hedge and PE funds.

At every turn, pension funds pushed the envelope: From public to private securities, from direct investment to delegation to asset managers, from mutual funds to predatory hedge and PE funds.

I made three charts to illustrate this. The first shows the evolution of the asset side of pension fund balance sheets since 1945. This story is well known.

This one's more interesting. The growth of mutual funds – and thus of the asset management sector as we know it – is largely a function of the growth of pension fund assets, and especially of IRAs and DC plans since the 1990s. (@its_mccarthy, you had asked about this.)

The grimmest picture is this one. US public pension funds, big or small, have roughly tripled their alternatives share, from under 10 percent in 2001 to 30 percent in 2020.

Labor's capital *made* the hedge/PE/VC fund billionaire class, and it's own expense.

Labor's capital *made* the hedge/PE/VC fund billionaire class, and it's own expense.

I'm not making a new argument. The pension financialization veterans @NataschaZwan, @its_mccarthy, @MNaczyk , @DrAdam_Dixon, @TobiasWiss loom large, as does the recent "Fiscal mutualism" piece by @SeanVanatta and @m_r_glass. (Many more I couldn't cite to due space constraints.)

There's also lot of excellent work on funded pensions & financialization in EMEs (this part got cut in the editing process). These two pieces by @BrunoBonizzi, @jenchurchill79 & Diego Guevara, and by @felipe_ruizb are excellent.

academic.oup.com/ser/article-ab…

link.springer.com/chapter/10.100…

academic.oup.com/ser/article-ab…

link.springer.com/chapter/10.100…

To sum up: In a liberalized financial system, "pro-labor financial capital" is an oxymoron – a meso-level dream turned into a nightmare by macro constraints.

For alternatives, look to the work of, among others, @lenorepalladino, @rch371, and @Cmmonwealth. Also: PAYGO is good.

For alternatives, look to the work of, among others, @lenorepalladino, @rch371, and @Cmmonwealth. Also: PAYGO is good.

On the path to an alternative regime, funded pensions are an obstacle rather than a stepping stone.

There's a sequencing problem: For things to get better for labor, they'd have to get worse for capital first – including for labor's capital.

PAYGO systems are good. /END

There's a sequencing problem: For things to get better for labor, they'd have to get worse for capital first – including for labor's capital.

PAYGO systems are good. /END

• • •

Missing some Tweet in this thread? You can try to

force a refresh