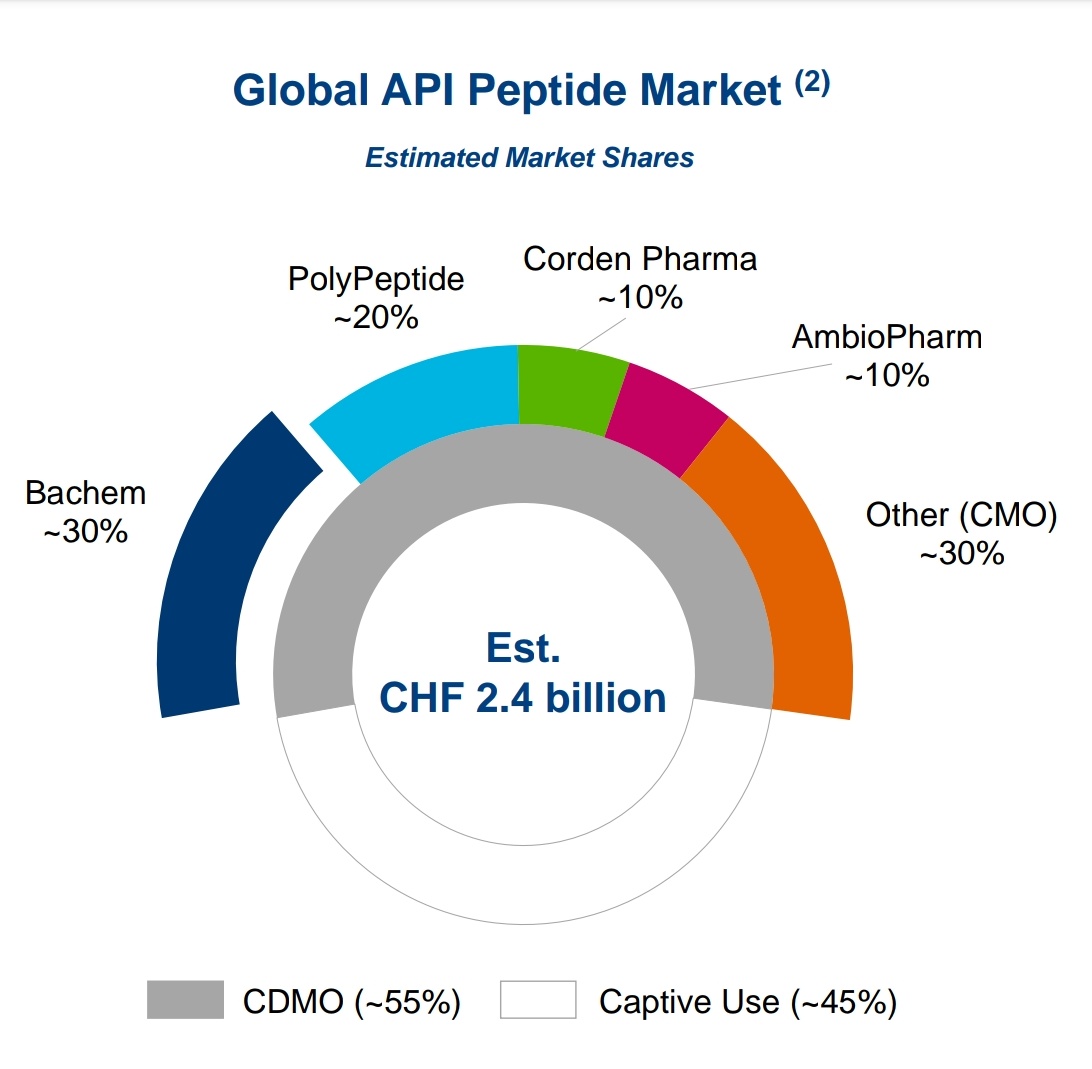

Global players in peptide business.

1. Bachem

2. Polypeptide

3. Corden Pharma

4. AmbioPharm

1. Bachem

2. Polypeptide

3. Corden Pharma

4. AmbioPharm

https://twitter.com/abhymurarka/status/1422568328279650305

Bachem

World's leading peptide CDMO.

150+ NCE Projects

1600+ employees across 6 locations

Expertise on Peptide NCEs & Oligonucleotide NCEs.

bachem.com/download/326/n…

bachem.com/download/180/b…

bachem.com/download/180/b…

World's leading peptide CDMO.

150+ NCE Projects

1600+ employees across 6 locations

Expertise on Peptide NCEs & Oligonucleotide NCEs.

bachem.com/download/326/n…

bachem.com/download/180/b…

bachem.com/download/180/b…

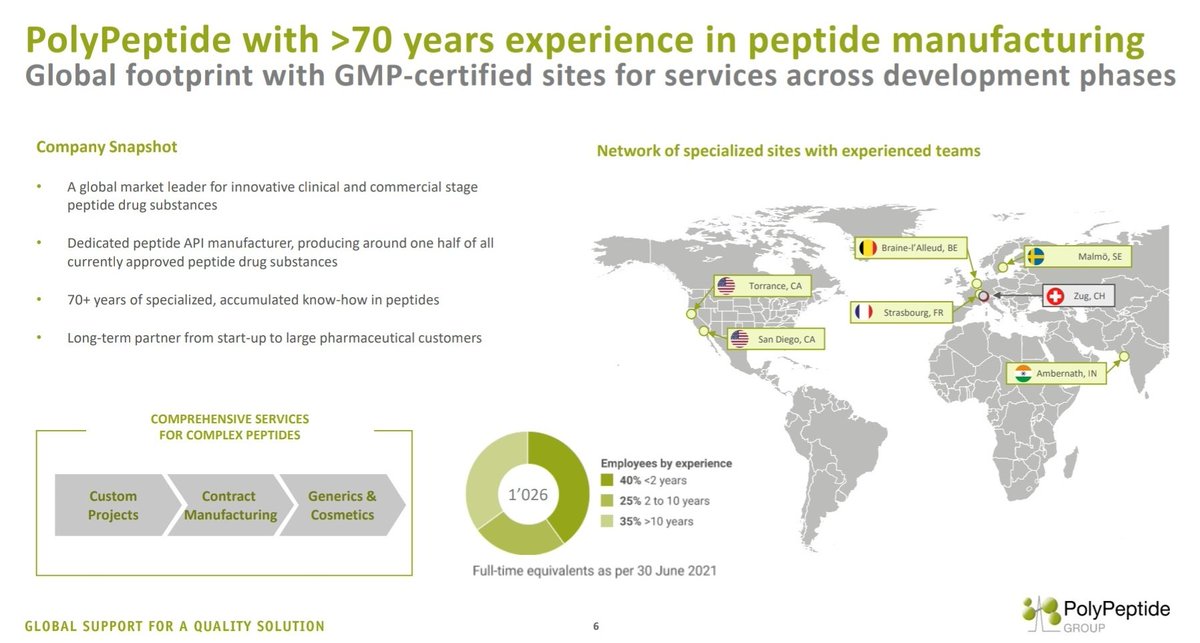

Polypeptide

Leader in outsourced peptide manufacturing.

Produces around half of the commercially aproved peptides.

6 GMP certified facilities including one in Ambernath, India.

1000+ employees

group.polypeptide.com/app/uploads/20…

Leader in outsourced peptide manufacturing.

Produces around half of the commercially aproved peptides.

6 GMP certified facilities including one in Ambernath, India.

1000+ employees

group.polypeptide.com/app/uploads/20…

Strong demand for peptide drugs.

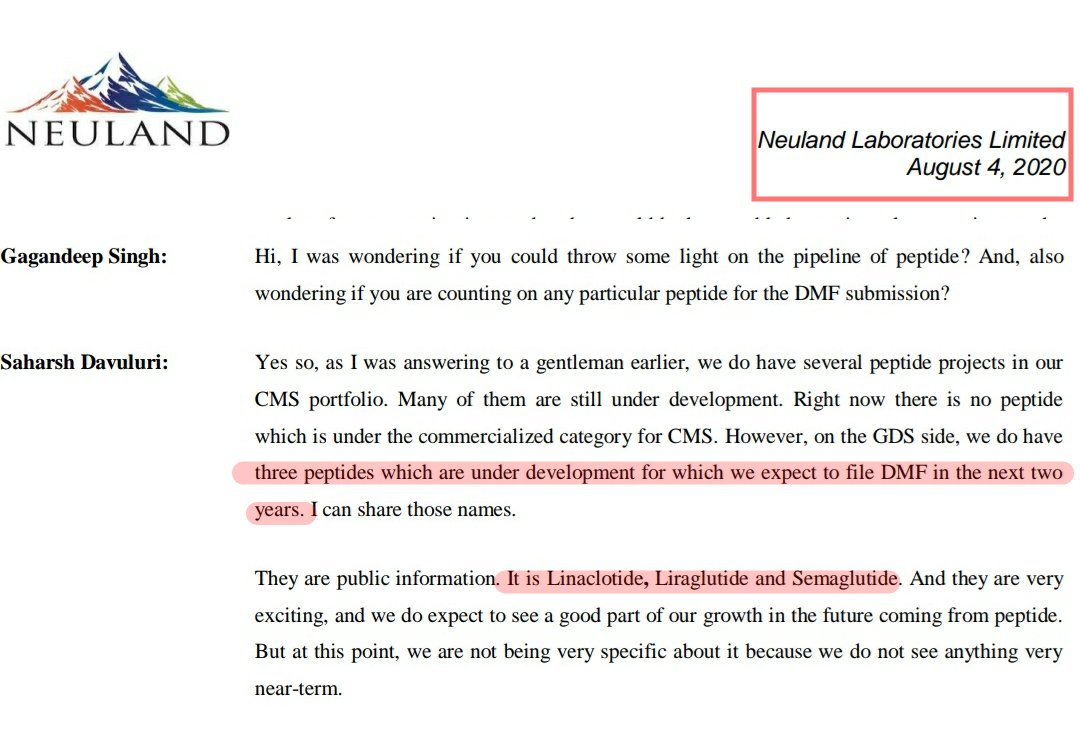

Piramal pharma looks good on peptide space than Neuland on DMF filings.

Neuland have 4 peptides under development, that too on early development phase & expects to file a DMF may be in the end of FY23.

(They had started developing these peptides from 2018)

(They had started developing these peptides from 2018)

These are the 4 peptides Neuland is working on in the generic space.

@rahuja671 has pointed out that there are only 3 peptides on the R&D pipeline of Neuland on the most recent API product list. (Jan 2022)

That means they might have omitted the peptide Octreotide from their pipeline.

That means they might have omitted the peptide Octreotide from their pipeline.

Neuland had been working on this molecule for the past 4 years and yet they couldn't commercialise it and now they have omitted it from pipeline.

Don't know the exact reason for that and couldn't find anything about that in past concalls.

Don't know the exact reason for that and couldn't find anything about that in past concalls.

• • •

Missing some Tweet in this thread? You can try to

force a refresh