#KrsnaaDiagnostics

Hav written multiple times abt the co in the past.

Would like to cover in more detail via below thread to understand what's the outlook for this diagnostic play dominating in PPP space via

A Short 🧵

(1/N)

Hav written multiple times abt the co in the past.

Would like to cover in more detail via below thread to understand what's the outlook for this diagnostic play dominating in PPP space via

A Short 🧵

(1/N)

The best part abt their asset light biz is, they offer the diagnostics service 40-45 pct cheaper than other players like Dr Lal, Metropolis etc, & yet co has the best operating margins, & key thing to note, key players dont apply for these govt tenders due to low pricing

(2/N)

(2/N)

Where as Krsnaa has a strong hold in the domain, while their competitors are local players who apply in these govt tenders, while govt is now looking at giving tenders to more established players like Krsnaa, who can actually manage these services at affordable price

(3/N)

(3/N)

Co has currently presence in 70 districts, while there are 760 districts in the country, as many other states start opting for PPP model.

The co is confident of immense growth in years to come.

(4/N)

The co is confident of immense growth in years to come.

(4/N)

Q3 Revenue for the co up 9 pct YoY led by core Biz of Radiology & Pathology which grew by 34 pct YoY, while Covid revenue down by 93 pct YoY.

Co plans to tie up with 5-6 Private Hospitals in this fiscal year

(5/N)

Co plans to tie up with 5-6 Private Hospitals in this fiscal year

(5/N)

Co has operationalized 5 centres in Punjab and 1 centre in Mumbai for Radiology and 5 processing centres, 42 collection centres for Pathology in Punjab.

Const. for 10 Radiology centres has bn completed & expected to operationalize soon, while 14 centres under construction

(6/N)

Const. for 10 Radiology centres has bn completed & expected to operationalize soon, while 14 centres under construction

(6/N)

Co has participated in 3 tenders in HP, Punjab & UP expecting the outcome soon, while various tenders are expected to come out in Assam, Bihar, Rajasthan & MP

Co to announce foray into private markets for health packages for corporates, introducing home collection services

(7/N)

Co to announce foray into private markets for health packages for corporates, introducing home collection services

(7/N)

Let's see the guidance given by the co for FY23.

Co expects to do a topline of upto 650 crores in FY23, as Punjab, HP & Mumbai centres operationalizes & ramped up.

Imp to note, current rate of Co rev is 400 crores.

FY23 wud see meaningful growth.

(8/N)

Co expects to do a topline of upto 650 crores in FY23, as Punjab, HP & Mumbai centres operationalizes & ramped up.

Imp to note, current rate of Co rev is 400 crores.

FY23 wud see meaningful growth.

(8/N)

Co is confident of having 30 pct Ebitda margins in coming years, & as biz grows organically from each centre, Co expects margins to inch up even higher, due to its asset light model, where space is provided by hospital.

(9/N)

(9/N)

Co will be doing a capex of 100 crores planned for FY23 to set up new centres based on tenders co win going forward.

Hope you liked the info, Do like & retweet if it was helpful.

@shubhfin

@NAVofNav

@sahil_vi

Hope you liked the info, Do like & retweet if it was helpful.

@shubhfin

@NAVofNav

@sahil_vi

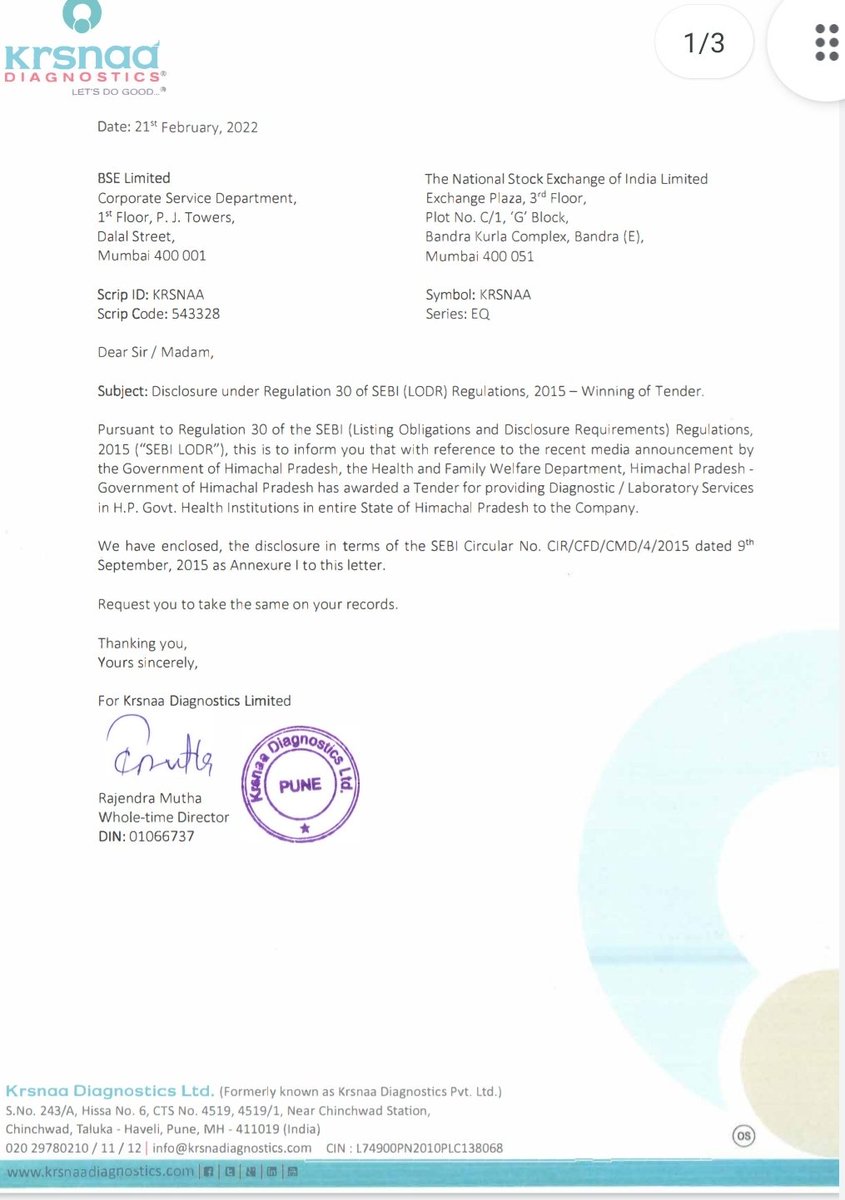

The best news I saw today, while preparing this thread ⬇

Co got the tender for diagnostics services by HP govt for the entire state :)

@sahil_vi

Co got the tender for diagnostics services by HP govt for the entire state :)

@sahil_vi

• • •

Missing some Tweet in this thread? You can try to

force a refresh