#Biocon_biologics

An effort to understand the biosimilar business.

Not a sell/buy recommendation.

Do your due diligence.

An effort to understand the biosimilar business.

Not a sell/buy recommendation.

Do your due diligence.

Earlier, Biocon hasn't had direct commercialization & supply chain in Developed Markets. They had partnered with Viatris (Mylan) for that.

Now, Biocon biologics has come up with an agreement to acquire Biologics business of Viatris for $3.3 Billion to create an unique vertically integrated biologics player.

Viatris will contribute to Biocon Biologics its biosimilars portfolio & related commercial & operational capabilities,amounting to 2022

estimated revenue of $875m & 2022 estimated adjusted EBITDA

of $200m for $3.335 billion,which is 16.5x of 2022 biosimilars

adjusted EBITDA.

estimated revenue of $875m & 2022 estimated adjusted EBITDA

of $200m for $3.335 billion,which is 16.5x of 2022 biosimilars

adjusted EBITDA.

Viatris will receive $2B cash & $1B of convertible preferred equity. Also receive up to $335m as additional cash expected to be paid in 2024.Viatris will own a stake of ~12.9% of Biocon Biologics, on a fully diluted basis. Viatris will also have certain priority rights in IPO.

This deal adds regulatory capabilities in regulated markets, commercial & supply chain capabilities to Biocon Biologics.

It seems like, Biocon plans to pay the $2B through $800m equity infusion & $1200m debt. (₹9000 Cr debt, that's an expected 5 fold jump in debt of biocon biologics)

The debt of this transaction will be supported by EBITDA base of ~₹1000 Cr of Biocon biologics + ₹1500 Cr ($200m) of Viatris.

That is combined estimated annual EBITDA of 2500 Cr.

That is combined estimated annual EBITDA of 2500 Cr.

For Viatris the deal is immediately accretive & they have got a very attractive valuation.

For Viatris, the EBITDA margin of biosimilar business was lower than the company average. It makes sense to sell the business at a very attractive 16.5x EBITDA multiple.

For Viatris, the EBITDA margin of biosimilar business was lower than the company average. It makes sense to sell the business at a very attractive 16.5x EBITDA multiple.

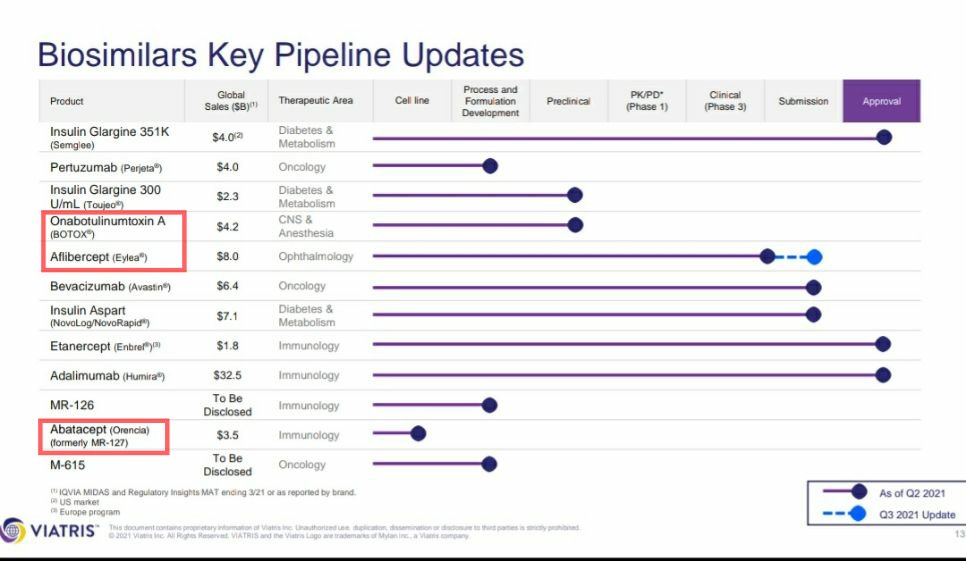

It seems like this deal is not the entire biosimilars portfolio. It does include all biosimilars developed alongside Biocon as well as a few others (biosimilars for humira, Enbrel, Eyelea)

But No mentioning of Abatacept (Orencia), Onabotulinum toxin A.

But No mentioning of Abatacept (Orencia), Onabotulinum toxin A.

There is an option to buy Aflibercept at $175M payment due in FY25.

Right now they have only 4 Biosimilars approved in US and 3 of those were first to get approval

Fulphila(Pegfilgrastim)

Ogivri (Trastuzumab)

Insulin glargine with interchangeability (Semglee)

Adalimumab(Hulio) will commercialize in US only on 2023 as there is patent protection.

Fulphila(Pegfilgrastim)

Ogivri (Trastuzumab)

Insulin glargine with interchangeability (Semglee)

Adalimumab(Hulio) will commercialize in US only on 2023 as there is patent protection.

Viatris (Biocon) was the first one to get approval for Pegfilgrastim biosimilar back in 2018.

They had launched Fulphila on July 2018.

They had launched Fulphila on July 2018.

Despite being the first one to launch & having early mover advantage, they had lost market share to Udenyca by Coherus.

Coherus launched their product Udenyca on Jan 2019.

Coherus launched their product Udenyca on Jan 2019.

By December 2019, Udenyca had gained 20.5% market share, while Fulphila (Biocon's product) had shrinked it's market share to 6%

Another biosimilar of Pegfilgrastim had launched on Dec 2019, Ziextenzo by Sandoz.

Right now, even Ziextenzo has more market share than Biocon's Fulphila.

Right now, even Ziextenzo has more market share than Biocon's Fulphila.

There is intense competition in Biosimilars.More players are coming in & it is not easy to maintain market share.

This leads to average selling price (ASP) erosion and margin decline as seen in generics.

In certain areas of Europe, there is tender,where winner takes all.

This leads to average selling price (ASP) erosion and margin decline as seen in generics.

In certain areas of Europe, there is tender,where winner takes all.

How did Coherus & Sandoz gain market share in Pegfilgrastim so fast while Viatris struggled?

Coherus (Udenyca) - They stockpiled 3 lakhs syringes prior to launch & they were able to do supply guarantees & did very well in market where others couldn't.

Coherus (Udenyca) - They stockpiled 3 lakhs syringes prior to launch & they were able to do supply guarantees & did very well in market where others couldn't.

Sandoz (Ziextenzo)- They were the first & only company to launch both long & short acting treatment options.

Together with better marketing of Novartis they've also gained more market share than Fulphila.

Together with better marketing of Novartis they've also gained more market share than Fulphila.

In case of Trastuzumab biosimilars, Ogivri of Viatris was dropped from preferred formulary list and substituted with Amgen's Kanjinti & Pfizer's Trazimera on Jan 2021.

Kanjinti is the market leader of Trastuzumab biosimilars now.

Kanjinti is the market leader of Trastuzumab biosimilars now.

National preferred formulary list helps in prescription and suggest which one to be preferred.

Ogivri of Viatris has a market share of 11.4% in US with 5 biosimilars and total of 60% biosimilar market share.

Amgen's Kanjinti is the market leader here.

Amgen's Kanjinti is the market leader here.

In Adalimumab (Humira) biosimilar space, 7 players have got approval and all of them will get commercialised on 2023 when patent expires for Humira.

Among those players, Cyltezo has got interchangeability approval on 2021 and Amgen is near to get that status.

Interchangeability status may help them to get good market share even during intense competition.

There will be intense competition among 7 biosimilars and Humira.

Interchangeability status may help them to get good market share even during intense competition.

There will be intense competition among 7 biosimilars and Humira.

Amgen tries to differentiate their product Amgevita (Adalimumab biosimilar) with

Latex free, citrate free preperation

Finer needle gauge

Interchangeability status.

Latex free, citrate free preperation

Finer needle gauge

Interchangeability status.

Amgevita has got leadership position in Adalimumab biosimilar space in Europe. They might replicate that success in US also.

Coherus tries to bring value proposition with

Very competitive price

Substantial supply guarantees

Pre filled syringe (PFS) with auto-injector

Non stinging citrate free formulation

29gauge fine needles

Very competitive price

Substantial supply guarantees

Pre filled syringe (PFS) with auto-injector

Non stinging citrate free formulation

29gauge fine needles

Humira had citrate in their formulation-injection was uncomfortable for the patient.

Coherus has developed proprietary non stinging citrate free formulation -greater comfort for patient.

29 gauge fine needle-less pain

Differentiating features helps to face fierce competition

Coherus has developed proprietary non stinging citrate free formulation -greater comfort for patient.

29 gauge fine needle-less pain

Differentiating features helps to face fierce competition

In Humira (Adalimumab) biosimilar, there is total of 15 players preparing for that, 7 players already got approval and competition is expected to be fierce.

80-90% price erosion may happen.

Others are developing differentiating features to face competition.

80-90% price erosion may happen.

Others are developing differentiating features to face competition.

What will be the differentiating feature for Viatris?

Where will it stand in this competitive space?

I couldn't find any differentiating feature for Viatris in Adalimumab biosimilar space.

Where will it stand in this competitive space?

I couldn't find any differentiating feature for Viatris in Adalimumab biosimilar space.

Coherus had gross margins of 84-82% in Udenyca (Pegfilgrastim biosimilar) with leadership position.

I don't think even Biocon has this much gross margin. (Kindly share info if this is wrong)

And Coherus continue to be in leadership position.

I don't think even Biocon has this much gross margin. (Kindly share info if this is wrong)

And Coherus continue to be in leadership position.

Coherus is planning to launch on-body-injector in 2023 which will compete directly with Neulasta Onpro(50% market share) to gain further market share.

Amgen expects severe competition against Neulasta and expects net price and volume erosion.

Despite having early mover advantage, Viatris (Biocon) have only 8-10% market share in both Ogivri and Fulphila.

As more players enter the market, competition will become much fierce, results in price erosion & decline in margins just like in generics.

Is biocon the lowest cost producer? Their margins doesn't say so.

Needs to be seen how this unfolds.

Is biocon the lowest cost producer? Their margins doesn't say so.

Needs to be seen how this unfolds.

Earlier they had CDMO partnerships with players other than Viatris. (Libbs & Sandoz)

What will happen to their CDMO opportunities now as biocon has become a competitor to them as they have acquired Viatris & become a fully integrated player.

What will happen to their CDMO opportunities now as biocon has become a competitor to them as they have acquired Viatris & become a fully integrated player.

• • •

Missing some Tweet in this thread? You can try to

force a refresh