At the commencement of this session of Parliament, Prime Minister Lee expressed his hope that, with a more sizable Opposition, there would be more sophisticated policy debate, with alternatives instead of just objections being offered. (1/n)

My #workersparty colleagues and I took that charge seriously. So when the GST hike was proposed, we took pen to paper, and worked out a range of revenue options that we felt could stave off the need to raise GST. (2/n)

By our estimates, the hole that GST would fill is around $3.6 billion. So we went ahead and worked out four different ways—we call these levers—that we could pull in more revenue, each built around a different theme. (3/n)

The first option increases effective taxes on MNCs, while leaving SMEs untouched. Our increase simply assumes full compliance with the OECD BEPS treaty (which we’ve signed). To enhance realism, we even allow for bleed in the income tax take for corporations and individuals. (4/n)

This corporate tax lever will yield $3.5 bn. So, while we’ll lose when some firms relocate and others pay revenue at their points of sale, we also save on needing to undercut others with corporate tax goodies. Others have corroborated how our tax take under BEPS could rise. (5/n)

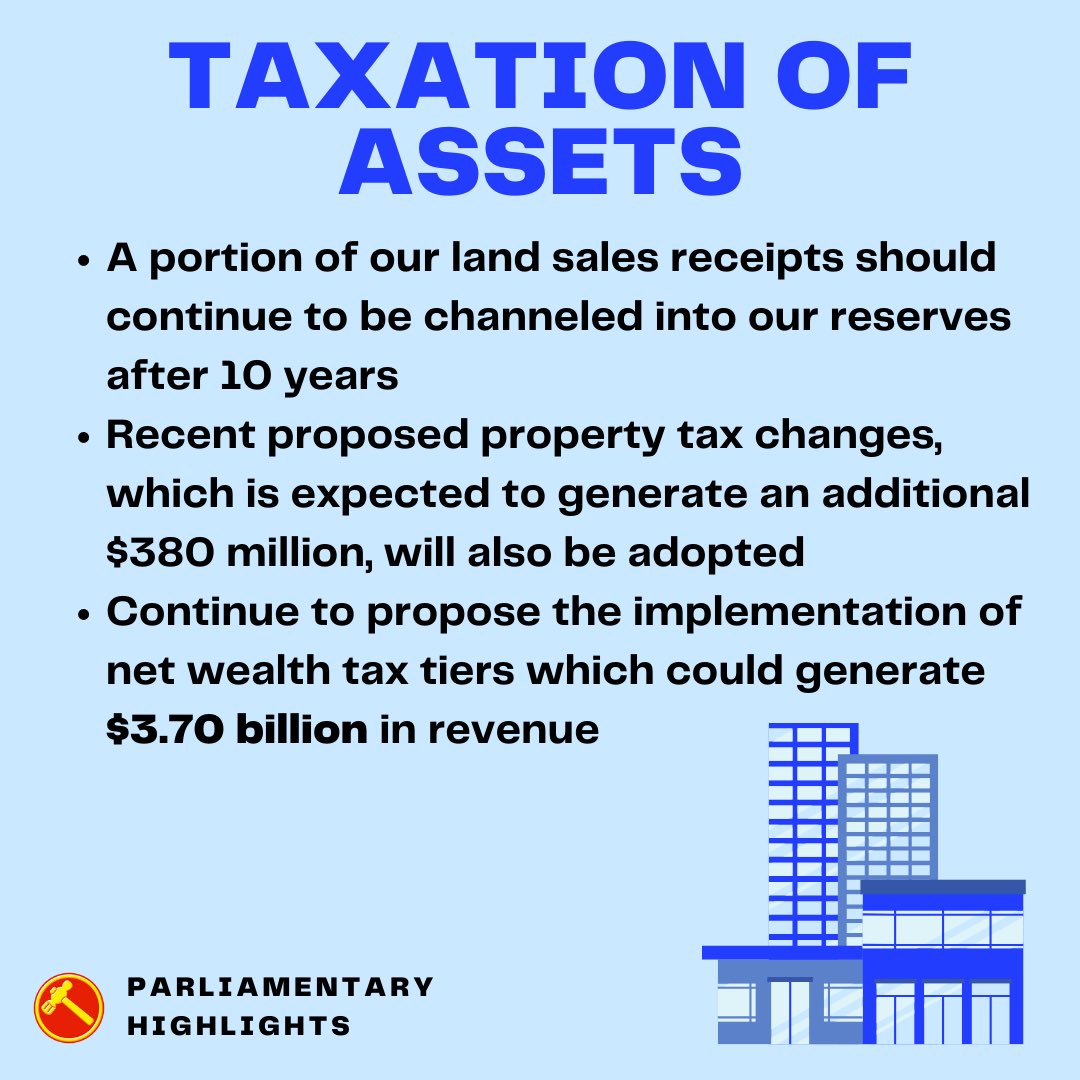

The second option extracts some revenue from land sales, higher property taxes, and wealth taxes. Basically, those with more assets contribute more, which is also a way to help address soaring inequality, something many Singaporeans care about. (6/n)

This asset tax lever will yield $3.7 bn. Does this “punish” success? That’s one way to look at it. Another way to see it is that those who have been more blessed, contribute back more. In most cases, the well-to-do won’t be made worse off; their wealth just grows slower. (7/n)

A third option is to change the share of our net investment returns contribution (NIRC) that we plough back into reserves—currently an arbitrary 50 percent—to 60 percent. This reserves lever will raise $4.3 bn. (8/n)

It is important to stress that this doesn’t run down our reserves. It just builds it up more slowly. As much as we want to invest for the future, we shouldn’t neglect the needs of the present. It doesn’t make sense to live in a giant house but eat kaya roti all day. (9/n)

A fourth option is to raise taxes on stuff that generates negative spillovers for others. We consider raising “sin” taxes—on alcohol, gambling, the like—and on carbon (to $80/ton, the upper bound of the government’s accepted range). (10/n)

This allows us to cap a corporate tax increase to only 8 percent. Together, this “externalities” lever will raise $3.7 bn. Admittedly, sin taxes tend to be regressive (the poor pay more as a share of incomes). But such taxes reduce the harm from gambling/alcohol addiction. (11/n)

In his response, Finance Minister Lawrence Wong rejected all these proposals, dismissing them as unrealistic or inconsistent with their philosophical beliefs. We obviously disagree. (12/n)

He said that the corporate tax revenue estimate was unrealistic, citing a straw man of a hypothetical $70 bn figure, used as a hyperbolic example. But our actual corporate tax lever yields much more credible numbers, consistent with our international obligations. (13/n)

He also rehashed the selfsame defense that land sales above 10 years should be treated as reserves, without addressing how our proposal extracts out the first 9 years of a lease into current revenue, which is already what the government does for leases below 10 years. (14/n)

He failed to explain how our reserves lever, which only reduces the NIRC by 10 percent (and doesn’t draw down reserves at all), “steals “from future generations, any more than the PAP’s own proposal to change the NIR formula in 2008 and 2015. (15/n)

And he repeated a tired trope that wealth taxes cannot be credibly enforced, ignoring how we make very modest recovery assumptions that yield only $1.2 bn from this source, far lower than figures put out by other independent analysts. (16/n)

Importantly, Minister Wong kept repeating that there was no other way to make ends meet, other than by hiking GST. As we showed, however, there are at least 4 levers we can pull, and pulling all four would cover the hole 4 times over. (17/n)

So rebut one component or even an entire lever, on the basis of principle or flawed assumptions. But the #workersparty is confident that the claim that there’s no other way is due to a lack of imagination or political courage, rather than genuine fiscal realities. (n/n)

• • •

Missing some Tweet in this thread? You can try to

force a refresh