Key takeaways from Calculating Return on Invested Capital by @mjmauboussin, D.Callahan.

cc:@SteadyCompound @realdennishong @EugeneNg_VCap @long_equity @JoinCommonstock @RamBhupatiraju @bkaellner @BrianFeroldi @InvestmentBook1 @HurriCap @Vivek_Investor @FromValue @MoS_Investing

cc:@SteadyCompound @realdennishong @EugeneNg_VCap @long_equity @JoinCommonstock @RamBhupatiraju @bkaellner @BrianFeroldi @InvestmentBook1 @HurriCap @Vivek_Investor @FromValue @MoS_Investing

ROIC is a measure of a company's capital efficiency.

Value Creation includes the spread of what a company earns above the cost of capital and how much the company can invest

Value Creation includes the spread of what a company earns above the cost of capital and how much the company can invest

Buffett coined the $1 test

- To test the success of a business, you should check if $1 invested in the company generate value more than one dollar in the market place.

eg. If a company invests $1000 into a factory and estimates the cost of capital at 10% . If the factory...

- To test the success of a business, you should check if $1 invested in the company generate value more than one dollar in the market place.

eg. If a company invests $1000 into a factory and estimates the cost of capital at 10% . If the factory...

generates $80 in after tax earnings in perpetuity. The market value of the factory would be $800($80/0.10)and hence fail Buffett's $1 Test

We are interested in understanding the changes in ROIC over time, not just the present ROIC.

The goal of the investor is to find a mismatch between the expectations built into the stock price and the financial results the company will actually achieve.

The goal of the investor is to find a mismatch between the expectations built into the stock price and the financial results the company will actually achieve.

This image below shows the ROIC formula

NOPAT

-measures the cash earnings of a company before financing costs

-assumes no financial leverage

-is the same whether a company is highly levered or debt free

NOPAT= EBIT - Cash Taxes

-measures the cash earnings of a company before financing costs

-assumes no financial leverage

-is the same whether a company is highly levered or debt free

NOPAT= EBIT - Cash Taxes

Invested Capital(IC)

-can think of it in 2 ways:

1. Amount of net assets a company needs to run a business

2. The amount of financing a company's creditors and shareholders need to supply to fund the net assets.

The image below demonstrates how to calculate IC in the 2 cases

-can think of it in 2 ways:

1. Amount of net assets a company needs to run a business

2. The amount of financing a company's creditors and shareholders need to supply to fund the net assets.

The image below demonstrates how to calculate IC in the 2 cases

Let's look at Cisco as an example.

Cisco had a NOPAT of $10.4 billion and Invested Capital amounting to $30.4 billion.

Thus a ROIC=[$10.4billion/($33.6 billion+$27.2billion/2)]=34.1% in fiscal 2013

Cisco had a NOPAT of $10.4 billion and Invested Capital amounting to $30.4 billion.

Thus a ROIC=[$10.4billion/($33.6 billion+$27.2billion/2)]=34.1% in fiscal 2013

Practical Issues in Calculating ROIC

-hosts of issues require one to make adjustments when doing their calculation

1. Excess Cash

2. Goodwill

3.Restructuring Charges

4.Operating Leases

5.Minority interests

6.R&D capitalization

7. Share Buybacks

-hosts of issues require one to make adjustments when doing their calculation

1. Excess Cash

2. Goodwill

3.Restructuring Charges

4.Operating Leases

5.Minority interests

6.R&D capitalization

7. Share Buybacks

Excess Cash

-treat ROIC and capital allocation issues separately

-the goal of ROIC is to understand how efficiently a company uses its operating capital, so we should only consider the cash a company needs to run its business

-so in calculations we need to exclude excess cash

-treat ROIC and capital allocation issues separately

-the goal of ROIC is to understand how efficiently a company uses its operating capital, so we should only consider the cash a company needs to run its business

-so in calculations we need to exclude excess cash

Goodwill

-for a proper ROIC calculation, we need to make sure the numerator and denominator consistent.

-so we need to ;ay attention to companies that have been in M&A's

-if the company has been acquisitive, distinguish between operating returns and acquisition returns

-for a proper ROIC calculation, we need to make sure the numerator and denominator consistent.

-so we need to ;ay attention to companies that have been in M&A's

-if the company has been acquisitive, distinguish between operating returns and acquisition returns

- thus we calculate ROIC including and excluding goodwill

Restructuring Charges

-restructuring charges include costs related to items such as reducing the size of the work force and plant closings

-you don't have to make any adjustments to capture the provision for charges

-restructuring charges include costs related to items such as reducing the size of the work force and plant closings

-you don't have to make any adjustments to capture the provision for charges

Operating Leases

-are any lease obligations the company has put on the balance sheet or capitalized

- if a company leases a substantial percentages of its assets, you should make adjustments for ROIC

-there are 2 steps to do this:

1. Adjust NOPAT by reclassifying the implied...

-are any lease obligations the company has put on the balance sheet or capitalized

- if a company leases a substantial percentages of its assets, you should make adjustments for ROIC

-there are 2 steps to do this:

1. Adjust NOPAT by reclassifying the implied...

interest expense portion of the lease payments from an operating expense to a financing cost. This increases EBITA.

2.Add the implied principal amount of the lease to assets as well as the debt. This increases the invested capital

2.Add the implied principal amount of the lease to assets as well as the debt. This increases the invested capital

Minority interests

-adjustment for minority interests is relevant either:

1. When another company owns a meaningful minority percentage of the company you are analyzing

2. When the company you are analyzing owns a meaningful minority stake in another company

-adjustment for minority interests is relevant either:

1. When another company owns a meaningful minority percentage of the company you are analyzing

2. When the company you are analyzing owns a meaningful minority stake in another company

-in the first case: Calculate ROIC as if the business is wholly owned

--in the second case: Calculate ROIC as you would normally excluding the minority stake

--in the second case: Calculate ROIC as you would normally excluding the minority stake

Share Buybacks

-ROIC is not affected by share buybacks provided you strip out excess cash

-ROIC is not affected by share buybacks provided you strip out excess cash

Return on Incremental Invested Capital(ROIIC)

-it is not the absolute ROIC that matters, but rather the change in ROIC. Having a sense of where ROIC is going can be of great value. A useful measure is ROIIC.

-ROIIC recognizes that sunk costs are irrelevant and what ...

-it is not the absolute ROIC that matters, but rather the change in ROIC. Having a sense of where ROIC is going can be of great value. A useful measure is ROIIC.

-ROIIC recognizes that sunk costs are irrelevant and what ...

matters is the relationship between incremental earnings and incremental investments.

Calculate ROIIC on a rolling 3 or 5 year basis. This is due to the fact that businesses sometimes have a volatile pattern of investments or NOPAT

This image below is of the ROIIC formula:

Calculate ROIIC on a rolling 3 or 5 year basis. This is due to the fact that businesses sometimes have a volatile pattern of investments or NOPAT

This image below is of the ROIIC formula:

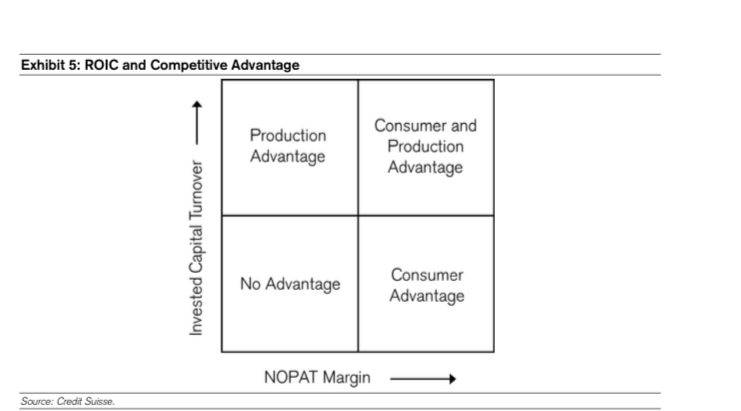

ROIC and Competitive Strategy Analysis

-companies with large excess returns generally have some competitive advantage

- an analysis of ROIC can indicate not only whether a company has a competitive advantage but it also shows what lies at the foundation of that advantage

-companies with large excess returns generally have some competitive advantage

- an analysis of ROIC can indicate not only whether a company has a competitive advantage but it also shows what lies at the foundation of that advantage

-there are 2 sources of a competitive advantage:

1. Consumer Advantage - due to habitual use of a product and high switching costs

2. Production Advantage- allows the company to deliver its goods/ services more cheaply than its competitors

Lets break down the ROIC:

1. Consumer Advantage - due to habitual use of a product and high switching costs

2. Production Advantage- allows the company to deliver its goods/ services more cheaply than its competitors

Lets break down the ROIC:

NOPAT/ Sales = NOPAT margin

Sales/ Invested Capital= Invested capital Turnover

Low Cost Retailer

-low NOPAT margin

-higher invested capital turnover

Luxury Goods retailer

-higher NOPAT margin

-low invested capital turnover

Sales/ Invested Capital= Invested capital Turnover

Low Cost Retailer

-low NOPAT margin

-higher invested capital turnover

Luxury Goods retailer

-higher NOPAT margin

-low invested capital turnover

If a company has a high ROIC through a high NOPAT margin- you should focus your analysis on a consumer advantage.

If high ROIC comes from a high turnover ratio- emphasize analysis of a production advantage

Here is the link to the document:research-doc.credit-suisse.com/docView?langua…

If high ROIC comes from a high turnover ratio- emphasize analysis of a production advantage

Here is the link to the document:research-doc.credit-suisse.com/docView?langua…

• • •

Missing some Tweet in this thread? You can try to

force a refresh