Sunday Musings:

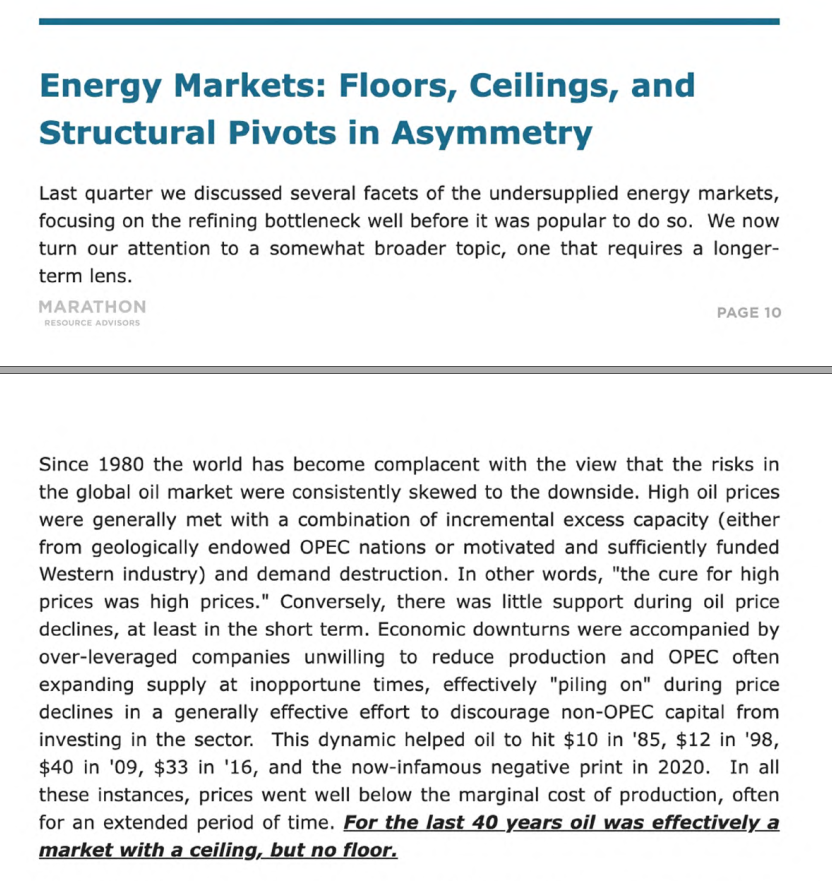

Several weeks ago we wrote to our LPs that we believed the oil markets were transitioning from 40 years of having a firm ceiling and no floor towards having a firmer floor and a vastly diminished ceiling.

This week's Saudi comments support that view.

Several weeks ago we wrote to our LPs that we believed the oil markets were transitioning from 40 years of having a firm ceiling and no floor towards having a firmer floor and a vastly diminished ceiling.

This week's Saudi comments support that view.

Historically, OPEC increased production into economic downturns. The resulting downside volatility discouraged western investment.

Their willingness to reduce supply to make room for Iranian barrels indicates they no longer need to, as decarb/ESG sentiment achieves same goal.

Their willingness to reduce supply to make room for Iranian barrels indicates they no longer need to, as decarb/ESG sentiment achieves same goal.

If correct, energy equities current status as effectively short-duration options on crude prices with negative skew may well evolve into something more akin to longer-duration options with flat or positive skew (extended duration = realization we still need it for next 15+ years)

More thoughts on complacency in the Agriculture markets, resource policy impacts on trade/currency markets and other topics.

Accredited/Qualified investors interested in reading the full letter can DM or request at mrafunds.com

early chart h/t @crudechronicle

#EFT

Accredited/Qualified investors interested in reading the full letter can DM or request at mrafunds.com

early chart h/t @crudechronicle

#EFT

• • •

Missing some Tweet in this thread? You can try to

force a refresh