1) A thread of hypotheses, loosely held.

This recession will be nothing like 2002, when EPS for the companies in the S&P 500 tech GIC declined 80%. Tech EPS likely even more stable this time than in 08/09 when EPS declined only -3%ish. Function of shift to recurring revs.

This recession will be nothing like 2002, when EPS for the companies in the S&P 500 tech GIC declined 80%. Tech EPS likely even more stable this time than in 08/09 when EPS declined only -3%ish. Function of shift to recurring revs.

2) From a trading perspective, weakness needs to be bought and strength needs to be sold.

Said another way, cannot chase and cannot press.

BTDSTR.

Freedom comes from discipline.

Said another way, cannot chase and cannot press.

BTDSTR.

Freedom comes from discipline.

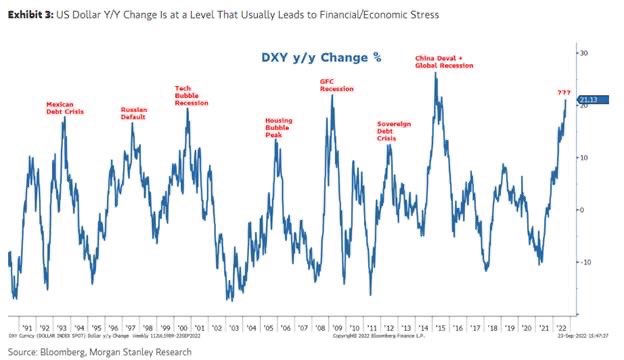

3) Actual inflation #’s are more important than the Fed. The market will trade on the former even more than the latter.

This is likely to be the first recession in living memory with positive nominal GDP growth and healthy consumer balance sheets. Prior playbooks may not work.

This is likely to be the first recession in living memory with positive nominal GDP growth and healthy consumer balance sheets. Prior playbooks may not work.

4) Competitive advantage changes more during a downturn than at any other time. CEO decisions are unusually important. This means that no matter how long-term an investor is, turnover is generally necessary during a downturn.

Must always balance conviction with *flexibility*

Must always balance conviction with *flexibility*

5) “Upgrading” a portfolio during a bear market sounds smart but just ensures underperformance when it ends.

The time to “upgrade” was before the bear market began.

The time to “upgrade” was before the bear market began.

6) Growing FCF per share is the best way to create value.

EV/FCF is my preferred valuation metric although GAAP P/E invaluable in bear markets for putting in a valuation floor.

EV/FCF is my preferred valuation metric although GAAP P/E invaluable in bear markets for putting in a valuation floor.

7) SMB software co’s over enterprise software co’s as this is a “top-down recession.”

Infrastructure software over application software. AI finally coming for the latter. Consumption over seat based.

Infrastructure software over application software. AI finally coming for the latter. Consumption over seat based.

8) Fabless semi co’s over equipment co’s. FIFO although datacenter spend still strong and may even improve in 23 with Genoa/Emerald Rapids enabling composable architectures (starting with memory pooling) that will drive hyperscaler margins and capital efficiency.

9) The memory pooling enabled by Genoa and Emerald Rapids will drive improved capital efficiency/margins for the hyperscalers over time but will have a Nehalem like impact over next 2 years as payback on CPU refresh will be at 10+ year highs. Basically will pull spend forward.

10) Long-term impact of composable architectures on memory demand and AI innovation very hard to call.

Curious to see if Bergamo and Sierra Forest slow down ARM in datacenter as RISC and CISC architectures continue converging.

Curious to see if Bergamo and Sierra Forest slow down ARM in datacenter as RISC and CISC architectures continue converging.

11) Innovation that we have seen at the data warehouse/lakehouse/whatever layer is coming to storage primitives in the cloud. Competitors for EBS/S3 coming in same way came for Redshift. Same silly multi-cloud argument will work while driving actual efficiencies for layers above.

12) Impact of IDFA/ATT will steadily recede from a targeting/measurement perspective but will be a long, long time before we get back to 2020 levels of ROAS.

This massively advantages the dominant eCommerce incumbent who was previously suffering from 1000s of small DTC nicks.

This massively advantages the dominant eCommerce incumbent who was previously suffering from 1000s of small DTC nicks.

13) Short form video may lead inferior economics for social media co’s over the long-term as creator payout competition ramps.

14) Internal silicon efforts at hyperscalers may slow down outside of AWS. The Annapurna team was one of a kind and the external silicon vendors today are much more willing to customize and embed hyperscaler IP, etc. See TPU embarrassment over time.

15) Companies that started cutting early are going to be advantaged both near-term and longer-term. Companies with weak CEOs who cut late have to cut deeper which hurts coming out.

CEOs who cut costs late = investors who “upgrade” with the mkt down 25%ish.

CEOs who cut costs late = investors who “upgrade” with the mkt down 25%ish.

16) The operating leverage in *some* SaaS companies is going to massively surprise to the upside in 2023. And broadly speaking, tech margins will be better than expected as they all finally have religion on this.

17) Crypto needs to develop multiple real world use cases outside of remittances and “store of wealth” for non USD countries.

18) Geopolitical risk has never been higher in my career.

Still amazes me that multiple people can be competent enough to become dictators for life yet be utterly incompetent at anything other than acquiring power.

Analogous to many CEOs so guess I shouldn’t be amazed.

Still amazes me that multiple people can be competent enough to become dictators for life yet be utterly incompetent at anything other than acquiring power.

Analogous to many CEOs so guess I shouldn’t be amazed.

19) Nothing is more dangerous to the financial health of a tech founder pre-IPO/sale than a high valuation given they own common and the investors own preferred. Many are learning this lesson in 2022.

20) Public mkt analogy is that nothing is more dangerous to the financial health of a high profile tech CEO/founder than super-voting stock.

Super-voting stock doesn’t encourage long-term thinking, it just encourages bad decision making.

All power corrupts.

Super-voting stock doesn’t encourage long-term thinking, it just encourages bad decision making.

All power corrupts.

21) Hypothesis > thesis for investing. The former encourages one to seek disconfirming info while a thesis is “a substantiation of of a specific view” and thereby encourages one to seek confirmatory evidence.

Hypotheses are at the heart of the Scientific Method.

Hypotheses are at the heart of the Scientific Method.

22) Take all this with a grain of salt as I have made many mistakes over the past year.

23) I like to end on MJ’s number. He is the 🐐 and significantly better than LBJ. This is not a hypothesis. Just a fact.

• • •

Missing some Tweet in this thread? You can try to

force a refresh