It seems like several Central Banks are going through a sudden ''change of heart''.

Recently many Central Banks and today the ECB came out pretty dovish.

Let's see what's going on, and whether the Fed is going to join the party too.

A thread.

1/

Recently many Central Banks and today the ECB came out pretty dovish.

Let's see what's going on, and whether the Fed is going to join the party too.

A thread.

1/

Australia, Canada and now Europe are starting to weigh pros and cons of calibrating monetary policy with a single objective: bringing inflation down to 2%, as soon as possible.

Instead, they are beginning to consider a slowdownor a complete pause in rate hikes.

Why...

2/

Instead, they are beginning to consider a slowdownor a complete pause in rate hikes.

Why...

2/

...such a sudden ''change of heart''?

Because all these jurisdictions have something in common: inherent fragilities.

Be it private sector debt/domestic housing market (Canada) or a very suboptimal ‘‘monetary & fiscal union’’/recession fears (Europe)...

3/

Because all these jurisdictions have something in common: inherent fragilities.

Be it private sector debt/domestic housing market (Canada) or a very suboptimal ‘‘monetary & fiscal union’’/recession fears (Europe)...

3/

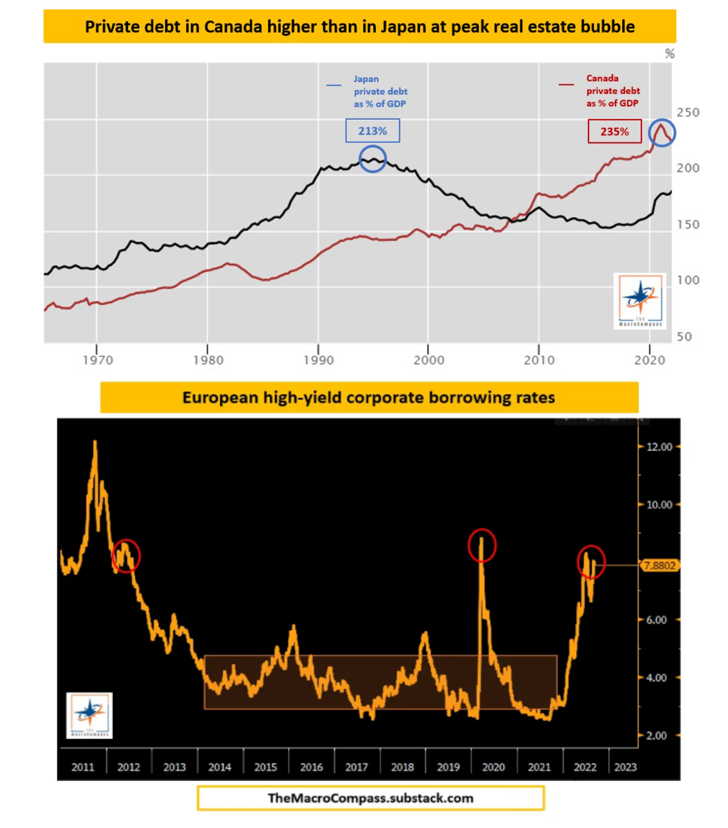

...it’s become increasingly clear that relentless monetary policy tightening will end up breaking something.

Have a look at this chart.

Canada: private debt as % of GDP higher than in Japan at the peak of the real estate bubble

Europe: junk corporates under big pressure

4/

Have a look at this chart.

Canada: private debt as % of GDP higher than in Japan at the peak of the real estate bubble

Europe: junk corporates under big pressure

4/

With such a backdrop, if you are the ECB once you tightened by 200 bps in a few months the pros and cons of further aggressive tightening become more ‘‘balanced’’.

In other words, the ECB is ‘‘hoping’’ that markets are right about inflation falling off a cliff and...

5/

In other words, the ECB is ‘‘hoping’’ that markets are right about inflation falling off a cliff and...

5/

...most importantly that a mild tightening of their monetary policy stance above neutral rates will be enough to engineer such a sharp drop in inflation.

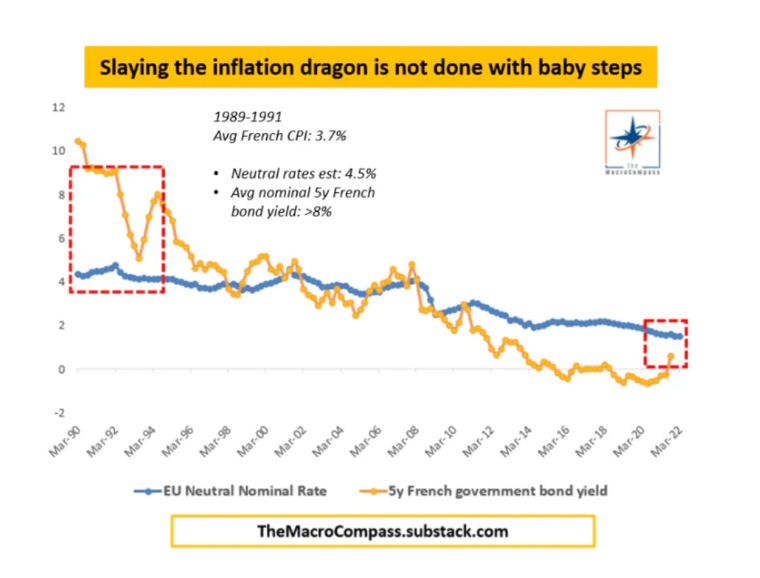

While this might happen, history is not on the ECB side.

Historically, sticky and persistent inflation is not slayed...

6/

While this might happen, history is not on the ECB side.

Historically, sticky and persistent inflation is not slayed...

6/

...with baby steps.

Again, a chart says more than 1,000 words.

In the 90s, France faced CPI >4% for quarters in a row.

Nominal yields 350 (!) bps above neutral for 2 years (!) were necessary to slay the inflation dragon.

7/

Again, a chart says more than 1,000 words.

In the 90s, France faced CPI >4% for quarters in a row.

Nominal yields 350 (!) bps above neutral for 2 years (!) were necessary to slay the inflation dragon.

7/

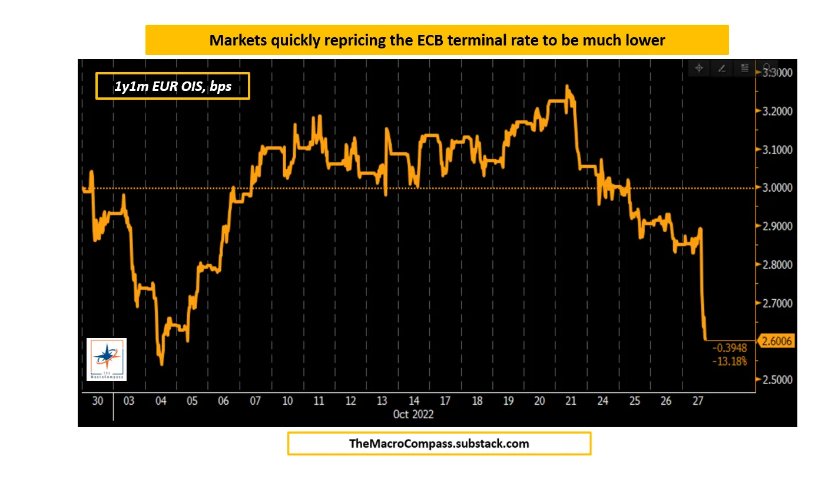

After today's dovish ECB meeting, markets are instead pricing the ECB terminal rate in the 2.5% area.

My estimate for nominal neutral EUR rates is 1.5%.

100 bps above neutral for a limited period of time sounds like not much with CPI at 10%.

8/

My estimate for nominal neutral EUR rates is 1.5%.

100 bps above neutral for a limited period of time sounds like not much with CPI at 10%.

8/

Before we move to market reactions, a word about the other important ECB decision of the day: changes in TLTRO conditions.

The ECB also drastically changed the remuneration mechanism for TLTROs, the cheap funding mechanism that allowed European banks to borrow ~ EUR 2 trn...

9/

The ECB also drastically changed the remuneration mechanism for TLTROs, the cheap funding mechanism that allowed European banks to borrow ~ EUR 2 trn...

9/

...at very advantageous rates during the pandemic.

The idea there is simple: incentivize banks to repay these TLTRO loans as soon as possible, hence shrinking the (huge) ECB balance sheet and at the same time easing some of the collateral scarcity in Europe.

10/

The idea there is simple: incentivize banks to repay these TLTRO loans as soon as possible, hence shrinking the (huge) ECB balance sheet and at the same time easing some of the collateral scarcity in Europe.

10/

The two obvious candidates to shrink the ECB balance sheet are QT and a reduction in outstanding TLTROs.

The ECB is well aware of the dangers of QT in the Eurozone (Italy, Greece?), and hence incentivizing banks to repay TLTRO loans early seems like a more viable option...

11/

The ECB is well aware of the dangers of QT in the Eurozone (Italy, Greece?), and hence incentivizing banks to repay TLTRO loans early seems like a more viable option...

11/

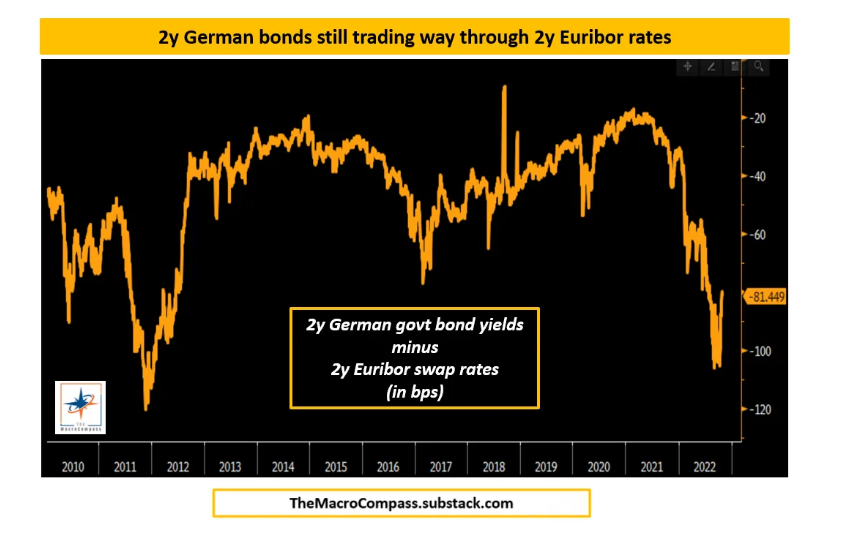

The hope is also that correcting the imbalance between a very abundant level of excess reserves and a scarce amount of good quality collateral (AAA German bonds) will ease the collateral scarcity in Europe.

Right now, German bonds command a very sizeable scarcity premium.

12/

Right now, German bonds command a very sizeable scarcity premium.

12/

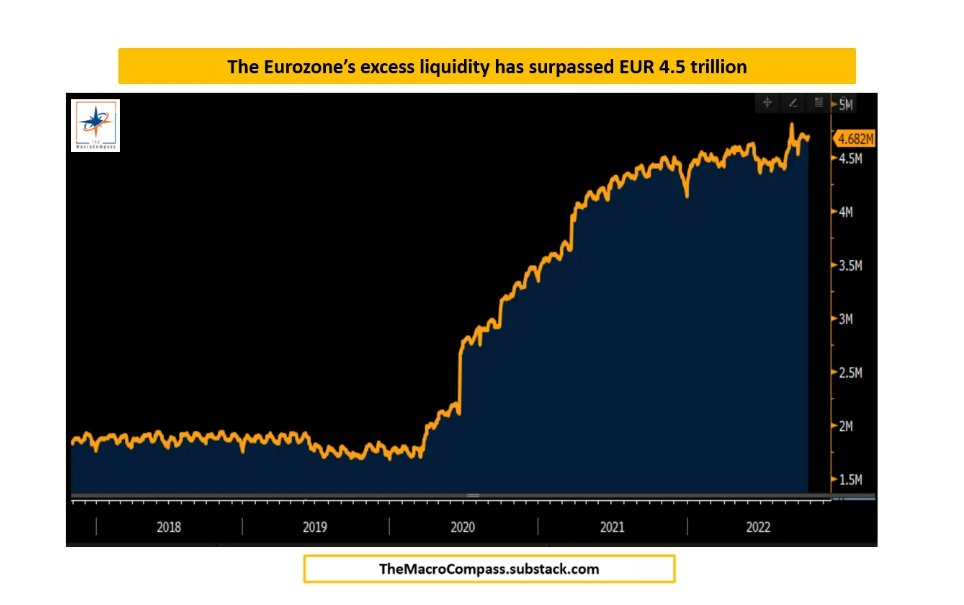

As the ECB balance sheet has ballooned to over EUR 4.5 trillion and this gigantic amount of excess reserves is at odds with a tightening monetary policy stance, the ECB is looking for ways to shrink its size.

Will they succeed this way?

I think so, but...

13/

Will they succeed this way?

I think so, but...

13/

...less excess reserves and more bond issuance to fund energy subsidies and other fiscal maneuvers might also end up requiring wider risk premia in Europe.

Now, how did markets react?

Very coherently, if you ask me.

Let's look at the nuances in the bond market.

14/

Now, how did markets react?

Very coherently, if you ask me.

Let's look at the nuances in the bond market.

14/

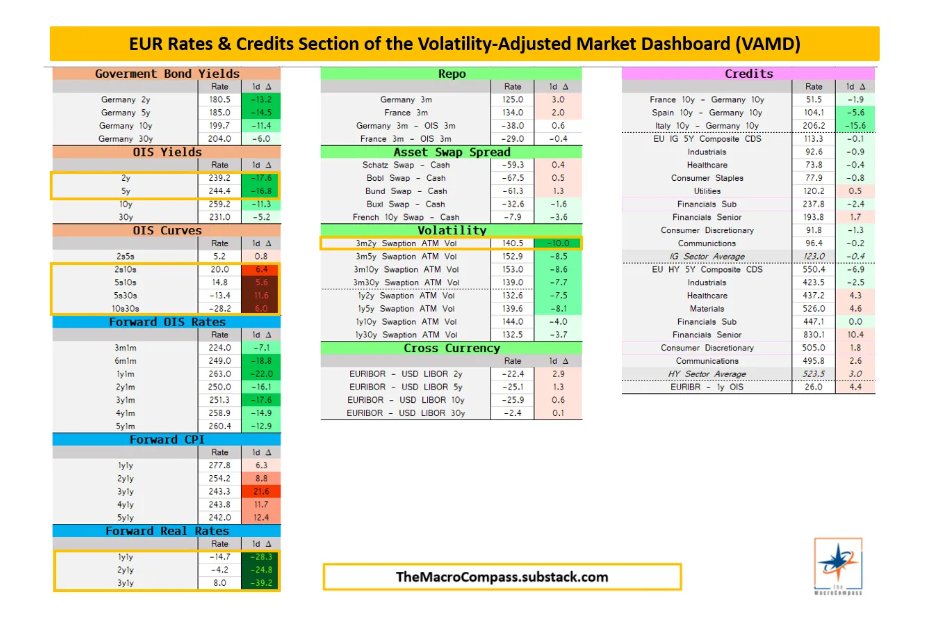

To grasp (the bond) market reaction to the ECB meeting is through a visual snapshot of the Rates & Credits section of my Volatility-Adjusted Market Dashboard (VAMD)

Daily changes are color-coded to reflect the magnitude of the move: the darker the color, the bigger the move

15/

Daily changes are color-coded to reflect the magnitude of the move: the darker the color, the bigger the move

15/

1) Lower front-end rates

2) Lower front-end bond volatility

3) Steeper yield curves

4) Much, much lower (forward) real rates

It all makes sense, let's see why.

16/

2) Lower front-end bond volatility

3) Steeper yield curves

4) Much, much lower (forward) real rates

It all makes sense, let's see why.

16/

If the ECB will be more reluctant to tighten monetary policy further even if CPI is still running at 10%, I have to:

A) Price that in via lower short-end bond yields (and volatility), but assign a bigger risk (term) premia to inflation persisting over time = steeper curves

17/

A) Price that in via lower short-end bond yields (and volatility), but assign a bigger risk (term) premia to inflation persisting over time = steeper curves

17/

B) Forward real yields will be lower, as the ECB commitment to have a tighter monetary stance prolonged over time has materially dropped.

Now, what does this mean for portfolio allocations - especially if other Central Banks (Fed?!) experience a similar change of heart?

18/

Now, what does this mean for portfolio allocations - especially if other Central Banks (Fed?!) experience a similar change of heart?

18/

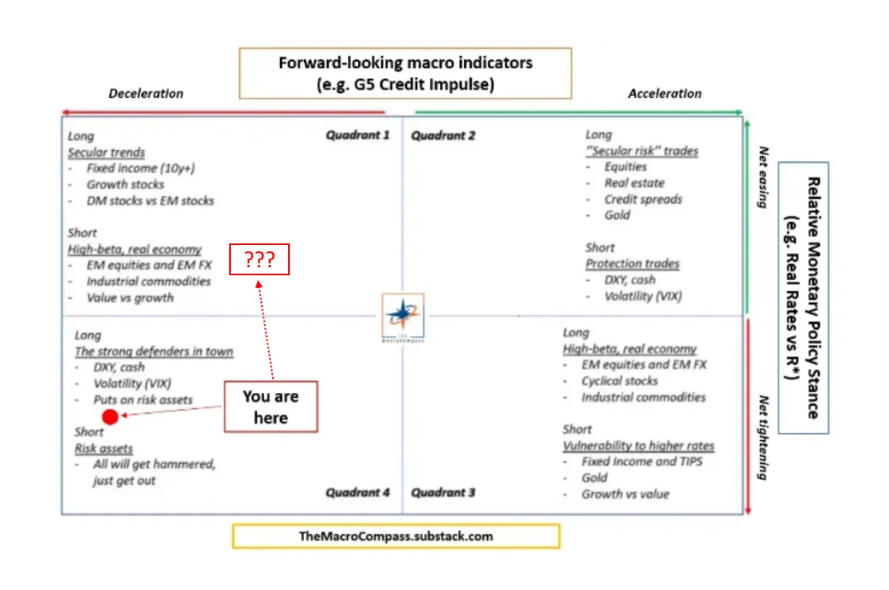

Using the Macro Compass quadrant framework, that would materially increase the probability of a move from Quadrant 4 to Quadrant 1 - at least on the margin.

Lowering the pace of tightening and ending up at ''tight but not incredibly tight'' move you North in the Compass.

19/

Lowering the pace of tightening and ending up at ''tight but not incredibly tight'' move you North in the Compass.

19/

As forward-looking macro indicators don't improve, that means you end up in Quadrant 1.

In this particular iteration of Quadrant 1 transition, bonds and gold could do particularly well.

The Fed is the elephant in the room.

20/

In this particular iteration of Quadrant 1 transition, bonds and gold could do particularly well.

The Fed is the elephant in the room.

20/

I personally don't believe the Fed can follow through on this ''change of heart'': the labor market is way too strong, and there has been no major progress on the (backward looking) inflation indicators they are looking at.

Nevertheless, next week will be really exciting...

21/

Nevertheless, next week will be really exciting...

21/

...and I'll be releasing my analysis of the Fed meeting and market implications immediately after the event on TheMacroCompass.substack.com

It's my newsletter that goes out to 110,000+ macro investors

Consider signing up, so you'll receive it directly in your inbox

It's free

22/22

It's my newsletter that goes out to 110,000+ macro investors

Consider signing up, so you'll receive it directly in your inbox

It's free

22/22

• • •

Missing some Tweet in this thread? You can try to

force a refresh