E-scooter company Bird trading at $0.24 a share after telling investors on Monday that its financial statements of the past 2.5 years "should no longer be relied upon" and there is "substantial doubt about the Company's ability to continue as a going concern"

🔥🧵

🔥🧵

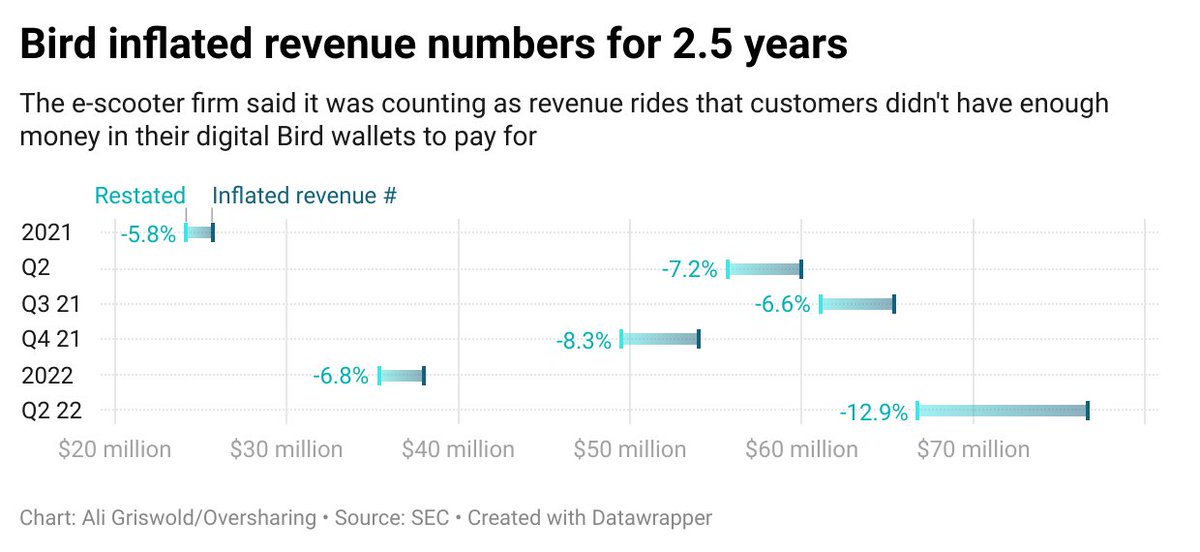

The short version: Bird lets riders pay with preloaded wallet balances ("Bird cash"), much like a gift card or metro card. Sometimes people took rides but didn't have enough Bird cash to pay. Bird recorded the full price of the ride as revenue anyway!

Since Q1 2021, that accounting error has led Bird to inflate revenue by 6-15% per quarter

Q1 21: $25.7mn ⟶ $24.2mn

Q2 21: $60mn ⟶ $55.7mn

Q3 21: $65.4mn ⟶ $61.1mn

Q4 21: $54mn ⟶ $49.5mn

Q1 22: $38mn ⟶ $35.4mn

Q2 22: $76.7mn ⟶ $66.8mn

Q1 21: $25.7mn ⟶ $24.2mn

Q2 21: $60mn ⟶ $55.7mn

Q3 21: $65.4mn ⟶ $61.1mn

Q4 21: $54mn ⟶ $49.5mn

Q1 22: $38mn ⟶ $35.4mn

Q2 22: $76.7mn ⟶ $66.8mn

(I started this thread and then paused to make that chart, because what isn't better with a good chart)

This is hilariously the same company whose co-founder and former CEO accused @coryweinberg of "fake news" for reporting that Bird burned $100 million in a single quarter back in 2019 theinformation.com/articles/hit-b…

https://twitter.com/travisv/status/1149762439593861120

(Travis V also clapped back to The Information's reporting with one of my favorite axis-less charts, or as @FTAlphaville calls them, AXES OF EVIL)

https://twitter.com/travisv/status/1149762561807548416

🚨 brief thread interlude to say that when this site goes up in flames—and now I'm talking about Twitter not Bird, though really it's a banner week for bad accounting and companies with bird-themed brands—you can find me on Substack at oversharing.substack.com

Ok back to Bird:

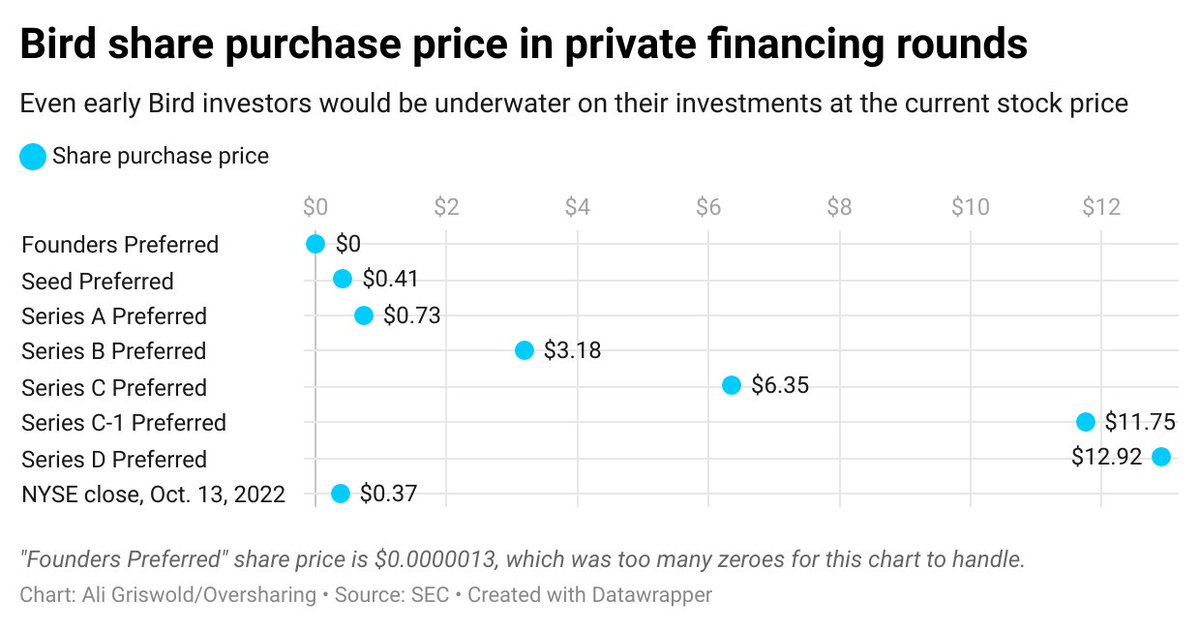

Bird's current market cap is $70mn. That's the least it's been valued at since its Series A funding in February 2018

I didn't bother to update this chart because a penny stock is a penny stock, but suffice it to say that Bird investors are doing quite badly

Bird's current market cap is $70mn. That's the least it's been valued at since its Series A funding in February 2018

I didn't bother to update this chart because a penny stock is a penny stock, but suffice it to say that Bird investors are doing quite badly

Before going public via SPAC, Bird raised $2.1bn from private investors. Billion with a b.

Bird is now worth just 3% of all that VC funding.

Bird is now worth just 3% of all that VC funding.

If Bird goes bust, I hope Silicon Valley reflects on how hype, momentum, and cult of personality drive investing decisions. I hope they look at Bird and wonder, what if some of that money went to local transit systems? To existing public infrastructure? To more diverse founders?

What if we used the substantial firepower of Silicon Valley to invest in our urban landscapes where there are clear needs—public transit, clean water, affordable housing (don't get me started on Adam Neumann)—instead of to fund the pipedreams of an insular cadre of tech bros?

If you liked this 🔥🧵 and want to stay in touch after the Twitterpocalypse, sign up for my newsletter Oversharing

oversharing.substack.com/p/bird-brain

oversharing.substack.com/p/bird-brain

• • •

Missing some Tweet in this thread? You can try to

force a refresh