A thread on IRFC.

You may find something which you have not seen elsewhere.

(1/n)

As per agreement with Ministry of railways (MoR), IRFC is allowed to charge 0.35%/0.40% over its cost of funds.

#irfc

You may find something which you have not seen elsewhere.

(1/n)

As per agreement with Ministry of railways (MoR), IRFC is allowed to charge 0.35%/0.40% over its cost of funds.

#irfc

(2/n)

Cost of Fund includes hedging costs also. Any gain/(loss) on unhedged portion is also pass through and included in the CoF for charging to MoR.

IRFC’s margin is protected at 0/35%/0.40%. neither more nor less is allowed by MoR.

Cost of Fund includes hedging costs also. Any gain/(loss) on unhedged portion is also pass through and included in the CoF for charging to MoR.

IRFC’s margin is protected at 0/35%/0.40%. neither more nor less is allowed by MoR.

(3/n)

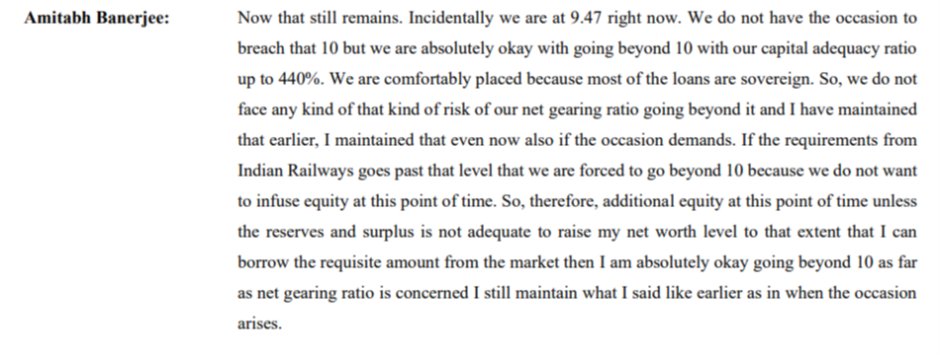

Owing to zero credit loss and zero risk weight on its MoR exposure, technically there is no upper limit on gearing ratio which IRFC is allowed to run.

Historically IRFC always maintained gearing of less than 10

However, management is ok if gearing ratio goes beyond 10x

Owing to zero credit loss and zero risk weight on its MoR exposure, technically there is no upper limit on gearing ratio which IRFC is allowed to run.

Historically IRFC always maintained gearing of less than 10

However, management is ok if gearing ratio goes beyond 10x

(4/n)

With gearing of 10x, IRFC can generate max RoE of CoF+4.4%.

With CoF of 6% it can generate RoE of 10.4%.

With CoF of 8%, it can generate RoE of 12.4%.

With gearing of 10x, IRFC can generate max RoE of CoF+4.4%.

With CoF of 6% it can generate RoE of 10.4%.

With CoF of 8%, it can generate RoE of 12.4%.

(5/n)

For earning higher RoE:

1. IRFC needs to increase the margin it charges on its loan

or

2. increase the gearing ratio.

With gearing ratio of 20x and 30x, the RoE will improve significantly

For earning higher RoE:

1. IRFC needs to increase the margin it charges on its loan

or

2. increase the gearing ratio.

With gearing ratio of 20x and 30x, the RoE will improve significantly

(6/n)

Historically, the gearing was always within 10x. Still IRFC reported RoE higher than what is possible as per margin it is allowed to charge.

FY21 onwards RoE is more than 13%.

Historically, the gearing was always within 10x. Still IRFC reported RoE higher than what is possible as per margin it is allowed to charge.

FY21 onwards RoE is more than 13%.

(7/n)

The question related to this anomaly was asked in one of the con-call but the management couldn’t give any satisfactory answer to this.

The question related to this anomaly was asked in one of the con-call but the management couldn’t give any satisfactory answer to this.

(8/n)

The same point was discussed in valuepickr forum. But still remains unanswered there.

The same point was discussed in valuepickr forum. But still remains unanswered there.

(9/n)

There is no doubt that IRFC is well positioned on

•Loan growth - large railway capex

•Credit quality - MoR exposure

•Cost to Income ratio – do not need much opex

•Competition – Monopoly

•Asset liability mismatch – All borrowings of IRFC are guaranteed by GoI

There is no doubt that IRFC is well positioned on

•Loan growth - large railway capex

•Credit quality - MoR exposure

•Cost to Income ratio – do not need much opex

•Competition – Monopoly

•Asset liability mismatch – All borrowings of IRFC are guaranteed by GoI

(10/n)

But if RoE < cost of capital, it can’t create wealth for investors

If business is generating only 10% RoE, it can't compound earnings faster

Company is reporting RoE in excess of 14%. But this is not reconciling with the business details, especially FY21 onwards

But if RoE < cost of capital, it can’t create wealth for investors

If business is generating only 10% RoE, it can't compound earnings faster

Company is reporting RoE in excess of 14%. But this is not reconciling with the business details, especially FY21 onwards

(11/n)

There is a possible reason for the mismatch.

Company’s numbers for FY20 onwards are not yet reconciled by MoR.

During MoR reconciliation audit if they find that IRFC has billed them higher amount than what is allowed as per agreement, they will ask for reversal.

There is a possible reason for the mismatch.

Company’s numbers for FY20 onwards are not yet reconciled by MoR.

During MoR reconciliation audit if they find that IRFC has billed them higher amount than what is allowed as per agreement, they will ask for reversal.

(12/n)

In previous years, MoR disallowed significant revenue billings which impacted the previous year numbers.

In previous years, MoR disallowed significant revenue billings which impacted the previous year numbers.

(13/n)

On account of MoR reconciliation exercise, IRFC restated the FY20 numbers retrospectively.

On account of MoR reconciliation exercise, IRFC restated the FY20 numbers retrospectively.

(14/n)

Auditors noted this prior period adjustment in their report

Auditors noted this prior period adjustment in their report

(15/n)

It is possible that once MoR completes its reconciliation for FY21, FY22 and FY23, the numbers are restated retrospectively such that actual profit earned in these years is closer to RoE of 10% and not what is reported currently.

It is possible that once MoR completes its reconciliation for FY21, FY22 and FY23, the numbers are restated retrospectively such that actual profit earned in these years is closer to RoE of 10% and not what is reported currently.

(16/n)

Momentum investors can happily play the momentum till it last.

But fundamental investors should provide due consideration to the risk highlighted in this thread.

-end-

Momentum investors can happily play the momentum till it last.

But fundamental investors should provide due consideration to the risk highlighted in this thread.

-end-

• • •

Missing some Tweet in this thread? You can try to

force a refresh