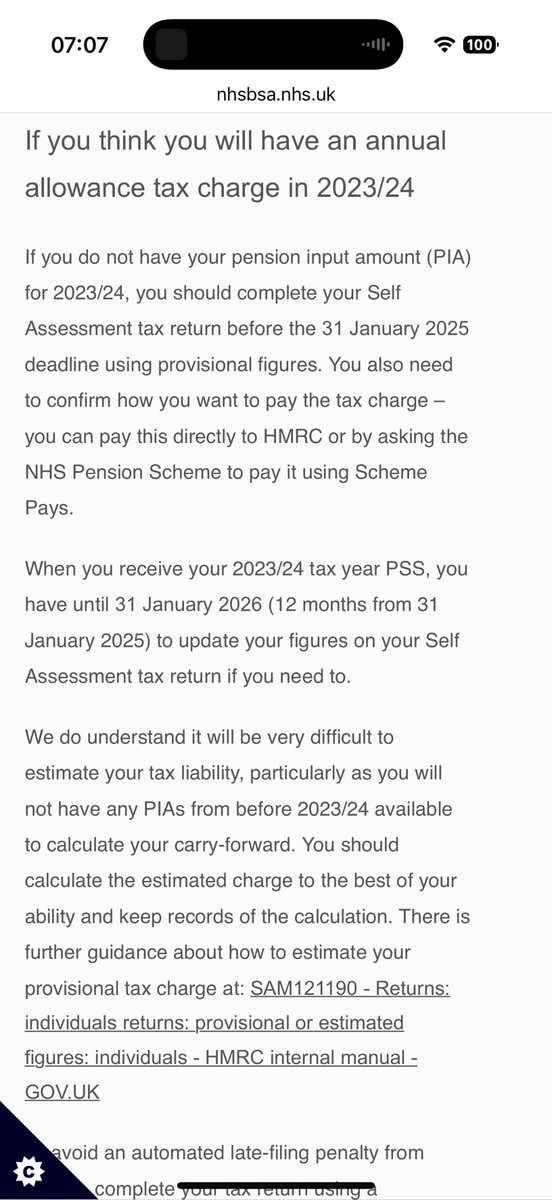

1/ This is a *really* important thread🧵 re current pensions consultation. I need you to take time to read it properly & watch the 2 videos / modelling done with @gdcuk

They are trying to steal your pension, whilst pretending they are fixing a problem. Read, 👀 2 videos & RT

They are trying to steal your pension, whilst pretending they are fixing a problem. Read, 👀 2 videos & RT

2/ Ive been tweeting for some some time now about the *huge* problems created for NHS pension by high inflation & the interaction with something called #CPIdisconnect & #FixNegativePIAs

https://twitter.com/goldstone_tony/status/1530483691960541191?s=20&t=rIAd2Pt7j9J00XOZsFr-eA

3/ Ive always been clear that we need to #FixTheFinanceAct specifically in relation to CPI disconnect (Section 235)

https://twitter.com/goldstone_tony/status/1530483835481341958?s=20&t=rIAd2Pt7j9J00XOZsFr-eA

4/ and also crucially to negative pension growth caused in S234.

To not fix this is tantamount to "pension theft"

To not fix this is tantamount to "pension theft"

https://twitter.com/goldstone_tony/status/1530483841525334018?s=20&t=rIAd2Pt7j9J00XOZsFr-eA

5/ Earlier in the week, Government announced to great fanfare that they had fixed the issues so "clinicians don't feel like they need to take earlier retirement or reduce hours"

https://twitter.com/SteveBarclay/status/1599713767683952640?s=20&t=KEMW_dnxfUoyRymvIDdalQ

6/ SPOILER ALERT: They havent fixed this at all, especially in some groups (just read the comments now including around 200 GPs & consultants)

https://twitter.com/SteveBarclay/status/1599713767683952640?s=20&t=KEMW_dnxfUoyRymvIDdalQ

7/ Ive recorded a short video talking about the issues of CPI disconnect and introducing the complex concept of negative pension growth

*PLEASE* take the 20mins time to watch it (best view HD on a computer)

*PLEASE* take the 20mins time to watch it (best view HD on a computer)

8/ In that video I talk at length about this slide about the interaction between 4 factors each year:

- September CPI

- "Opening value"

- Pay awards

- "Revaluation"

Government have proposed at best a partial fix to inflation related problems

- September CPI

- "Opening value"

- Pay awards

- "Revaluation"

Government have proposed at best a partial fix to inflation related problems

9/ Next we look at an article from @thetimes in which Secretary of State @SteveBarclay discusses the consultation announced later that day

10/ In that article Mr. Barclay gives a (somewhat exaggerated) example which could imply doctors can earn pensionable income of £174k (not many doctors around earning that) with virtually no AA charges thanks to the "fix"

11/ But in the next video, pensions expert @gdcuk reverse engineers that case to show that not all is quite as it seems with what Mr. Barclay implies

Again take time to watch this video in detail (ideally in HD on a computer)

Again take time to watch this video in detail (ideally in HD on a computer)

12/ The tax charge is not £ 628 as Mr. Barclay implies, but rather £ 5,811 - but in any event its a highly unusual tax year (22/23) as its the only tax year ever (or future) where there is no "revaluation/dynamization" as they have been moved back 6 days to next tax year

13/ But more importantly the selective case studies masks the ENORMOUS pension theft which happens in future years with MASSIVE negative pension loss (£100k in 23/24 and 85k in 24/25).

14/ This changes the 4 year pension liability from £39,971 to *ZERO* - as in NADA / NOTHING / ZILCH if negative pension growth is calculated, not ignoring negative growth - i.e. measuring *REAL* growth above inflation.

15/ Next we look at the effect of doing some "extra work" to help with the 7.2m waiting list - doing 12 PAs, and only 1 8 hour list per month at @TheBMA rates pushes that pension tax charge to 76k - higher by 36k for *ABSOLUTELY NO PENSION BENEFIT*. Just scandalous

16/ Unsurprisingly a higher earning member like Mr. Barclay cases study might be advised to drop the waiting list work, and indeed go from 12 PAs to less - and thats no suprise as it might make complete financial sense to do so to not #PayingToWork

17/ In the video next @gcduk and I look at a much more realistic case (remembering this was Mr. Barclays case, not mine or @TheBMA at look at a more realistic mid career consultant example

18/ We also look forward 10 years in this case and just look at the difference looking at negative PIAs (with carry forward) can make

19/ Over 10 years the pension tax charge is £68,498 - but counting negative pension growth i.e. *ACTUALLY* measuring *REAL* growth above inflation that falls to £19,763 - some £48,735 lower

20/ Just process that for a minute - they ignore the *MASSIVE* pension loss caused by subinflationary pay in tax years 23/24 and 24/25 (yellow) & instead of processing this fairly to measure real growth above inflation (green) they "zero" this off (red) and ignore it

21/ The net result is that you *MASSIVELY* overpay tax. And as its highly likely you cant afford to pay these AA charges from net income / savings, you are then forced to use expensive scheme pays loans based on inflation + 2.4% - despite your 1995 pension deflating, *massively*

22/ If you are not angry by this pension theft, which is what this is tantamount to, you may not have understood the problem as its complicated. If so *please* take the time to learn about this, and watch all the videos above, in detail.

23/ If you think this is me or the @BMA_Pensions moaning about something pretty niche, you are wrong. We are not the only ones jumping up and down about this, see what @Policy_Exchange @NHSEmployers @AISMANewsline have also called for in recent months, as well as Dr. Dan Poulter

24/ Government cannot on one hand claim in the consultation that the intention of government is to "only measure growth above inflation".

They are doing nothing of the sort, and in the process they are massively & unfairly decreasing your pension

They are doing nothing of the sort, and in the process they are massively & unfairly decreasing your pension

25/ Our new chancellor @Jeremy_Hunt knows this is a problem

#FixTheFinanceAct #FixNegativePIAs #TaxUnregistered

Its time to fix this properly, before its too late

RT if you are fed up with them robbing your pension & destroying the NHS

#FixTheFinanceAct #FixNegativePIAs #TaxUnregistered

Its time to fix this properly, before its too late

RT if you are fed up with them robbing your pension & destroying the NHS

https://twitter.com/Jeremy_Hunt/status/1555139559796912128?s=20&t=pMSUAs8iWGyVXI7VOljZtg

• • •

Missing some Tweet in this thread? You can try to

force a refresh