"You should NEVER hold a levered ETF unless you are day trading!!!"

We've all heard this advice, but is it really true? Let's dig in.

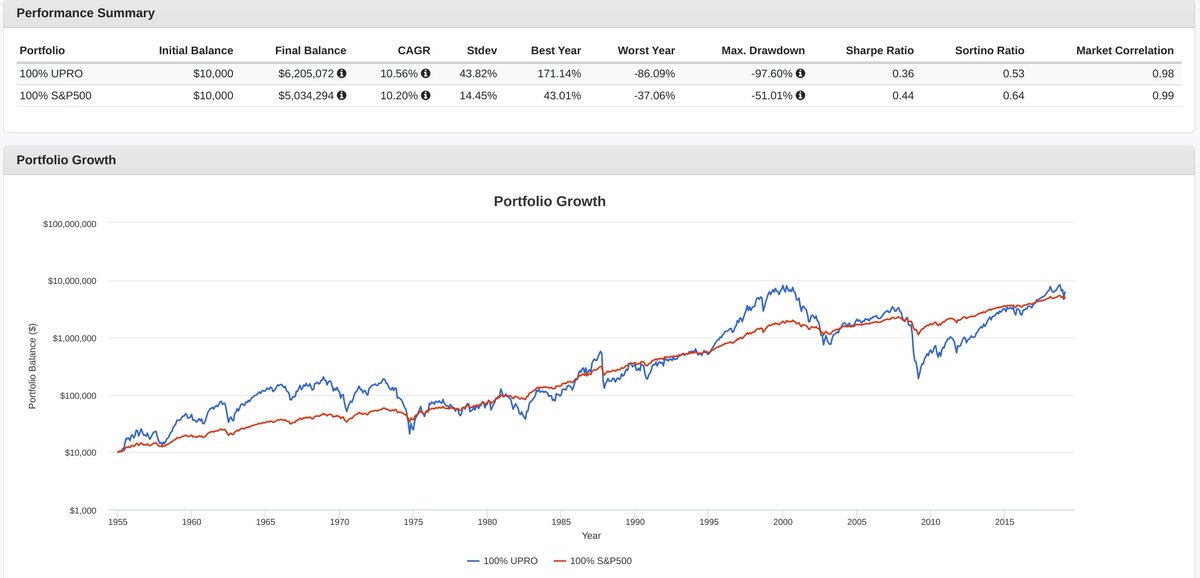

Sure, you shouldn't go 100% into $UPRO... you'll end up matching the S&P500, but with nearly 100% drawdowns and crazy volatility. (cont)

We've all heard this advice, but is it really true? Let's dig in.

Sure, you shouldn't go 100% into $UPRO... you'll end up matching the S&P500, but with nearly 100% drawdowns and crazy volatility. (cont)

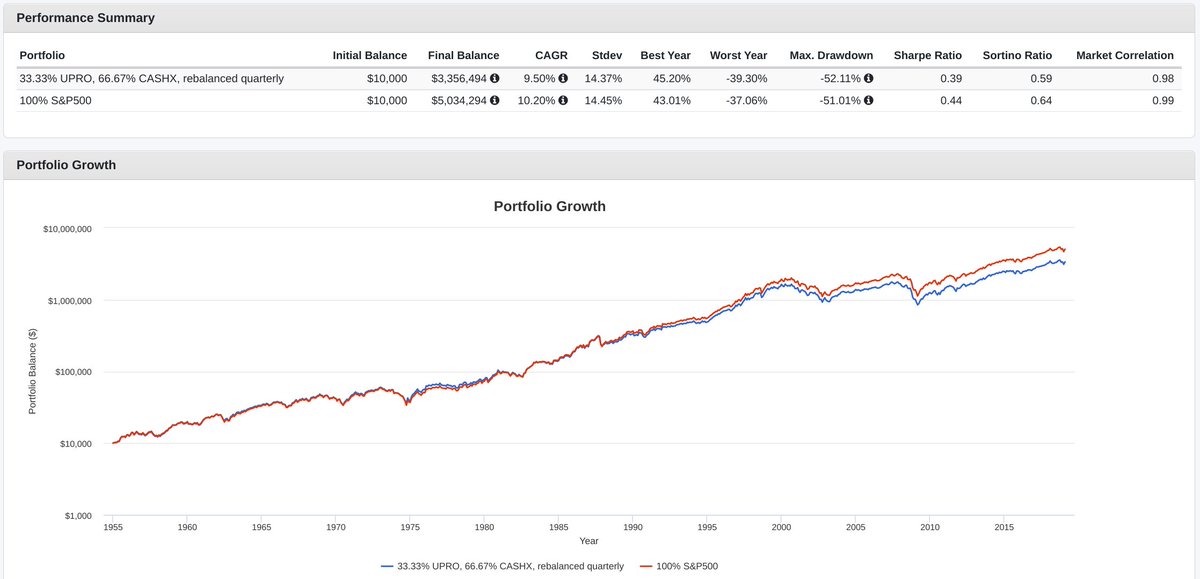

But what if you just use a 1/3 allocation to achieve an effective 100% exposure to the S&P500, while freeing up 2/3 for other assets?

Between the vol-decay and higher fees, the drag isn't all that bad... But it would be pretty silly to do this just to hold 2/3s in cash... (cont)

Between the vol-decay and higher fees, the drag isn't all that bad... But it would be pretty silly to do this just to hold 2/3s in cash... (cont)

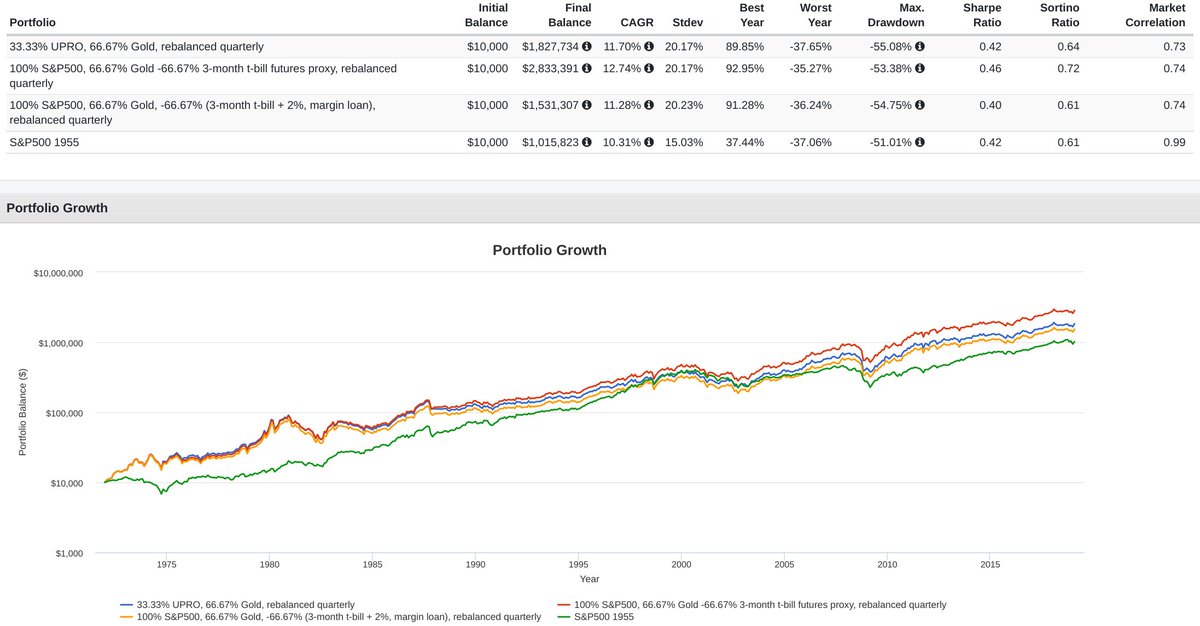

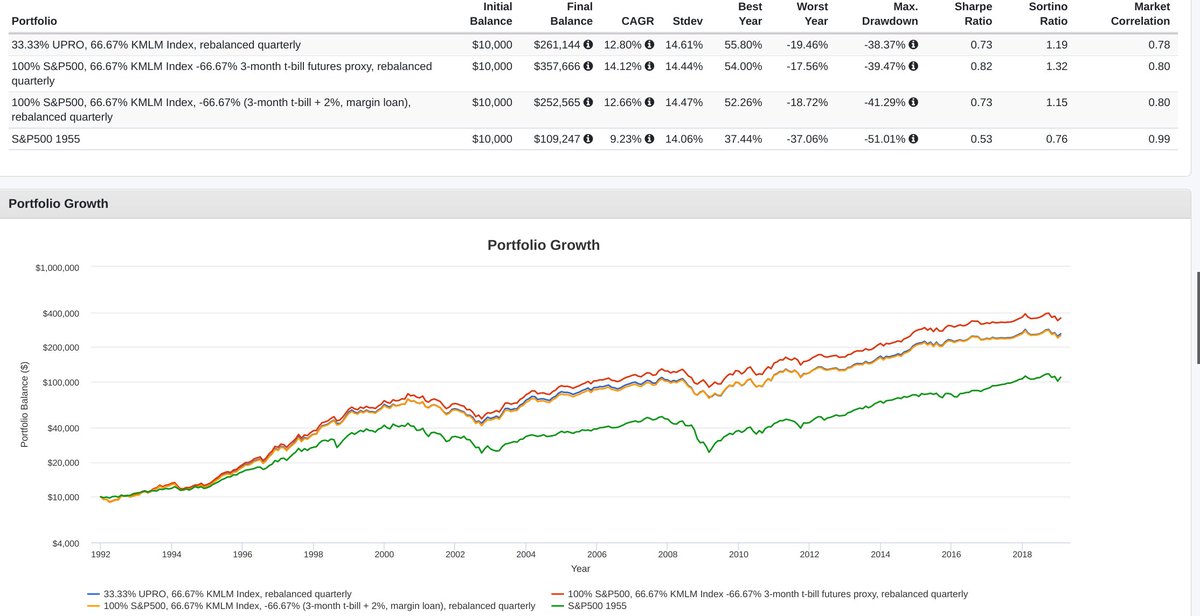

Each of these plots will compare 3 ways to get 100% S&P500 with 66.7% of an additional asset stacked on top :

1: 33.3% UPRO, 66.7% XYZ

2: 100% S&P500, 66.7% XYZ, -66.7% 3-month rate (futures proxy)

3: 100% S&P500, 66.7% XYZ, -66.7% 3-month rate plus 2% (margin proxy)

4: S&P

1: 33.3% UPRO, 66.7% XYZ

2: 100% S&P500, 66.7% XYZ, -66.7% 3-month rate (futures proxy)

3: 100% S&P500, 66.7% XYZ, -66.7% 3-month rate plus 2% (margin proxy)

4: S&P

Lets start with the oldest store of value there is... gold!

Prefer cashflow generating assets? How about some long-term US treasuries!

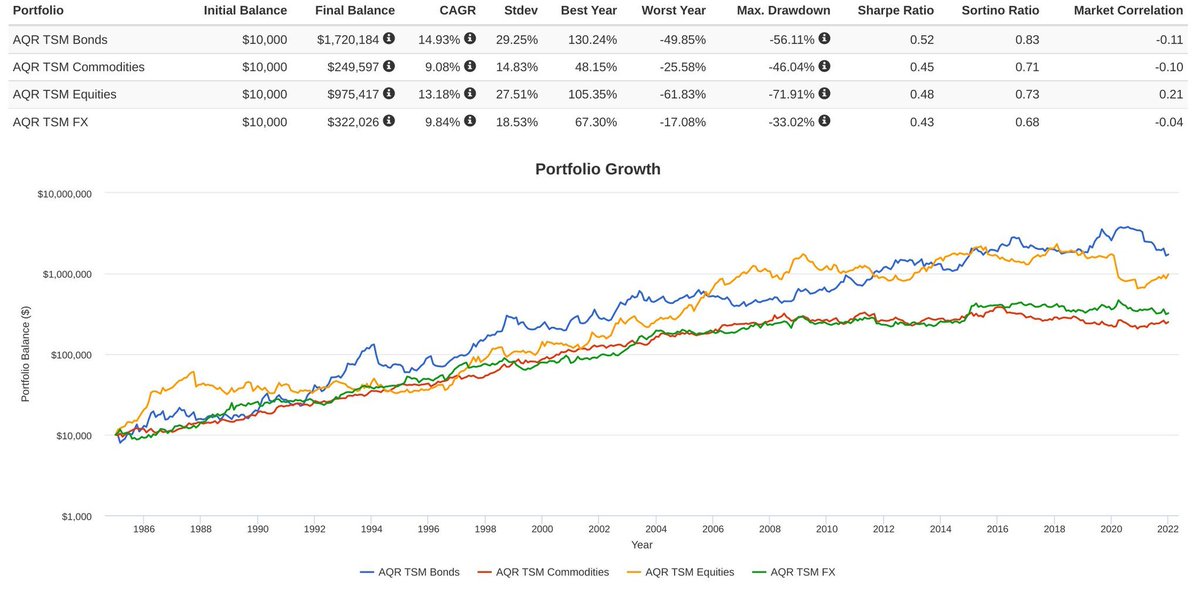

Like to hold a more diverse basket of assets both long and short, and use trend to determine positions? How about the Mt Lucas index net of 85bp to represent $KMLM?!

Another trend based index from AQR to get a bit further back in time.

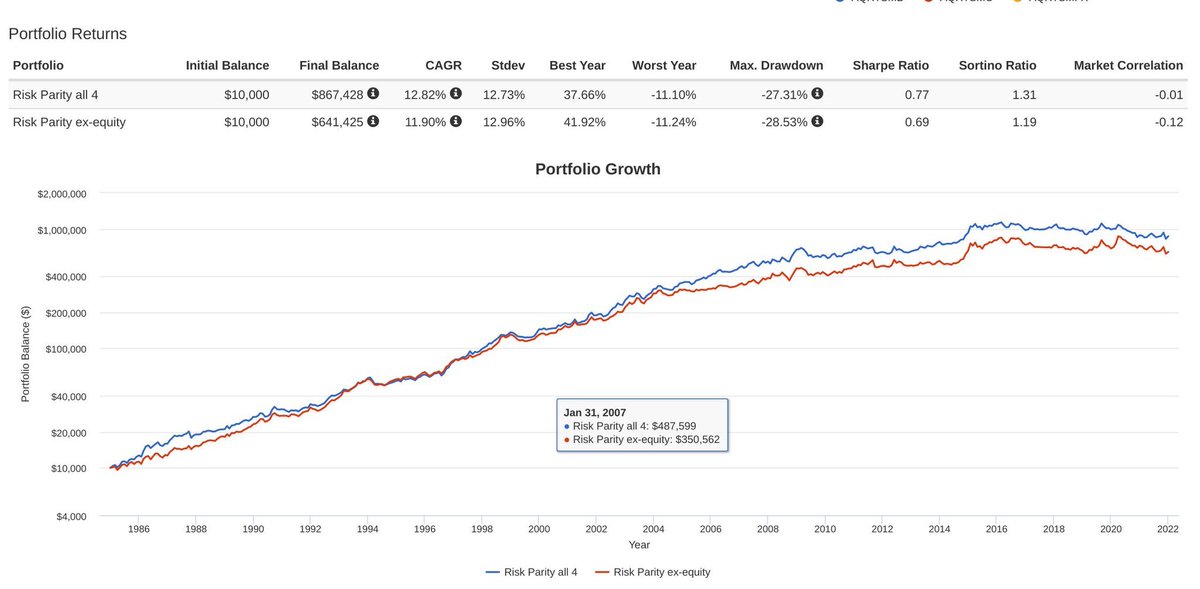

Too boring and you need more risk? Okay I doubt anyone really wants this portfolio but how about adding 2/3 stack of US small-value!?

75% drawdown, woof!

75% drawdown, woof!

None of these backtests are intended to represent actual returns you can expect moving forward, and in some cases not even what you could've got in the past (no trading costs in KMLM index, no costs at all in AQR), but they do show the potential relative utility of UPRO (cont)

In fact, in all cases it outperformed a traditional margin loan with a borrowing rate 2% above the 3-month t-bill, not bad at all, and you can even implement this in a retirement account! (cont)

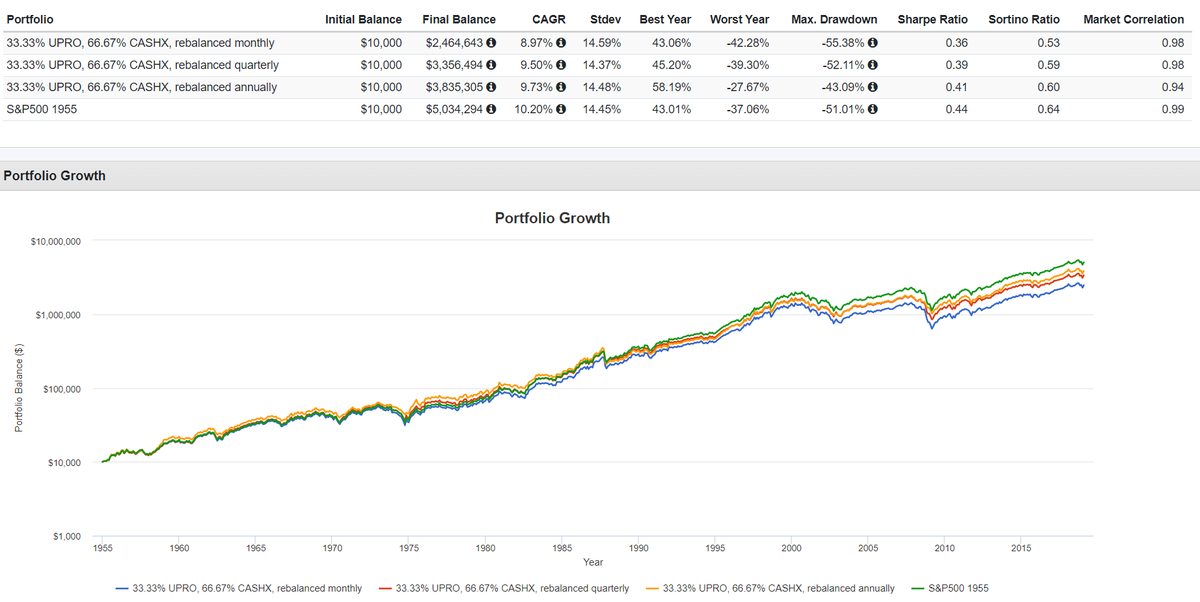

Does rebalance timing matter? Yes, but that is true of any portfolio, levered or not. Not shown, but rebalance bands may be most appropriate.

Last but not least, here is monthly rebalance between 33.33% UPRO, 66.67% 3-month t-bill, and -100% S&P500 to show the rolling drag.

Neat read on short gamma effect here (H/T @game_book_life):

moontowermeta.com/the-gamma-of-l…

Neat read on short gamma effect here (H/T @game_book_life):

moontowermeta.com/the-gamma-of-l…

What would you fill your 2/3 with? I bet @NomadicSamuel has some fun ideas!

• • •

Missing some Tweet in this thread? You can try to

force a refresh