NEW FROM US:

Block—How Inflated User Metrics and "Frictionless" Fraud Facilitation Enabled Insiders To Cash Out Over $1 Billion

hindenburgresearch.com/block $SQ

(1/n)

Block—How Inflated User Metrics and "Frictionless" Fraud Facilitation Enabled Insiders To Cash Out Over $1 Billion

hindenburgresearch.com/block $SQ

(1/n)

Block, formerly known as Square, is a ~$44 billion market cap company that claims to have developed a “frictionless” and “magical” financial technology with a mission to empower the “unbanked” and the “underbanked”. $SQ

(2/n)

(2/n)

Our 2-year investigation concludes $SQ systematically exploits the demographics it claims to help. The magic behind $SQ has not been innovation, but its willingness to mislead investors, facilitate fraud, avoid regulation & dress up predatory products as revolutionary tech. (3/n)

Our research involved dozens of interviews with former employees, partners, and industry experts, extensive review of regulatory and litigation records, and FOIA and public records requests. (4/n)

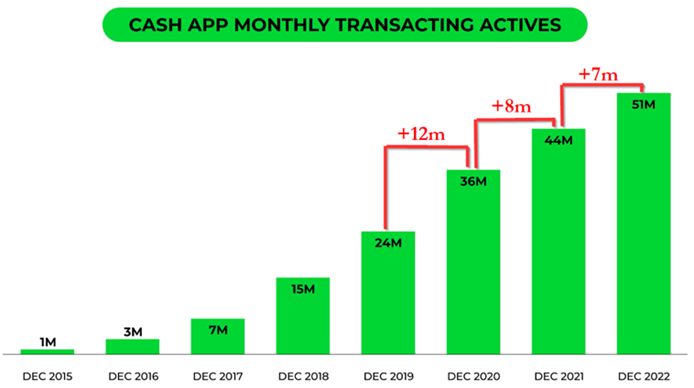

Most analysts are excited about the post-pandemic surge of $SQ's Cash App platform, with expectations its 51 million monthly transacting active users and low customer acquisition costs will drive high margin growth and serve as a future platform to offer new products. (5/n)

Our research shows $SQ has wildly overstated genuine user counts & understated customer acquisition costs for years.

Former employees evidenced that many users have dozens, or even hundreds of accounts associated with them, vastly inflating user metrics. (6/n)

Former employees evidenced that many users have dozens, or even hundreds of accounts associated with them, vastly inflating user metrics. (6/n)

Block obfuscates how many unique individuals use Cash App, reporting misleading metrics on "transacting actives" which include duplicate accounts by the same user.

Former employees estimated that 40%-75% of accounts they reviewed were fake, involved in fraud or duplicates. (7/n)

Former employees estimated that 40%-75% of accounts they reviewed were fake, involved in fraud or duplicates. (7/n)

$SQ has embraced one very underbanked segment: criminals. When users were caught engaging in fraud, $SQ would blacklist the account but not ban the user.

Former employees showed us blacklisted accts associated w/dozens or hundreds of other live accounts suspected of fraud. (8/n)

Former employees showed us blacklisted accts associated w/dozens or hundreds of other live accounts suspected of fraud. (8/n)

CEO Dorsey has touted how Cash App is in hundreds of hip hop songs as evidence of its appeal.

But artists are not rapping about Cash App’s smooth user interface — many describe using it to scam, traffic drugs or even pay for murder. (9/n)

But artists are not rapping about Cash App’s smooth user interface — many describe using it to scam, traffic drugs or even pay for murder. (9/n)

“I paid them hitters through Cash App”— Block even paid to promote a video for a song called “Cash App” which described paying contract killers through the app.

The song’s artist was later arrested for attempted murder. (10/n)

The song’s artist was later arrested for attempted murder. (10/n)

Cash App was cited “by far” as the top app used in U.S. sex trafficking, according to a leading non-profit organization.

Multiple Department of Justice complaints outline how Cash App has been used to facilitate sex trafficking, including sex trafficking of minors. (11/n)

Multiple Department of Justice complaints outline how Cash App has been used to facilitate sex trafficking, including sex trafficking of minors. (11/n)

There is even a gang named after Cash App: In 2021, Baltimore authorities charged members of the “Cash App” gang with distribution of fentanyl in a West Baltimore neighborhood, according to news reports and criminal records. (12/n)

Beyond facilitating payments for criminal activity, the platform has been overrun with scam accounts & fake users, according to interviews with former employees.

The phenomenon of allowing blacklisted users was so common that rappers bragged about it popular songs. (13/n)

The phenomenon of allowing blacklisted users was so common that rappers bragged about it popular songs. (13/n)

Examples of obvious distortions abound: “Jack Dorsey” has multiple fake accounts, including some that appear aimed at scamming Cash App users.

“Elon Musk” and “Donald Trump” had dozens. (14/n)

“Elon Musk” and “Donald Trump” had dozens. (14/n)

To test this, we turned our accounts into “Donald Trump” and “Elon Musk” and were easily able to send and receive funds. (15/n)

Taking it a step further, we ordered a Cash Card under our obviously fake persona, checking to see if Block’s compliance would take issue.

We promptly received our Donald J. Trump Cash Card in the mail. (16/n)

We promptly received our Donald J. Trump Cash Card in the mail. (16/n)

Former employees described how Cash App suppressed internal concerns and ignored user pleas for help as criminal activity and fraud ran rampant on its platform.

This appeared to be an effort to grow Cash App’s user base by disregarding AML rules. (17/n)

This appeared to be an effort to grow Cash App’s user base by disregarding AML rules. (17/n)

The COVID-19 pandemic and nationwide lockdowns posed an existential threat to Block's key driver of gross profit at the time, merchant services. (18/n)

In this environment, amid Cash App's anti-compliance free-for-all, the app stepped in to facilitate a wave of government COVID-relief payments.

Dorsey Tweeted users could get payments through Cash App “immediately” with “no bank account needed” due to its technology. (19/n)

Dorsey Tweeted users could get payments through Cash App “immediately” with “no bank account needed” due to its technology. (19/n)

Within weeks of Cash App accounts receiving their first government payments, states sought to claw back suspected fraud, former employees told us. (20/n)

Once again, the signs were hard to miss. Rapper “Nuke Bizzle”, made a popular music video about committing COVID fraud.

Weeks later, he was arrested and eventually convicted for committing COVID fraud. The only P2P payment provider mentioned in the indictment: Cash App. (21/n)

Weeks later, he was arrested and eventually convicted for committing COVID fraud. The only P2P payment provider mentioned in the indictment: Cash App. (21/n)

We filed public records requests to learn more about Block’s role in facilitating pandemic relief fraud and received answers from several states. (22/n)

Mass. sought to claw back over 69,000 payments from Cash App accounts just 4 months into the pandemic.

Suspect transactions at Cash App’s partner bank exceeded major banks like JP Morgan and Wells Fargo, despite the latter banks having 4x-5x as many deposit accounts. (23/n)

Suspect transactions at Cash App’s partner bank exceeded major banks like JP Morgan and Wells Fargo, despite the latter banks having 4x-5x as many deposit accounts. (23/n)

In Ohio, suspect pandemic-related unemployment payments to Cash App’s partner bank were 8x higher than the largest recipient of claims in the state, even though the competitor processed 2x the claims, according to data we obtained via a public records request. (24/n)

Compared to its Ohio competitor, data shows that Cash App’s partner bank had nearly 10x the number of applicants who applied for benefits through a bank account used by another claimant – a clear red flag of fraud. (25/n)

Block had obvious compliance lapses that enabled fraud, such as permitting single accounts to receive unemployment payments for multiple individuals from various states, and ineffective address verification. (26/n)

In an apparent effort to preserve its growth, Cash App ignored internal employee concerns, along with warnings from the Secret Service, FinCEN & State Regulators which all specifically flagged the issue of multiple payments going to the same account as a sign of fraud. (27/n)

Block reported a pandemic surge in user counts and revenue, ignoring the contribution of widespread fraudulent accounts and payments.

The new business provided a sharp one-time increase to Block’s stock, which rose 639% in 18 months during the pandemic. (28/n)

The new business provided a sharp one-time increase to Block’s stock, which rose 639% in 18 months during the pandemic. (28/n)

As $SQ soared on the back of facilitation of fraud, co-founders Dorsey and James McKelvey collectively sold over $1 billion of stock during the pandemic. Other execs, including CFO Amrita Ahuja and lead manager for Cash App Brian Grassadonia, also dumped millions in stock. (29/n)

With its influx of pandemic Cash App users, our research shows Block has quietly fueled its profitability by avoiding a key banking regulation meant to protect merchants.

“Interchange fees” are fees charged to merchants for accepting use of various payment cards. (30/n)

“Interchange fees” are fees charged to merchants for accepting use of various payment cards. (30/n)

Congress passed a law that legally caps “interchange fees” charged by large banks that have over $10 billion in assets.

Despite having $31 billion in assets, Block avoids these regulations by routing payments through a small bank and gouging merchants with elevated fees. (31/n)

Despite having $31 billion in assets, Block avoids these regulations by routing payments through a small bank and gouging merchants with elevated fees. (31/n)

$SQ includes only vague references in its filings acknowledging it even earns “interchange fees”.

It has never revealed the economics of this category, yet roughly 1/3 of Cash App’s revenue came from this opaque source, according to a 2022 Credit Suisse report. (32/n)

It has never revealed the economics of this category, yet roughly 1/3 of Cash App’s revenue came from this opaque source, according to a 2022 Credit Suisse report. (32/n)

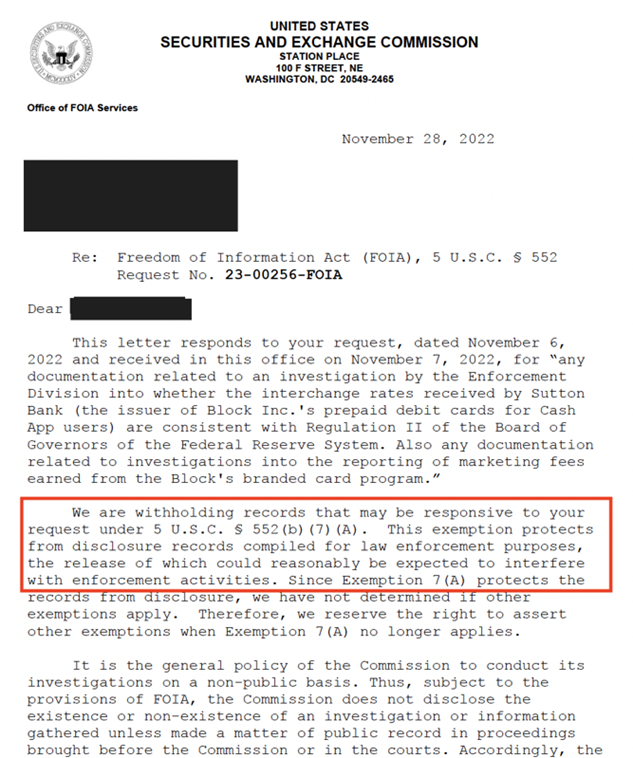

Competitor $PYPL has disclosed it is under investigation by SEC & CFPB over similar use of a small bank to avoid “interchange fee” caps.

A FOIA request we filed with the SEC indicates $SQ may be part of a similar investigation. (33/n)

A FOIA request we filed with the SEC indicates $SQ may be part of a similar investigation. (33/n)

$SQ completed the $29 billion acquisition of ‘buy now pay later’ service Afterpay in 2022.

Block has celebrated Afterpay as a major innovator, allowing users to buy things like a t-shirt and pay over time, only incurring massive fees if payments are late. (34/n)

Block has celebrated Afterpay as a major innovator, allowing users to buy things like a t-shirt and pay over time, only incurring massive fees if payments are late. (34/n)

Afterpay was designed in a way that avoided responsible lending rules in its native Australia, extending a form of credit to users that may have no income or credit.

Afterpay doesn't technically charge "interest", but late fees can reach APR equivalents as high as 289%. (35/n)

Afterpay doesn't technically charge "interest", but late fees can reach APR equivalents as high as 289%. (35/n)

The acquisition is flopping. In 2022, the year Afterpay was acquired, the pro forma combined entity lost $357 million, accelerating from pro forma 2021 losses of $184 million. (36/n)

• • •

Missing some Tweet in this thread? You can try to

force a refresh