Yield curve dynamics are crucial to understand if you want to become a better macro investor.

A thread.

1/ twitter.com/i/web/status/1…

A thread.

1/ twitter.com/i/web/status/1…

Yield curve dynamics represent a crucial macro variable, as they inform us on today’s borrowing conditions and on the market future expectations for growth and inflation.

2/

2/

An inverted yield curve often leads towards a recession because it chokes real-economy agents off with tight credit conditions (high front-end yields) which are reflected in weak future growth and inflation expectations (lower long-dated yields).

3/

3/

A steep yield curve instead signals accessible borrowing costs (low front-end yields) feeding into expectations for solid growth and inflation down the road (high long-dated yields).

4/

4/

Rapid changes in the shape of the yield curve at different stages of the cycle are a key macro variable to understand and incorporate in your portfolio allocation process.

So, let's explore the 4 main yield curve regimes.

5/

So, let's explore the 4 main yield curve regimes.

5/

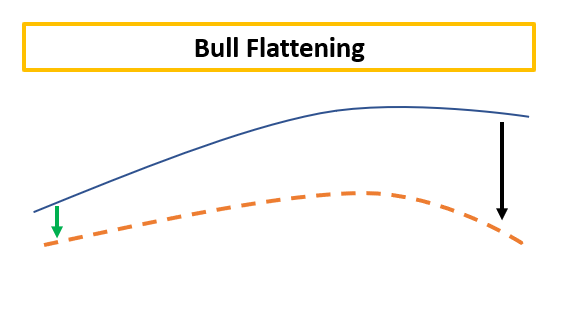

Bull Flattening = lower front-end yields, flatter curves.

Think of 2016: Fed Funds already basically at 0% and weak global growth.

Yields stay put at the front-end and could meaningfully move lower only at the long-end, hence bull-flattening the curve.

6/

Think of 2016: Fed Funds already basically at 0% and weak global growth.

Yields stay put at the front-end and could meaningfully move lower only at the long-end, hence bull-flattening the curve.

6/

When this happens, long bonds do very well and growth stocks tend to overperform value, as tech disproportionately benefits from low interest rates.

Also, 60/40 portfolios deliver great returns!

7/

Also, 60/40 portfolios deliver great returns!

7/

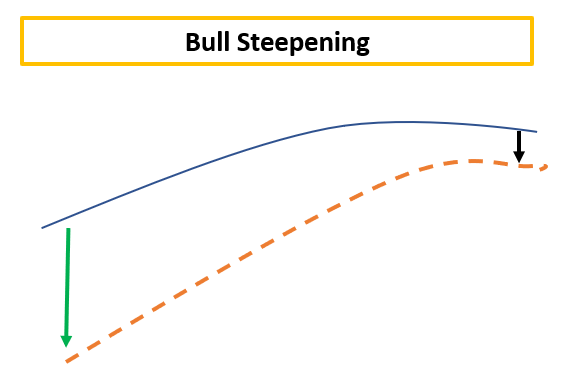

Bull Steepening = lower front-end yields, steeper curves.

Late 2020, early 2021: the Fed was keeping rates pinned at 0% and stimulating via QE but the economy was flooded with fiscal stimulus and ready for reopening.

8/

Late 2020, early 2021: the Fed was keeping rates pinned at 0% and stimulating via QE but the economy was flooded with fiscal stimulus and ready for reopening.

8/

The friendly borrowing conditions and the massive upcoming growth boost could mostly be reflected through higher long-end yields, while 2-year interest rates were pinned at 0% by the Fed.

Bull-steepening of the curve.

9/

Bull-steepening of the curve.

9/

This tends to happen ahead of recessions: short-dated bonds start to price in meaningful Fed cuts in response to weak economic conditions, and they rally harder than long-end bonds.

A transition from a flat curve to a bull steepening is very troublesome for markets.

10/

A transition from a flat curve to a bull steepening is very troublesome for markets.

10/

On the other hand bull steepening can be very positive for markets if accompanied by strong growth.

That means the Fed is keeping policy loose (low front-end yields) and higher growth and inflation expectations feed into the long-end (higher long bond yields).

11/

That means the Fed is keeping policy loose (low front-end yields) and higher growth and inflation expectations feed into the long-end (higher long bond yields).

11/

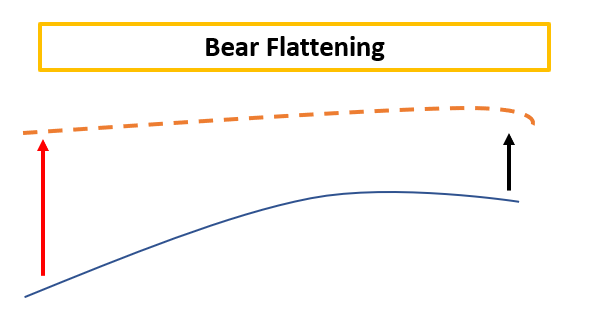

Bear Flattening = higher front-end yields, flatter curves.

2022 was the bear flattening year: Powell raised rates aggressively to fight inflation, but he ended up choking the economy off.

12/

2022 was the bear flattening year: Powell raised rates aggressively to fight inflation, but he ended up choking the economy off.

12/

This was reflected in lower future growth and inflation expectations at the long-end of the curve.

Front-end rates went higher, but the curve bear-flattened

When this happens in conjuction with weaker growth, cyclical stock sectors and tech tend to underperforms (see 2022)

13/

Front-end rates went higher, but the curve bear-flattened

When this happens in conjuction with weaker growth, cyclical stock sectors and tech tend to underperforms (see 2022)

13/

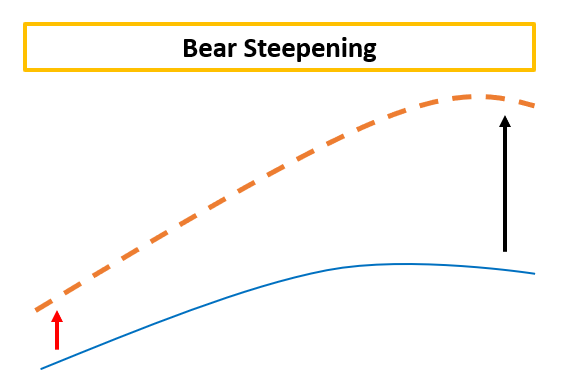

Bear Steepening = higher front-end yields, steeper curves.

Do you remember 2009? The worst of the GFC was behind us and (monetary-mechanics-illiterate) investors were afraid that QE would lead to runaway inflation and the Fed would be forced to start acting on it.

14/

Do you remember 2009? The worst of the GFC was behind us and (monetary-mechanics-illiterate) investors were afraid that QE would lead to runaway inflation and the Fed would be forced to start acting on it.

14/

Front-end yields moved a bit higher, but long-end yields took most of the hit as investors (mistakenly) bumped the inflation risk premium up = the curve bear-steepened.

It's a very rare occurrence, and it is generally associated with higher risk premia.

15/

It's a very rare occurrence, and it is generally associated with higher risk premia.

15/

Rapid changes in the shape of the yield curve when growth is at turning points are a key variable to consider for a successful asset allocation process.

If you enjoyed this thread and want more macro educational content...

16/

If you enjoyed this thread and want more macro educational content...

16/

...you are going to find plenty on TheMacroCompass.com.

I'll be waiting for you to join this macro learning journey!

17/17

I'll be waiting for you to join this macro learning journey!

17/17

• • •

Missing some Tweet in this thread? You can try to

force a refresh