Bharat Wire Ropes Ltd:-

The company is one of the largest manufacturers of Steel Wire Ropes in India. The company is one of the leading manufacturers of speciality steel wires, steel wire ropes, slings and strands, with over thousands of varieties of products.

Industry… twitter.com/i/web/status/1…

The company is one of the largest manufacturers of Steel Wire Ropes in India. The company is one of the leading manufacturers of speciality steel wires, steel wire ropes, slings and strands, with over thousands of varieties of products.

Industry… twitter.com/i/web/status/1…

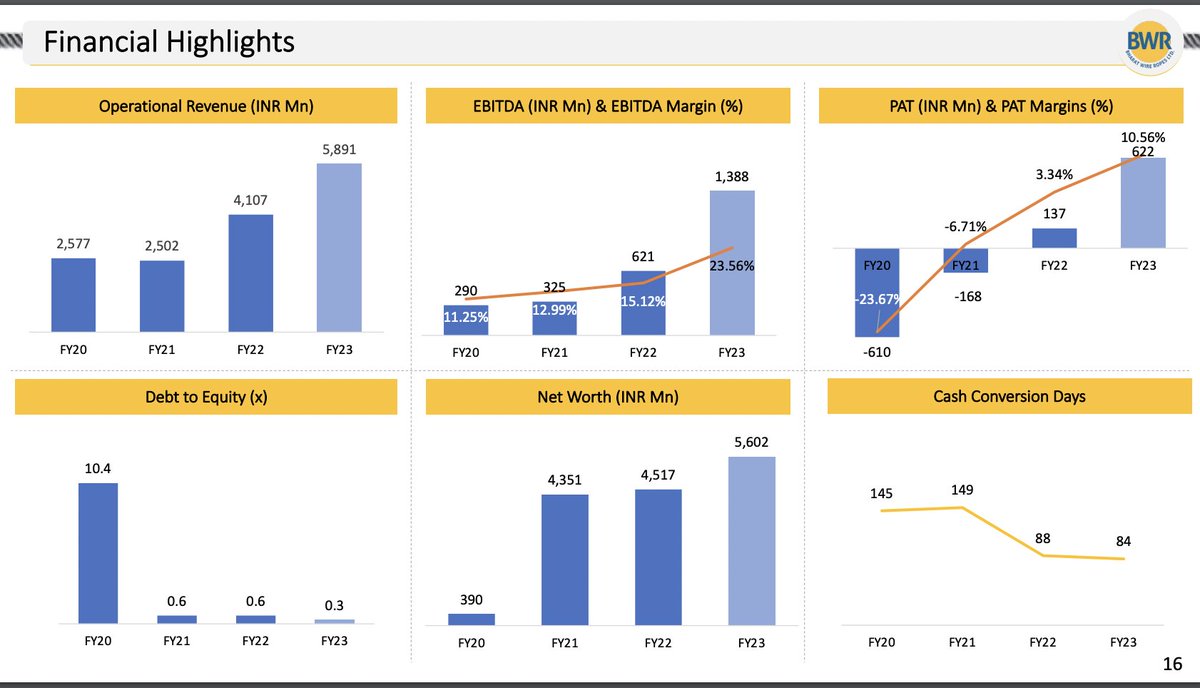

The company has turned around from posting losses of Rs 61 CR in FY20 to posting profits of Rs 62 CR in FY23.

Strong balance sheet with no ALM mismatch. Negligible debt on the books.

Improving cash conversion cycle.

Strong balance sheet with no ALM mismatch. Negligible debt on the books.

Improving cash conversion cycle.

Q4FY23 Con Call Updates:-

1. First ever Con Call with investors

2. The company has machines made in South Korea and Germany that allows Bharat Wires to compete with global manufacturers of Steel wires.

3. The company has transformed in the last few years.

4. Sales volumes up… twitter.com/i/web/status/1…

1. First ever Con Call with investors

2. The company has machines made in South Korea and Germany that allows Bharat Wires to compete with global manufacturers of Steel wires.

3. The company has transformed in the last few years.

4. Sales volumes up… twitter.com/i/web/status/1…

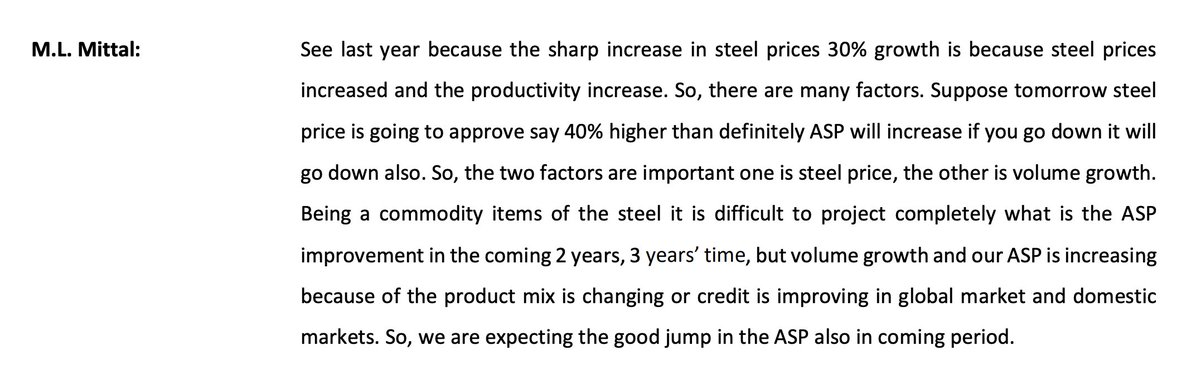

The company is confident of growing Volumes at 15-20% CAGR. However, value growth (realisations) would depend on steel price movements yet the company is improving ASP with improving product mix and selling high-value products.

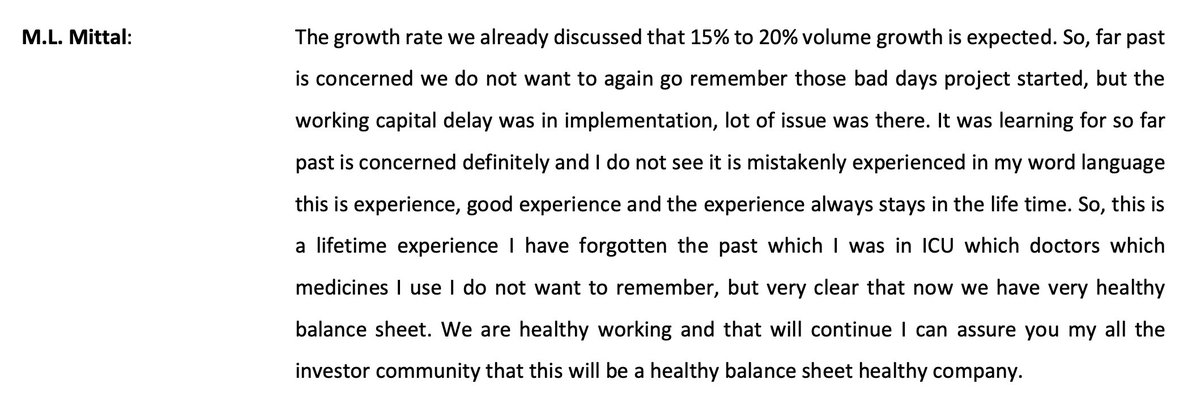

The management wants to forget about the past and move on to better days for the company.

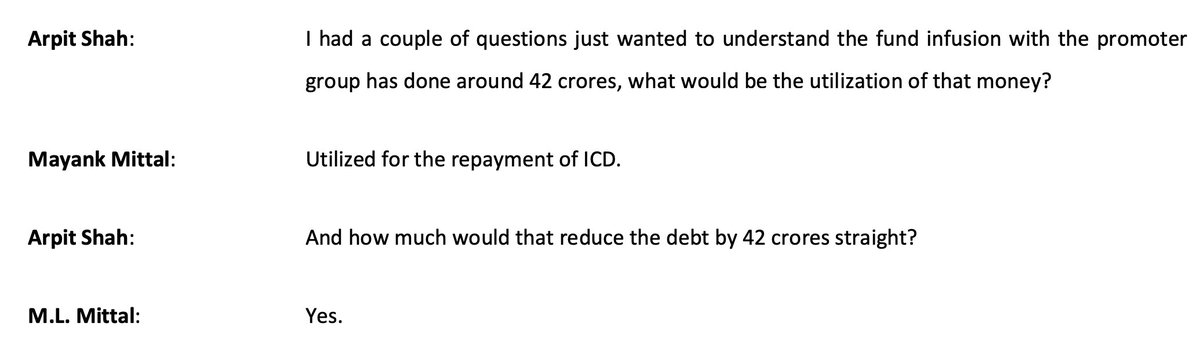

The promoter group has infused Rs 42 CR used to reduce debt on the balance sheet by the same amount.

WC cycle is around 3-4 months.

Receivables: 45 days

Inventory (WIP>Finished Goods): 2 months

Payables: 10 days

WC Days= 45+60-10

Receivables: 45 days

Inventory (WIP>Finished Goods): 2 months

Payables: 10 days

WC Days= 45+60-10

• • •

Missing some Tweet in this thread? You can try to

force a refresh