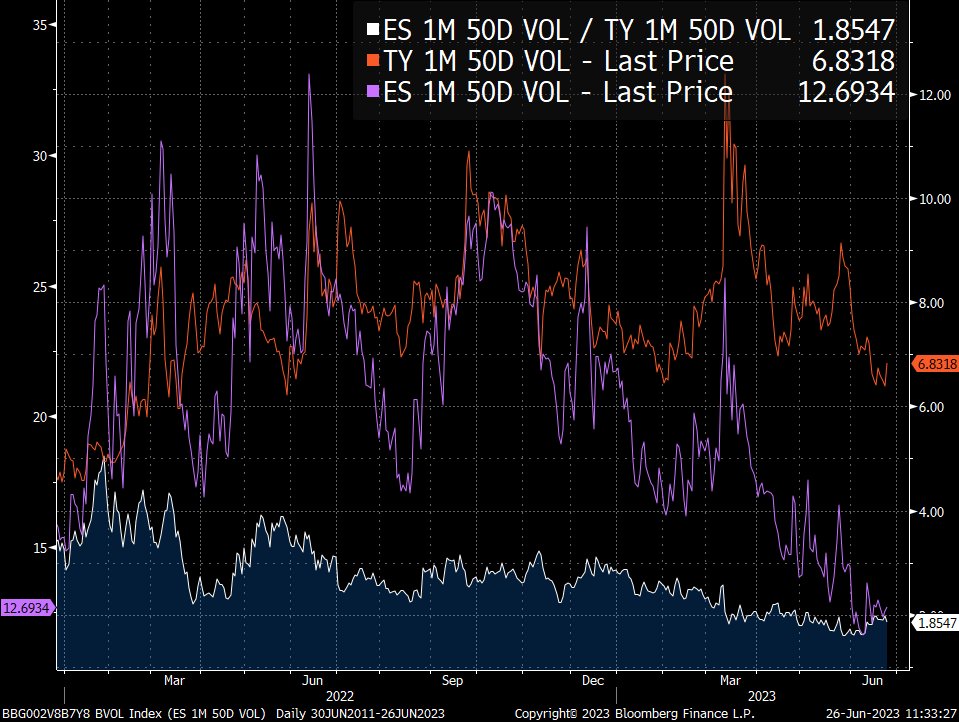

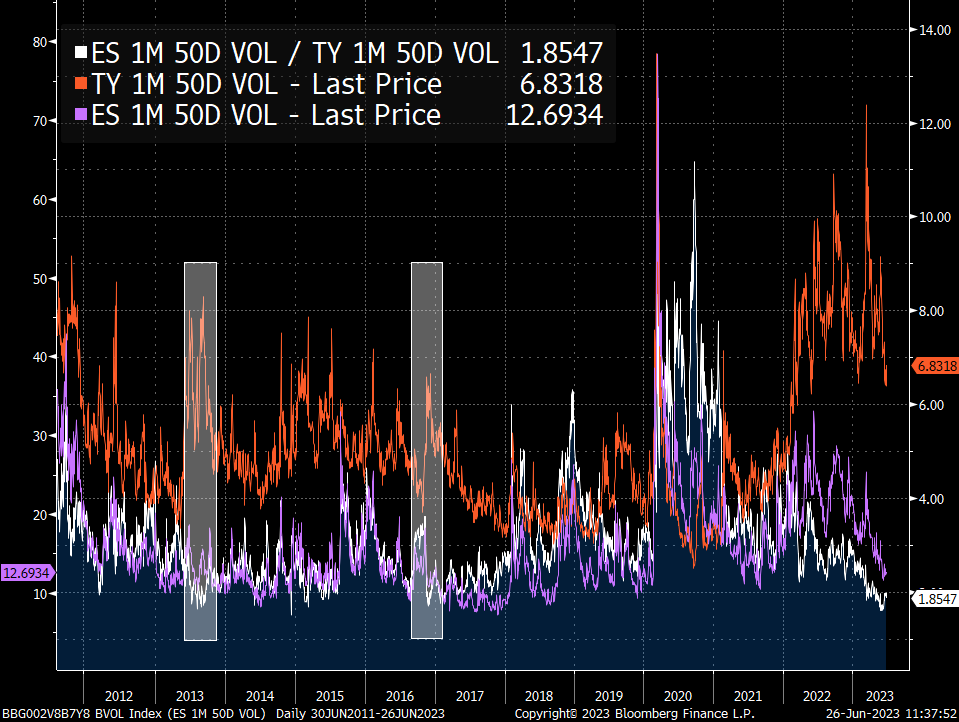

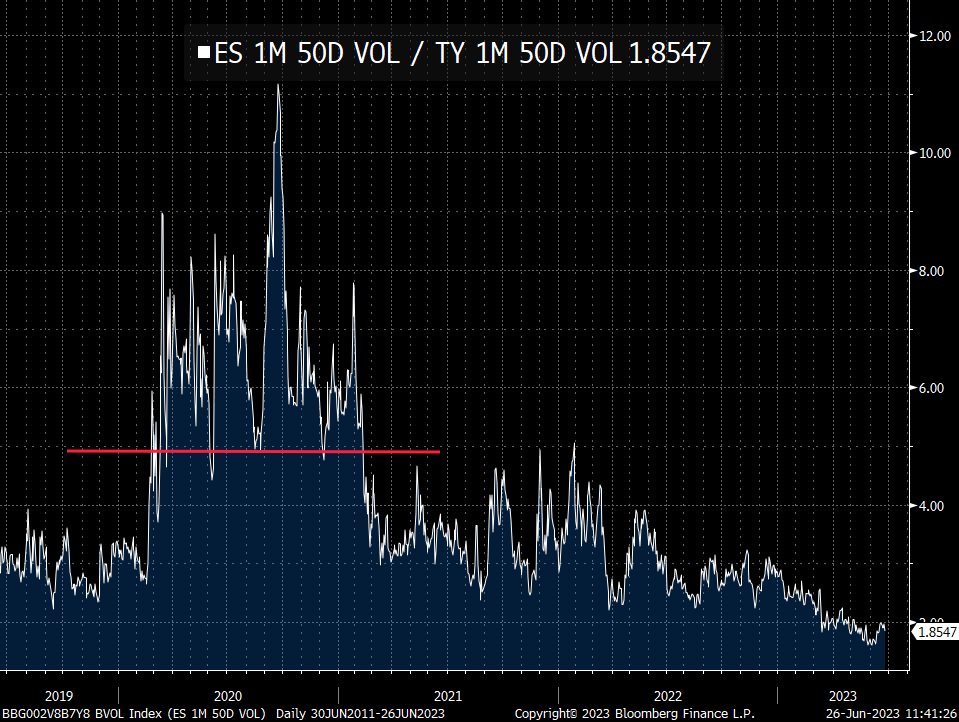

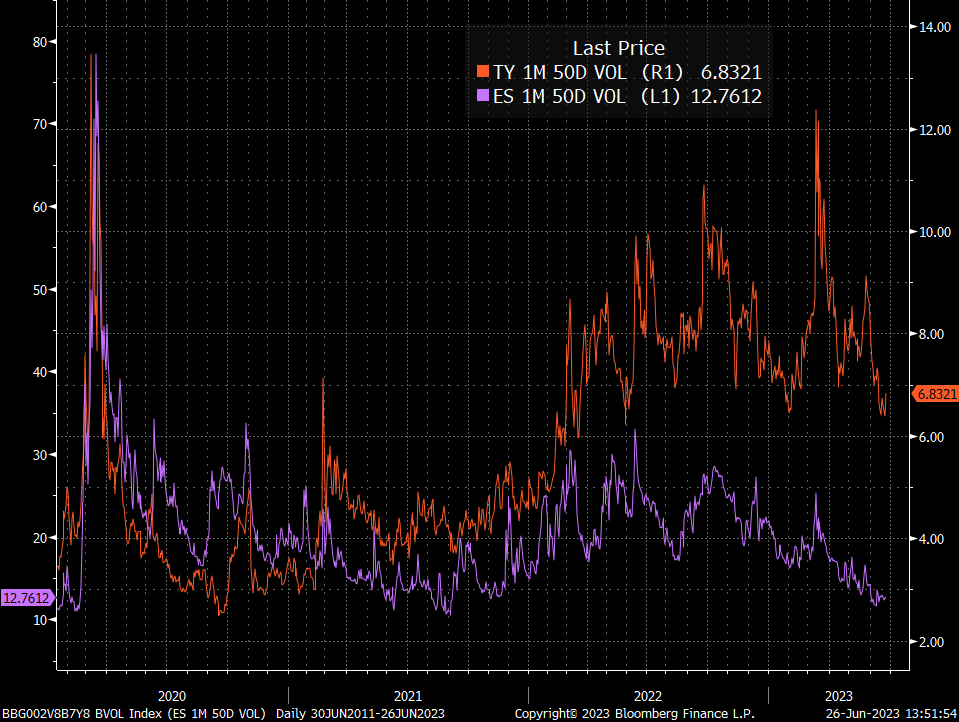

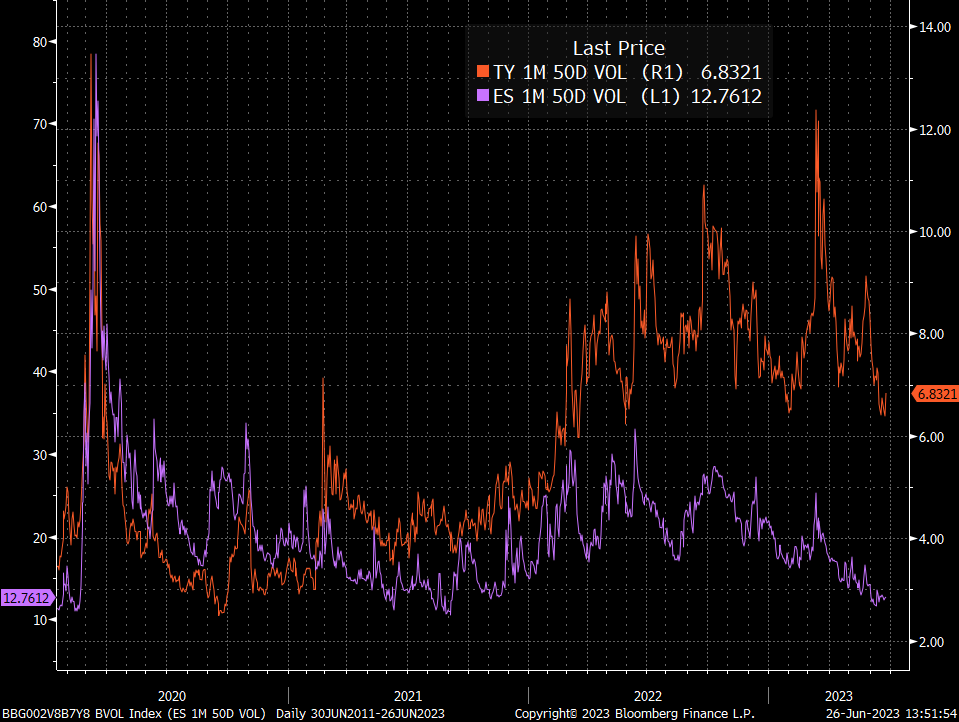

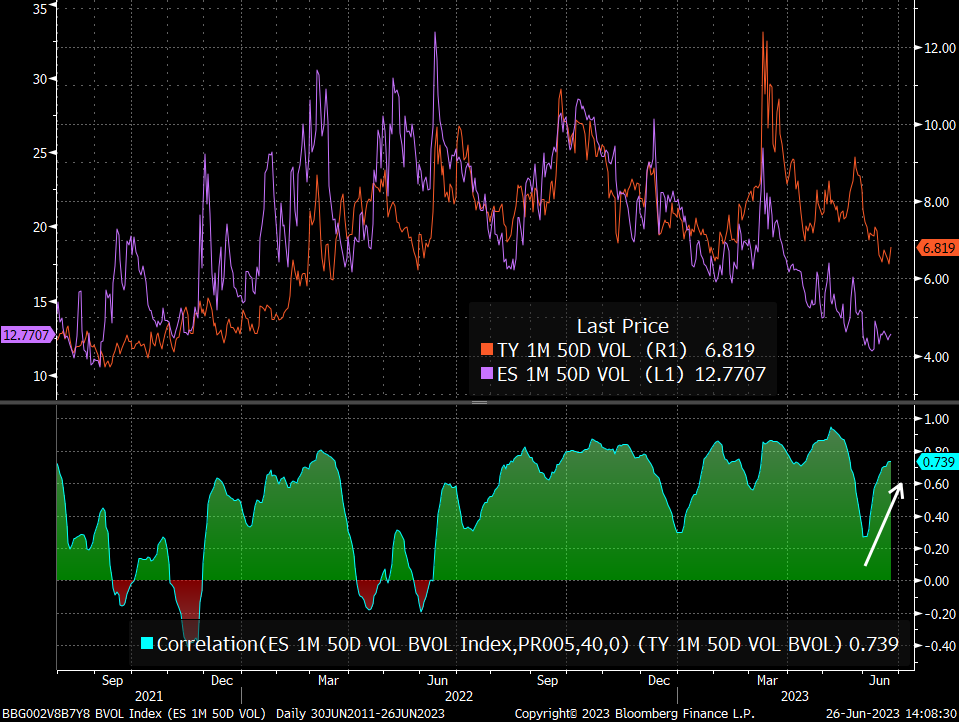

This is the ratio of 1 month ATM implied vol on ES vs TY. It recently went as low as 1.61, only seen for a blip in 2014. Other notable observed lows close to this level was 2013 and 2016 (the first clue).

Now if you're expecting bearporn - let me finish first before you do

/

Now if you're expecting bearporn - let me finish first before you do

/

The point of a ratio is that is involves TWO moving parts. Now with that in mind, let's try to deconstruct this ratio and find some sense in it. The obvious questions are

"why is it so low, what does it mean and what does it imply?"

So let's start with the first qn.

"why is it so low, what does it mean and what does it imply?"

So let's start with the first qn.

The ratio is low because equity IV has continued to decline while rate vol has not. Simple answer. Nothing more complicated needed.

What does it mean? Phrased another way, "WHY is it so low and WHY has equity IV declined while rate vol hasn't?"

Now this isn't quite as simple but we can draw some conclusions by just looking at a bit more of the chart. As mentioned, 2013 and 2016 both saw similar lows and...

Now this isn't quite as simple but we can draw some conclusions by just looking at a bit more of the chart. As mentioned, 2013 and 2016 both saw similar lows and...

...well the decline in the ratio was driven primarily by rate vol increasing significantly. in 2013 it was the taper tantrum and in 2016 it was fiscal impulse implied from Trump winning the presidential election that drove yields higher and as a result, rate vol.

So, what has driven the ratio to its current low? First let's look at the ratio again. We can understand that it shot up during the pandemic because of the global shutdown that rocked markets. Through 2020 the ratio implied a hefty vol premium in stocks over bonds until Feb 2021.

So what I'm concerned about is "what happened in Feb 2021 that caused the ratio to drop? Is this WHY the ratio embarked on a trip to current lows?

After all, that is the point at which the prior regime (the pandemic premium) ended.

After all, that is the point at which the prior regime (the pandemic premium) ended.

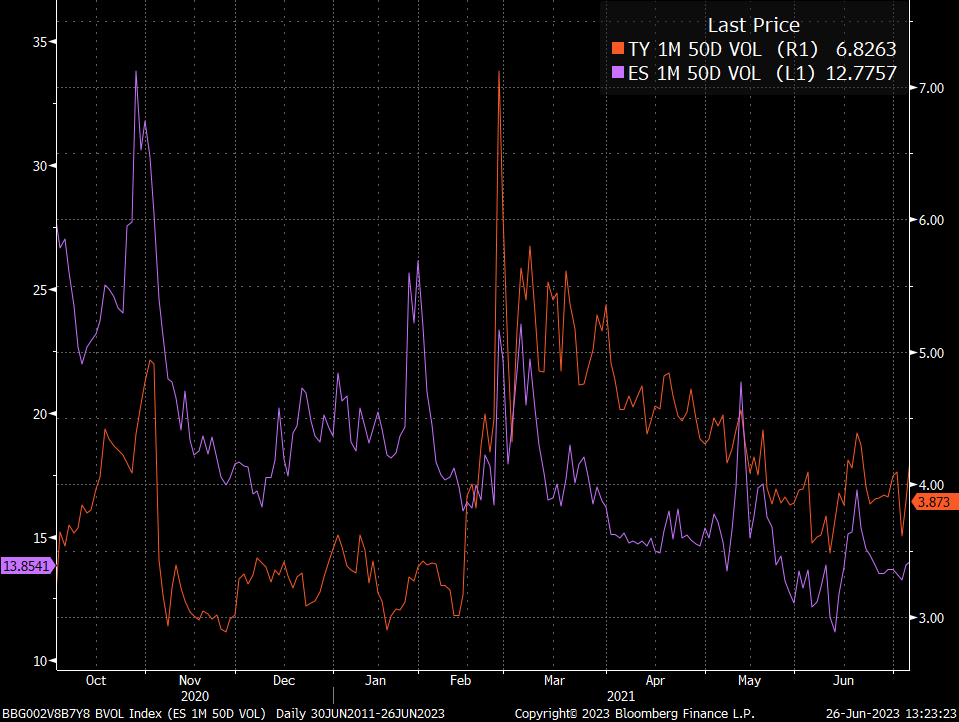

Amid the stupidity of meme-stock mania in Jan/Feb 2021 (p.s. the new trailer for Dumb Money with Seth Rogen as Gabe Plotkin just dropped), a shot across the bow of the rates market flew loudly but just not as loud as gamma-induced shitcos ripping to the moon:

Rates became unloved

Rates became unloved

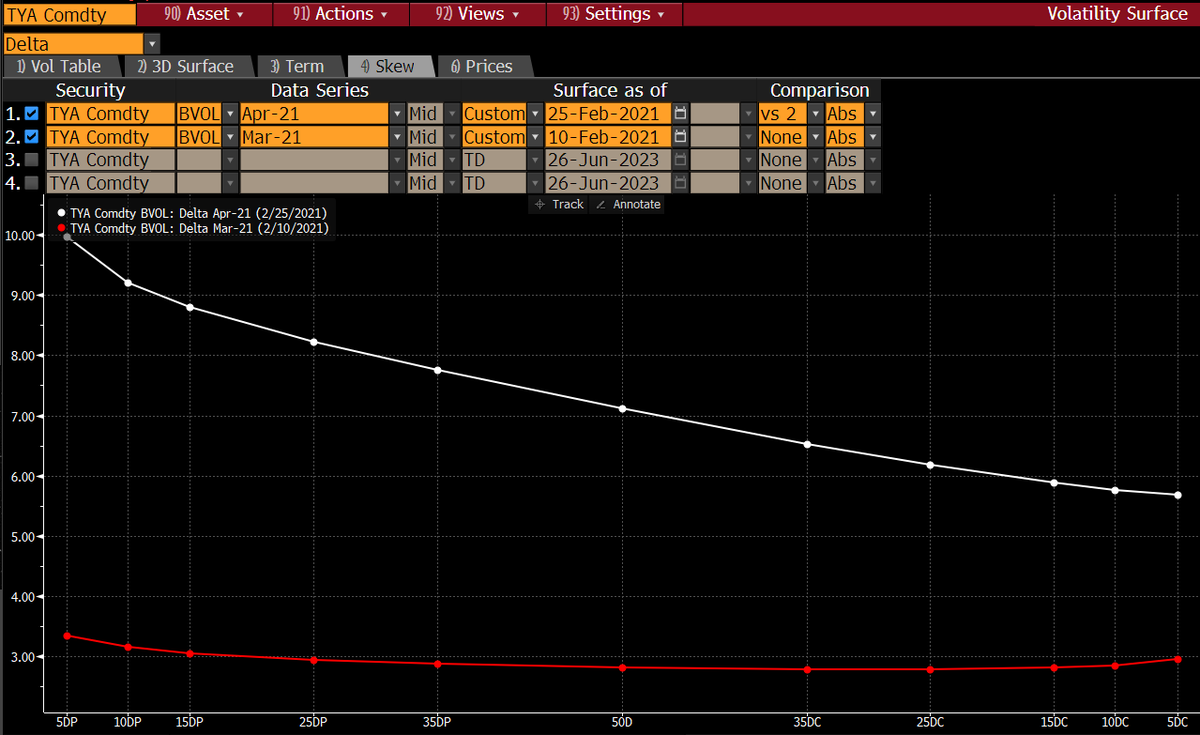

The put wing on TY (ZN) went from a 3vol handle on the 5 delta to 10% in 2 weeks. Inflation was becoming a concern and the market had *gasp* priced in as much as 1 rate hike by end 2022.

Funny how the clarity of the present elucidates the stupidity of the past.

Funny how the clarity of the present elucidates the stupidity of the past.

On the 25th of February, 2021 an otherwise normal Thursday the 10y Treasury lurched 14bps higher (23bps wider at one point); the highest single day amount since 2016's presidential election, outside of 3 days during the height of the pandemic.

That day they auctioned 7y as well.

That day they auctioned 7y as well.

It was a fucking disaster. The bid-to-cover (BC) fell to 2.04, the lowest in the 7-year's auction history. It was, essentially the harbinger of things to come.

I myself, up to that point had generally thought that pandemic recoveries ensured a long long runway of low rates. Yikes

I myself, up to that point had generally thought that pandemic recoveries ensured a long long runway of low rates. Yikes

It was so bad, one of the best rates traders around, @joegilster wasn't spared any peace of mind to care for his wife and expectant child. Here, he's chronicled in one of my favourite articles to date titled "'Dude, Get Back to Your Desk': The Week That Roiled Bond Markets"

While rate vol eventually calmed, the seed was planted in the market's mind - we could go higher and we will. It was just undetermined and underappreciated how much.

Narrator: it was a lot.

So the why of the ratio being so low currently is explained by rate volatility being very elevated due to a bearish paradigm that began in Feb 2021 juxtaposed with an equity market that was playing the SAME recovery outlook mind you.

To bring you back to this chart - look and appreciate that equity vol was HIGH in 2022 relative to the last decade and even while it is low, it is not abnormally so. It is rate vol that is the "anomaly" here.

Equity vol's anomaly is its reticence to follow rate vol, not its level

Equity vol's anomaly is its reticence to follow rate vol, not its level

The last qn of 'what does it imply?' is as usual, the hardest one to answer. But if we know 1) the ratio is at lows and 2) 'cos rate vol is abnormally high, and 3) it's driven by a bearish regime then the "mean reversion" bias leans more to bearish rate vol than bullish eq vol

this seems congruent with either of 2 scenarios:

1) normalisation of inflation sees pressure across the curve subside (vol lowers as Fed bets pared back, etc) while eq remains stable

2) a significant growth decline sees bonds get bid, lowering bearish skewed vol and eq vol rises

1) normalisation of inflation sees pressure across the curve subside (vol lowers as Fed bets pared back, etc) while eq remains stable

2) a significant growth decline sees bonds get bid, lowering bearish skewed vol and eq vol rises

the bearporn scenario is an extreme version of no.2 or a reflation scare that sends yields higher, rate vol higher and breaks the resolve of equity bulls now that PoV gains have been priced in and an en masse rush to dump stocks. Plausible but you need to see rate vol rip first.

Some risks I see are that we do see some signs of inflation coming back. I do not like that consumption remains robust while producer sentiment remains low and its implications on cost-push inflation from a supply constraint. Some central banks are still hawkish.

The onus is on data to confirm that rate vol should lower because enough has been done. Hard data is certainty. Vol is simply uncertainty.

That is why cross asset vol can come down with very little change in underlying levels - THAT'S HALF THE POINT!!!

That is why cross asset vol can come down with very little change in underlying levels - THAT'S HALF THE POINT!!!

So when looking at ratios such as these, yes they are very low. Yes it looks like equity vol is relatively cheap. But I believe the base case for normalisation happens under very economically constructive conditions rather than calamitous ones.

Unless....

Unless....

• • •

Missing some Tweet in this thread? You can try to

force a refresh