Srivari Spices and Foods #IPO. Engaged in the business of manufacturing spices and flour (chakki atta). #SrivariIPO #IpoAlert

.

RHP: https://t.co/ioAwKvWDl0archives.nseindia.com/emerge/corpora…

.

RHP: https://t.co/ioAwKvWDl0archives.nseindia.com/emerge/corpora…

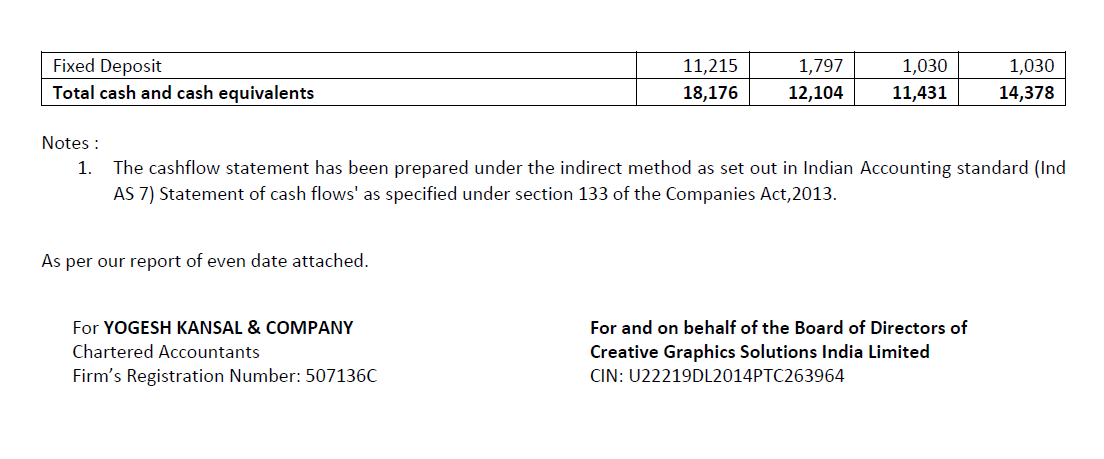

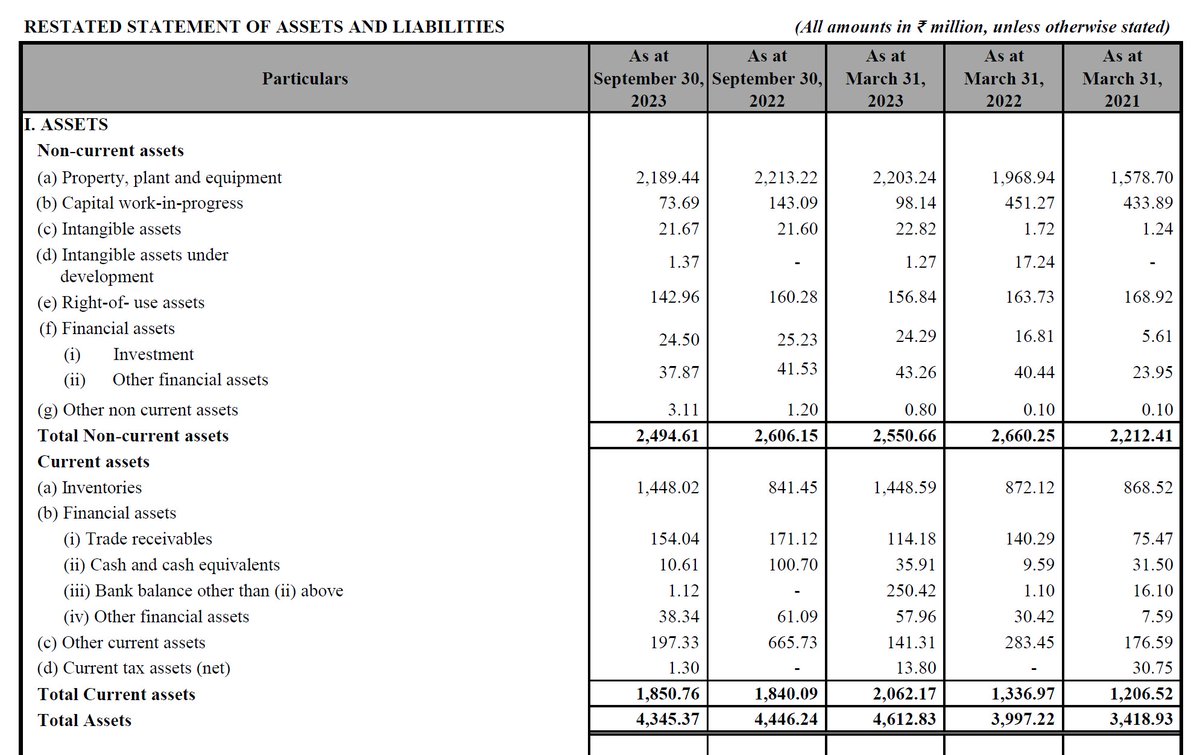

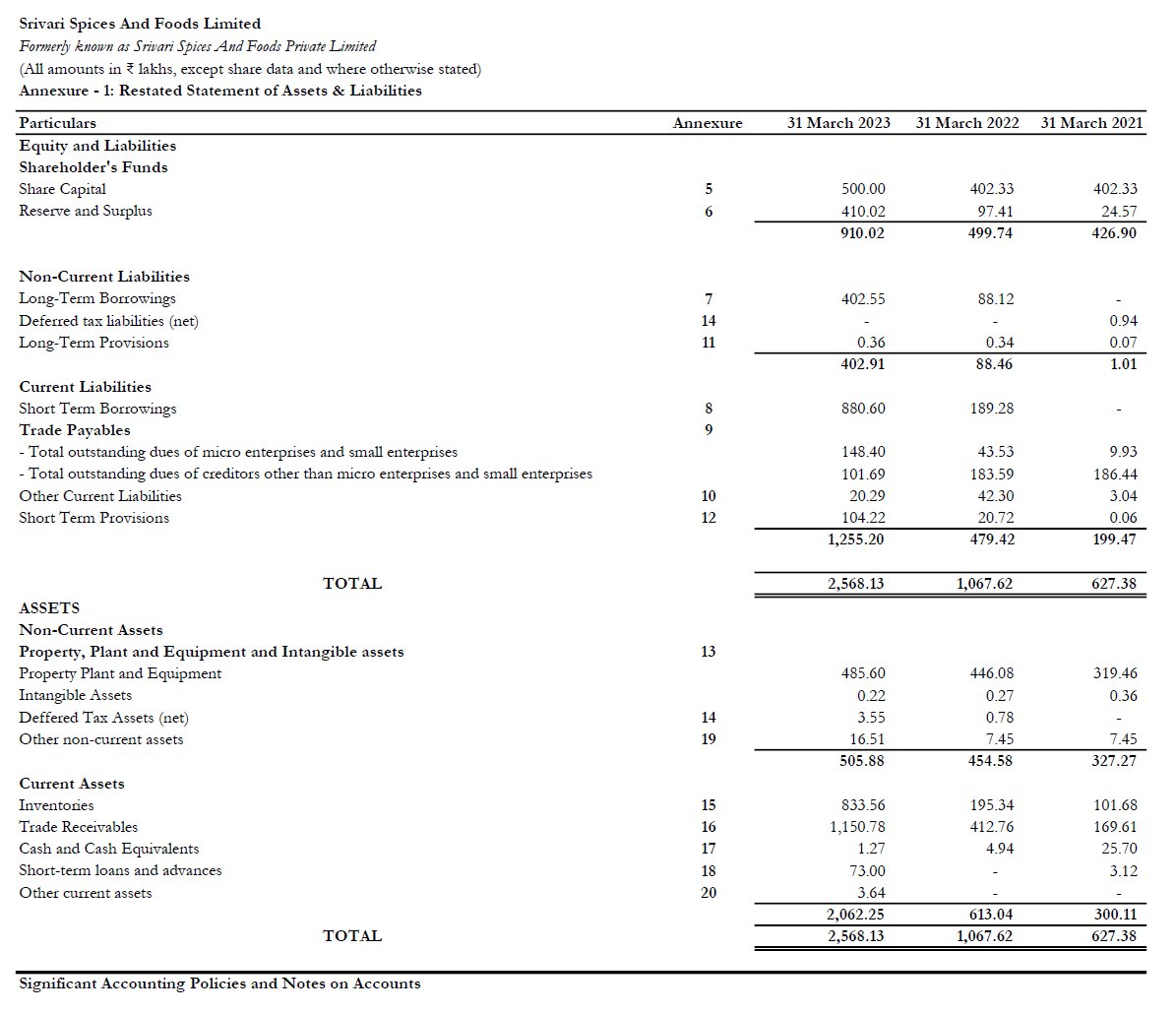

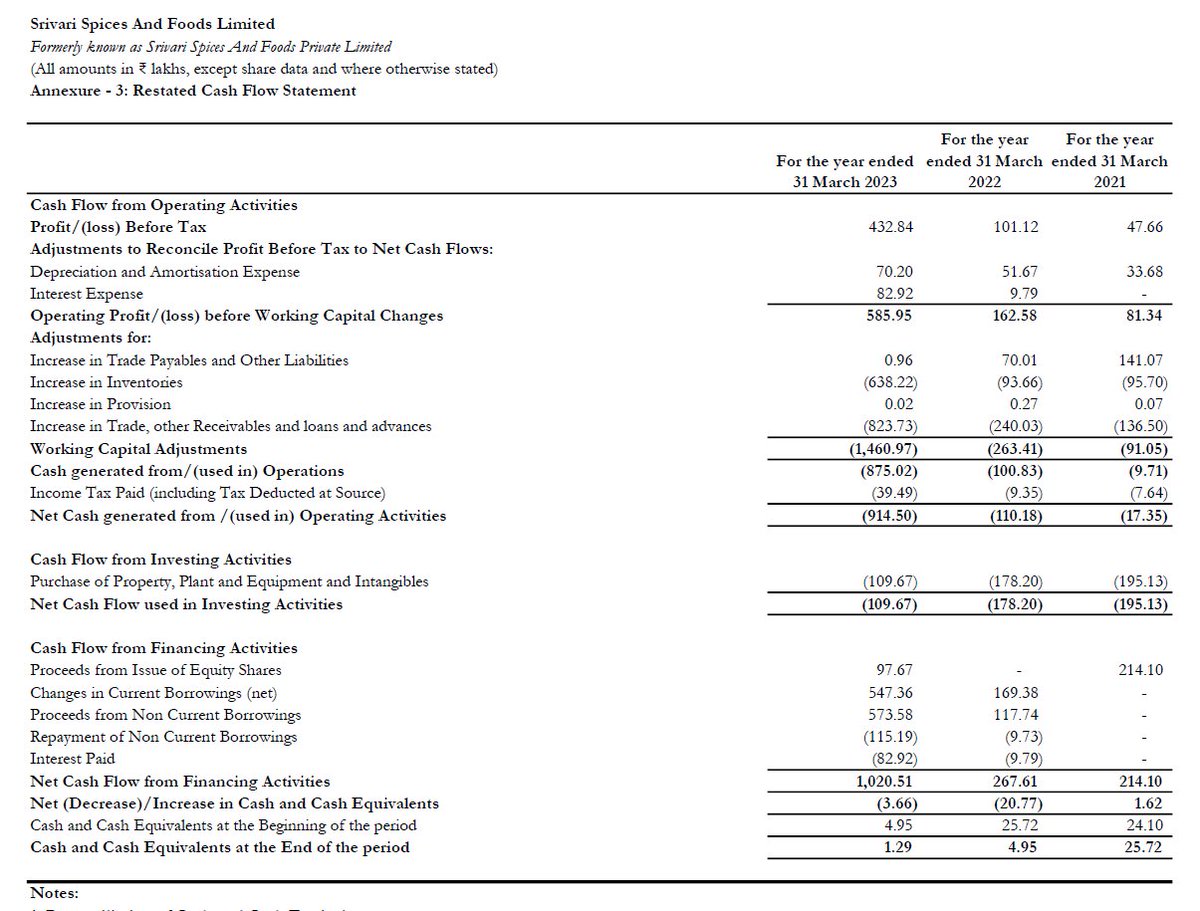

Balance Sheet and Cash Flow Statement:

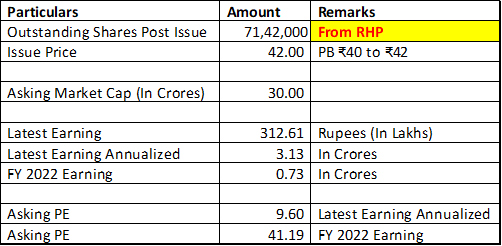

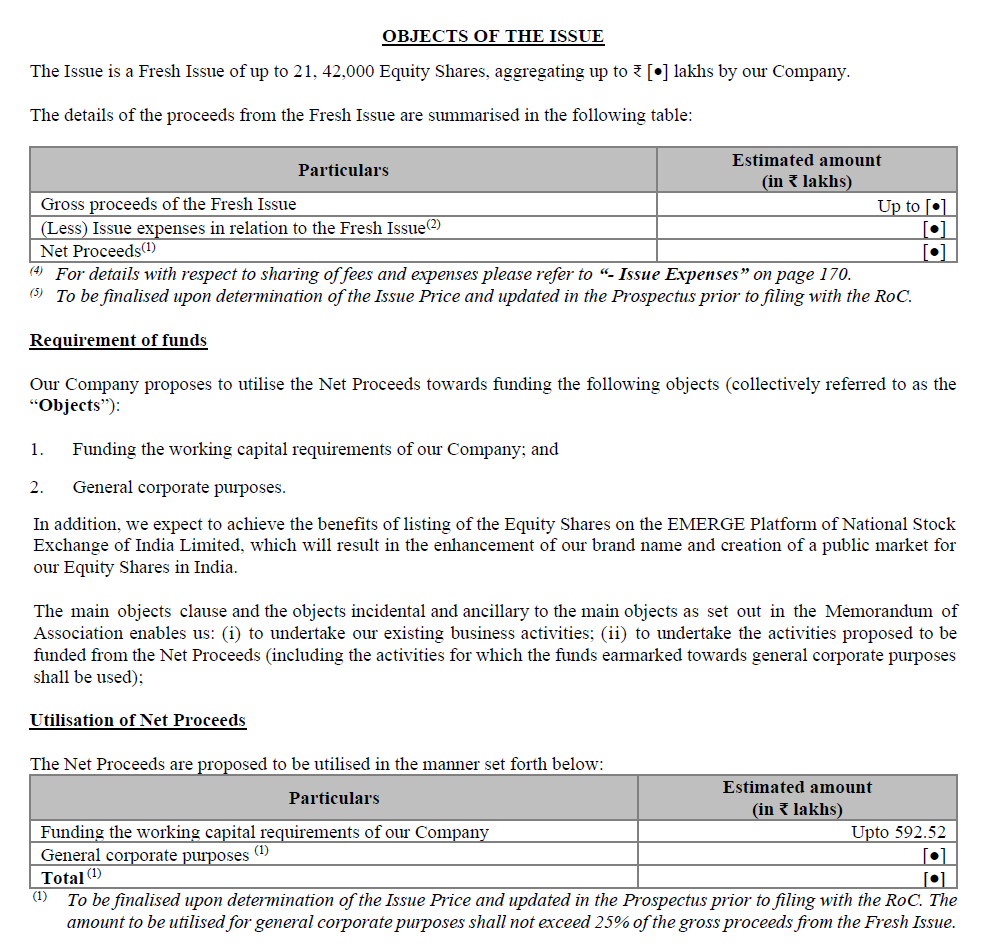

Objects of the Issue:

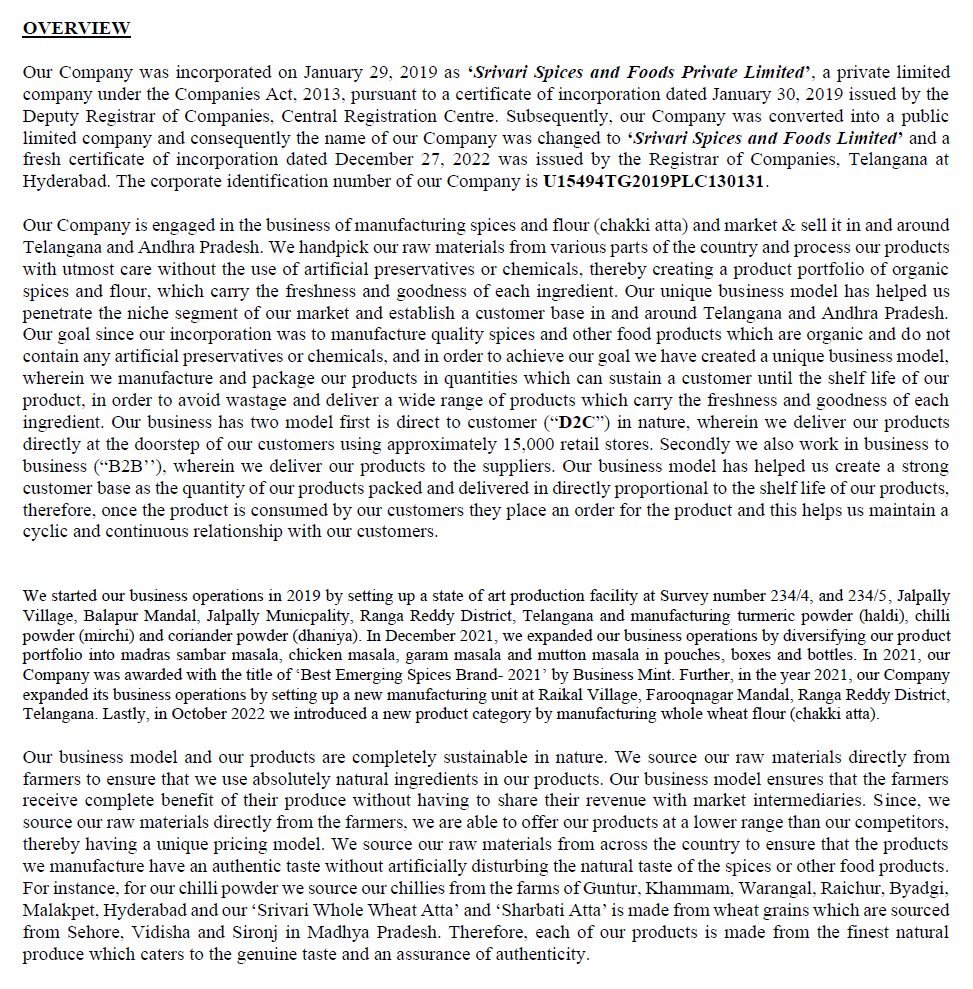

Business Overview:

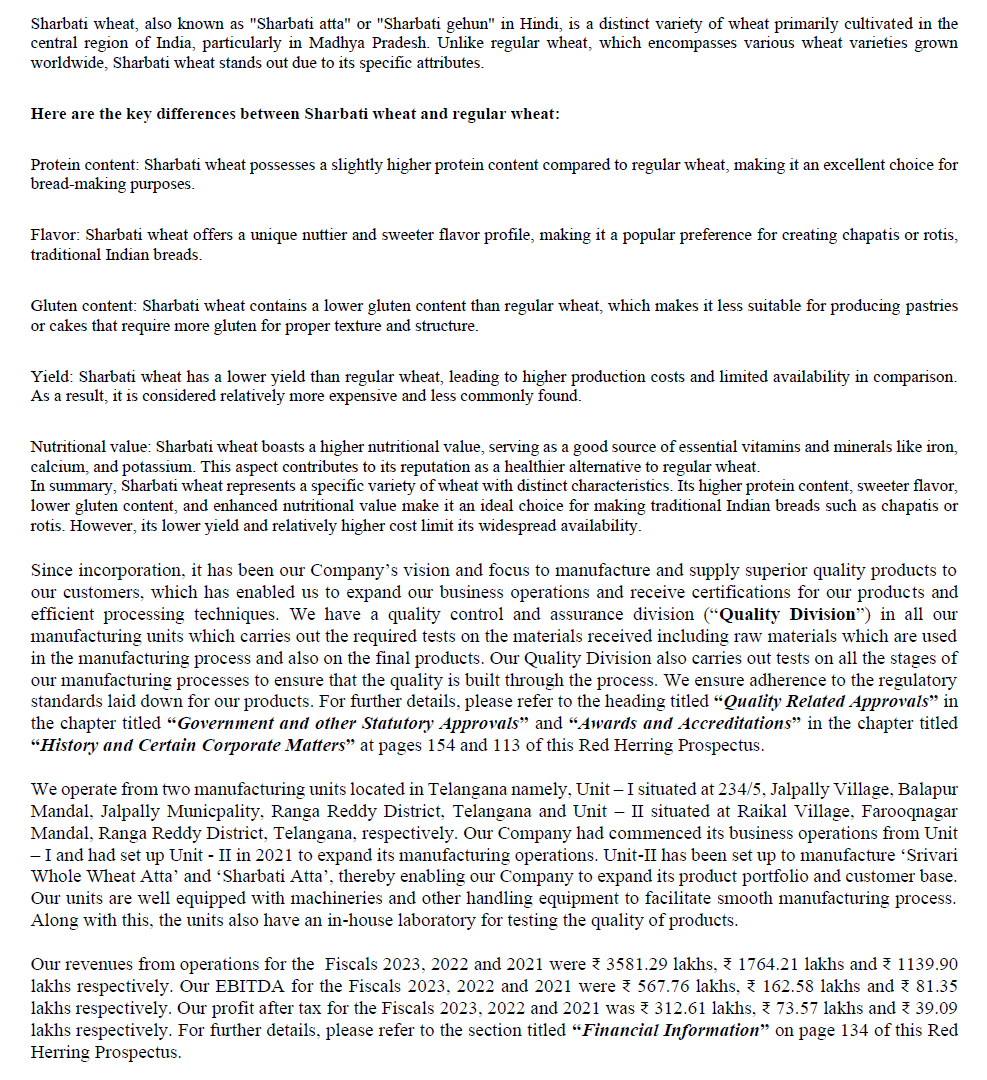

Business Overview (Continued):

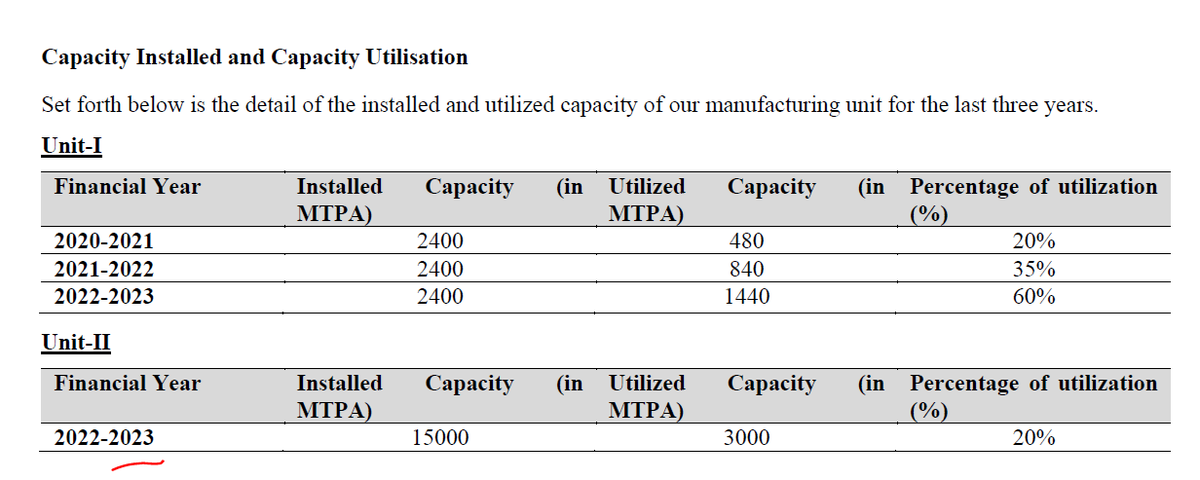

Capacity Utilization:

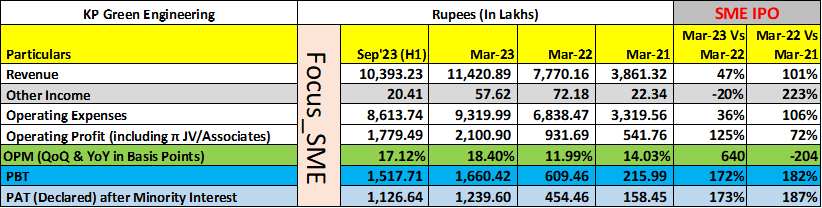

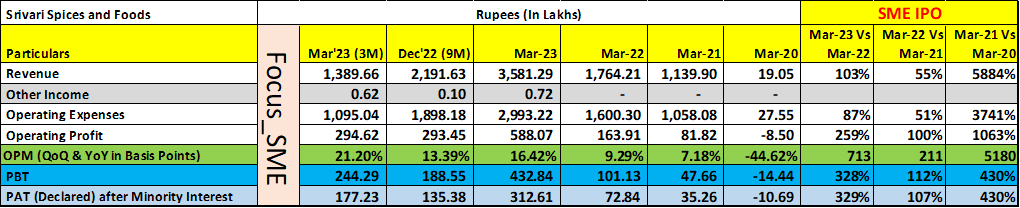

The asking valuation looks reasonable even though comes on the back of superb performance, which is aided by Unit-II that started recently. There's ample capacity available in both Unit-I & Unit-II. The cash flow though isn't good but not an issue right now IMO.

Company has added a lot of debts in FY23, which is OK given new unit but it's the interest rates that looks scary to me. Please do the math, how much would be FY24 interest in total? And if the company goes to have issues with Working Capital, then it can spell trouble.

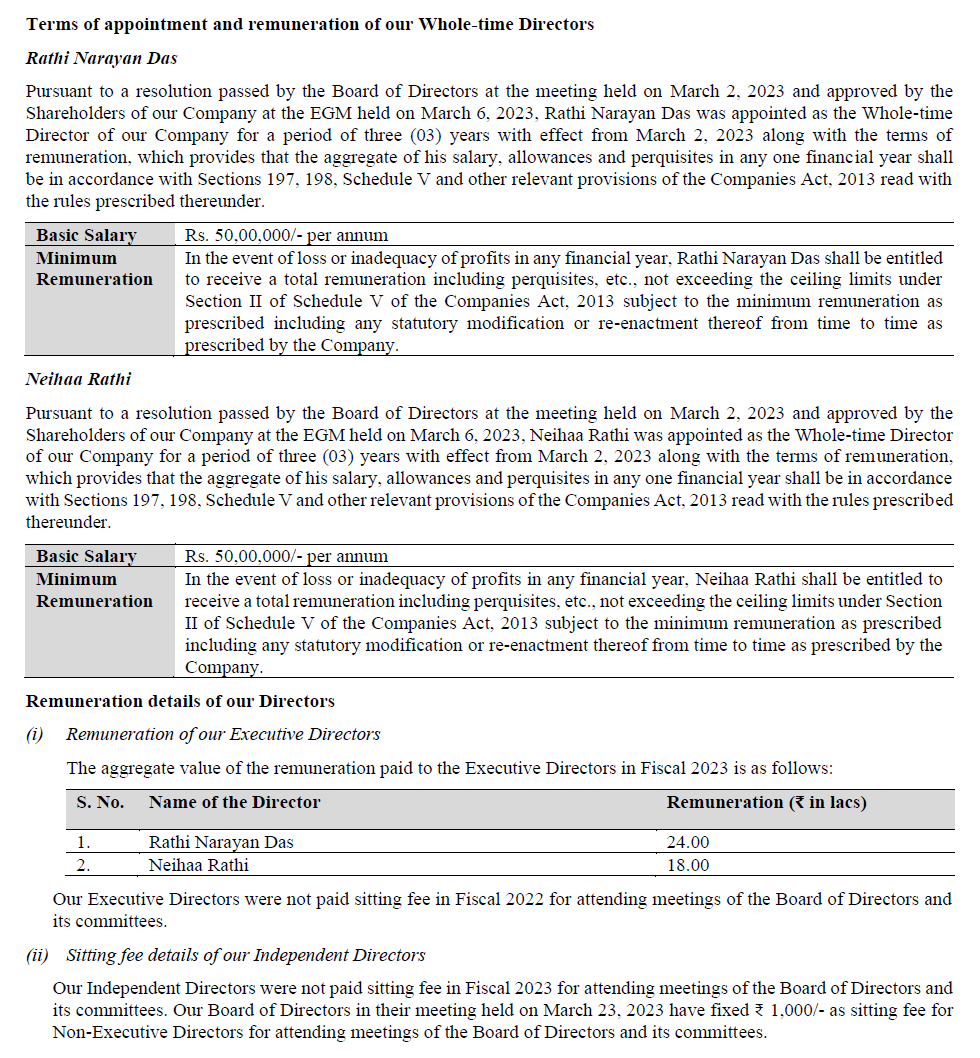

Management compensation looks ok now but might be on the higher side later. The related party transactions as of now look pretty good. Monitor debt &working capital movement as well as related party transactions & management compensation post listing.

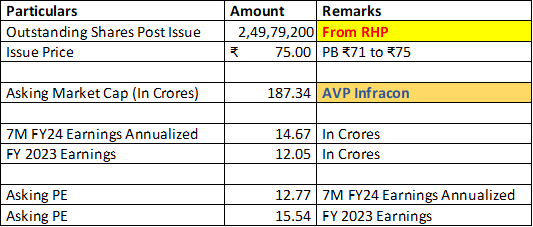

Overall, I am not comfortable with interest rates on debts but capacity leaves a lot on the table & valuation isn't sky high either. I MAY APPLY.

.

PLEASE DO YOUR OWN DUE DILIGENCE, REVIEW ACCORDING TO YOUR INVESTMENT STYLE AND THEN TAKE A DECISION.

.

PLEASE DO YOUR OWN DUE DILIGENCE, REVIEW ACCORDING TO YOUR INVESTMENT STYLE AND THEN TAKE A DECISION.

• • •

Missing some Tweet in this thread? You can try to

force a refresh