1/x

$ES_F $NQ_F $SPY $QQQ $IWM $TNX $TLT $GLD #BTC #Bitcoin

Predictive Analytic Models (PAM)

Robert P. Balan

Aug 23, 2023 10:17 AM

EUROPE SESSION BRIEF:

OUR EVALUATION OF THE US LABOR AND EMPLOYMENT SITUATION SHOWS DATA HAS STARTED BECOMING LESS BENIGN, AND MEDIA REPORTS LIKELY TO TRIGGER MORE BOND AND EQUITY PROFIT-TAKING AHEAD OF THURSDAY INITIAL JOBS CLAIMS, AND FRIDAY'S JACKSON HOLE EVENT

Our high-frequency evaluation of the US labor and employment situation suggests that the still benign labor and employment data will start becoming less favorable.

And if media stories today showcasing the possible degradation of recent benign jobs report are correct, then Mr. Jay Powell will have less favorable employment situation to validate a higher-for-longer rate policy during the JHole event.

$ES_F $NQ_F $SPY $QQQ $IWM $TNX $TLT $GLD #BTC #Bitcoin

Predictive Analytic Models (PAM)

Robert P. Balan

Aug 23, 2023 10:17 AM

EUROPE SESSION BRIEF:

OUR EVALUATION OF THE US LABOR AND EMPLOYMENT SITUATION SHOWS DATA HAS STARTED BECOMING LESS BENIGN, AND MEDIA REPORTS LIKELY TO TRIGGER MORE BOND AND EQUITY PROFIT-TAKING AHEAD OF THURSDAY INITIAL JOBS CLAIMS, AND FRIDAY'S JACKSON HOLE EVENT

Our high-frequency evaluation of the US labor and employment situation suggests that the still benign labor and employment data will start becoming less favorable.

And if media stories today showcasing the possible degradation of recent benign jobs report are correct, then Mr. Jay Powell will have less favorable employment situation to validate a higher-for-longer rate policy during the JHole event.

2/X

Robert P. BalanOwnerModeratorLeaderAug 23, 2023 10:18 AM

-- 500,000 jobs could disappear in dramatic revision of US government data: JPMorgan economist Daniel Silver predicts that the job market is 500,000 positions weaker than what the Bureau of Labor Statistics’ originally reported, meaning there are 40,000 fewer jobs pe…nypost.com/2023/08/22/us-…

NYpost.com

Robert P. BalanOwnerModeratorLeaderAug 23, 2023 10:18 AM

-- 500,000 jobs could disappear in dramatic revision of US government data: JPMorgan economist Daniel Silver predicts that the job market is 500,000 positions weaker than what the Bureau of Labor Statistics’ originally reported, meaning there are 40,000 fewer jobs pe…nypost.com/2023/08/22/us-…

NYpost.com

3/X

Robert P. Balan

Aug 23, 2023 4:56 PM

Here we are getting some supporting data for our thesis that the cracks in the employment and labor siotuation, will likely grow progressively wider. Recent hints of softness in the jobs data should progressively grow softer.

Nick Timiraos

The US economy added 306,000 fewer jobs than previously estimated during the March 2022-23 period, according to the preliminary estimate of annual benchmark revisions to the establishment survey . . .

Robert P. Balan

Aug 23, 2023 4:56 PM

Here we are getting some supporting data for our thesis that the cracks in the employment and labor siotuation, will likely grow progressively wider. Recent hints of softness in the jobs data should progressively grow softer.

Nick Timiraos

The US economy added 306,000 fewer jobs than previously estimated during the March 2022-23 period, according to the preliminary estimate of annual benchmark revisions to the establishment survey . . .

4/X

Robert P. Balan

Aug 23, 2023 2:20 PM

The initial claims data this week/tomorrow may make a difference with the Jackson Hole event Friday. It is only one data point, but if the insurance claims keep on rising, as has been the case for the past several weeks, then the NonFarm Payroll and Unemployment Rate data have to subsequently adjust lower, and higher, respectively.

Robert P. Balan

Aug 23, 2023 2:20 PM

The initial claims data this week/tomorrow may make a difference with the Jackson Hole event Friday. It is only one data point, but if the insurance claims keep on rising, as has been the case for the past several weeks, then the NonFarm Payroll and Unemployment Rate data have to subsequently adjust lower, and higher, respectively.

5/X

Robert P. BalanOwner

Aug 23, 2023 11:06 AM

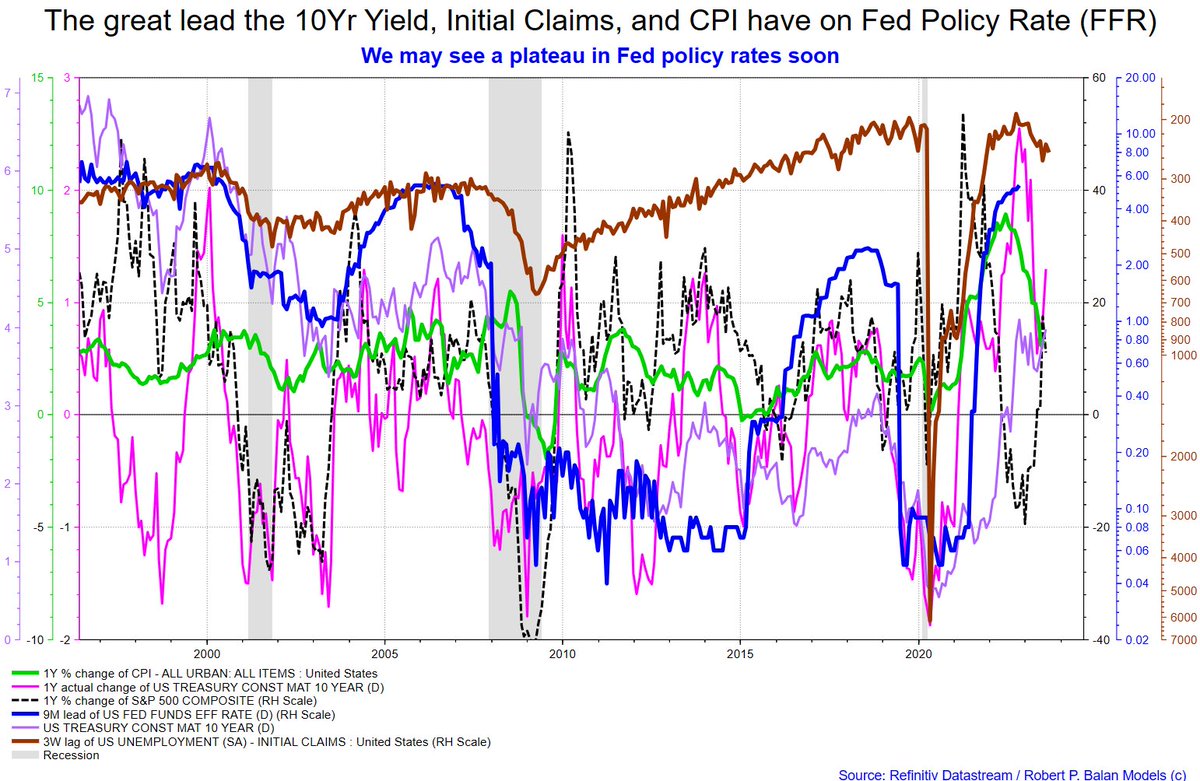

In fact, if the lead of changes on Initial Jobless Claims, 10Yr Yield and CPI over changes of the FFR is still extant, then we could see a plateau on FFR rates very soon.

In previous monetary policy cycles, the FFR plateau-ed well before the inflection point higher of the initial claims data, CPI and the 10Yr Yield.

Different circumstances this time around, its true; but the sequential logic remains the same.

Robert P. BalanOwner

Aug 23, 2023 11:06 AM

In fact, if the lead of changes on Initial Jobless Claims, 10Yr Yield and CPI over changes of the FFR is still extant, then we could see a plateau on FFR rates very soon.

In previous monetary policy cycles, the FFR plateau-ed well before the inflection point higher of the initial claims data, CPI and the 10Yr Yield.

Different circumstances this time around, its true; but the sequential logic remains the same.

6/X

User 58668107

Aug 22, 2023 11:28 PM

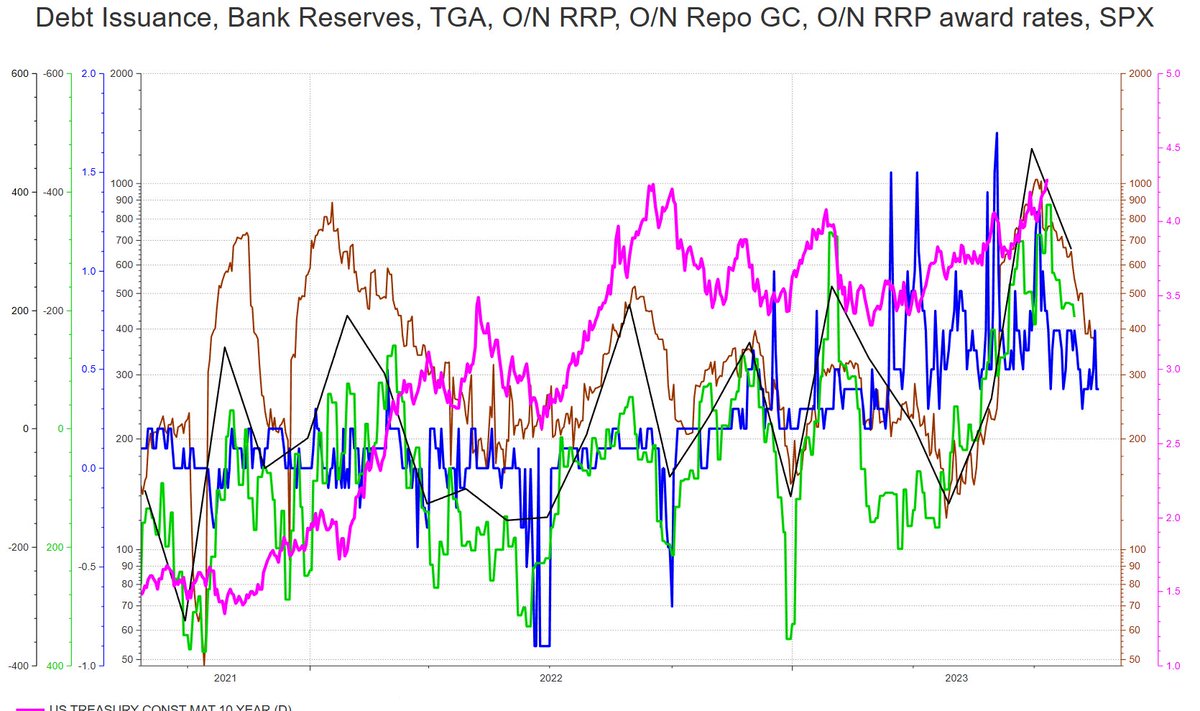

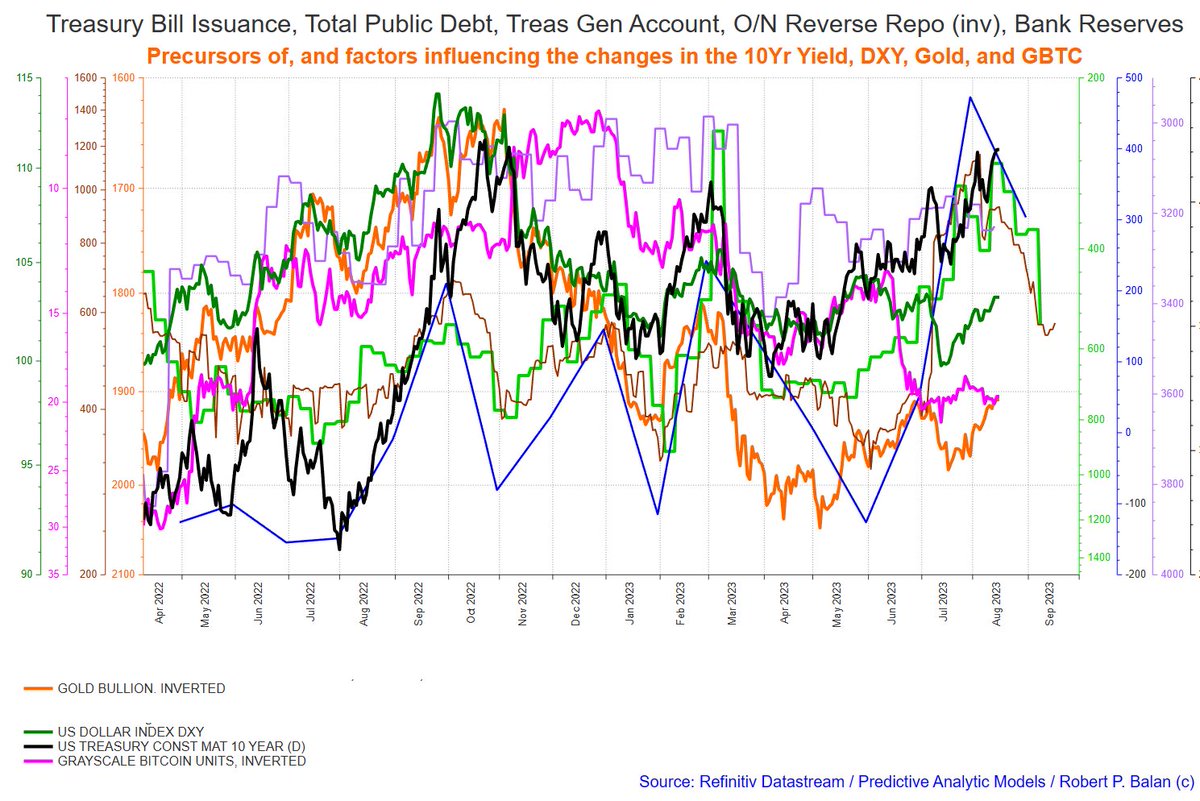

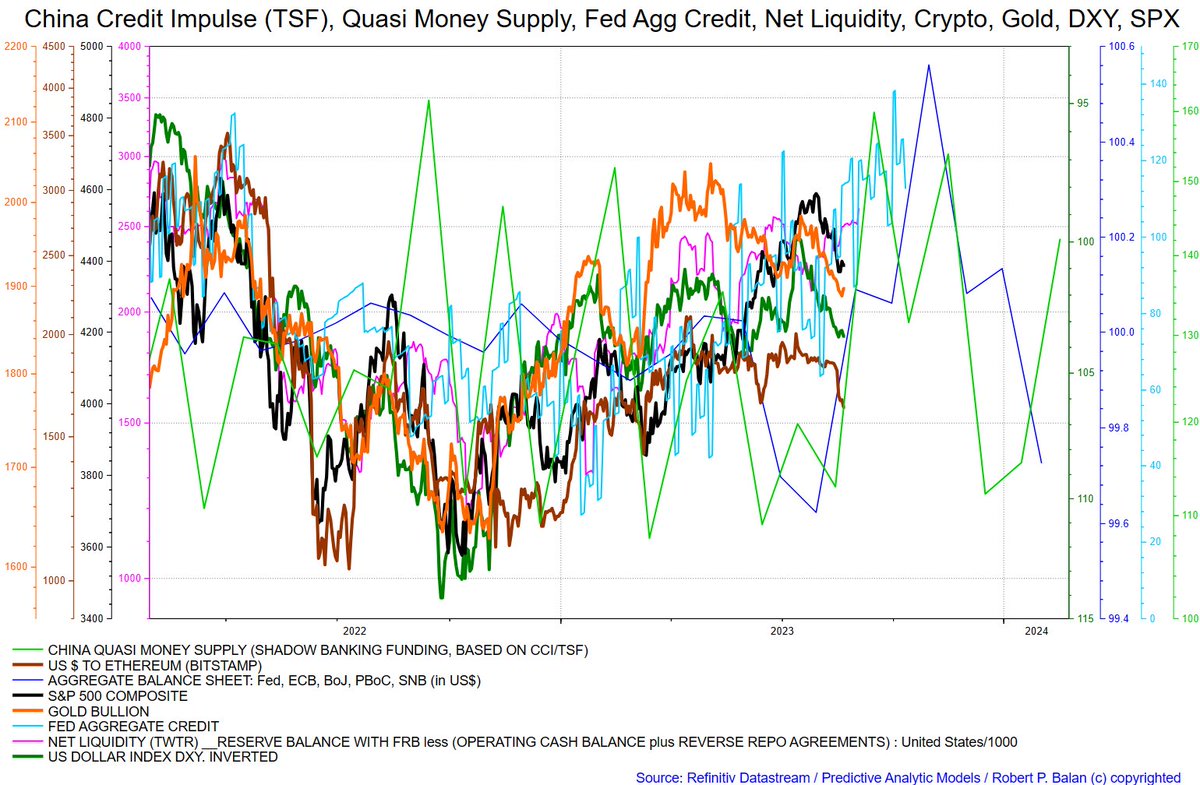

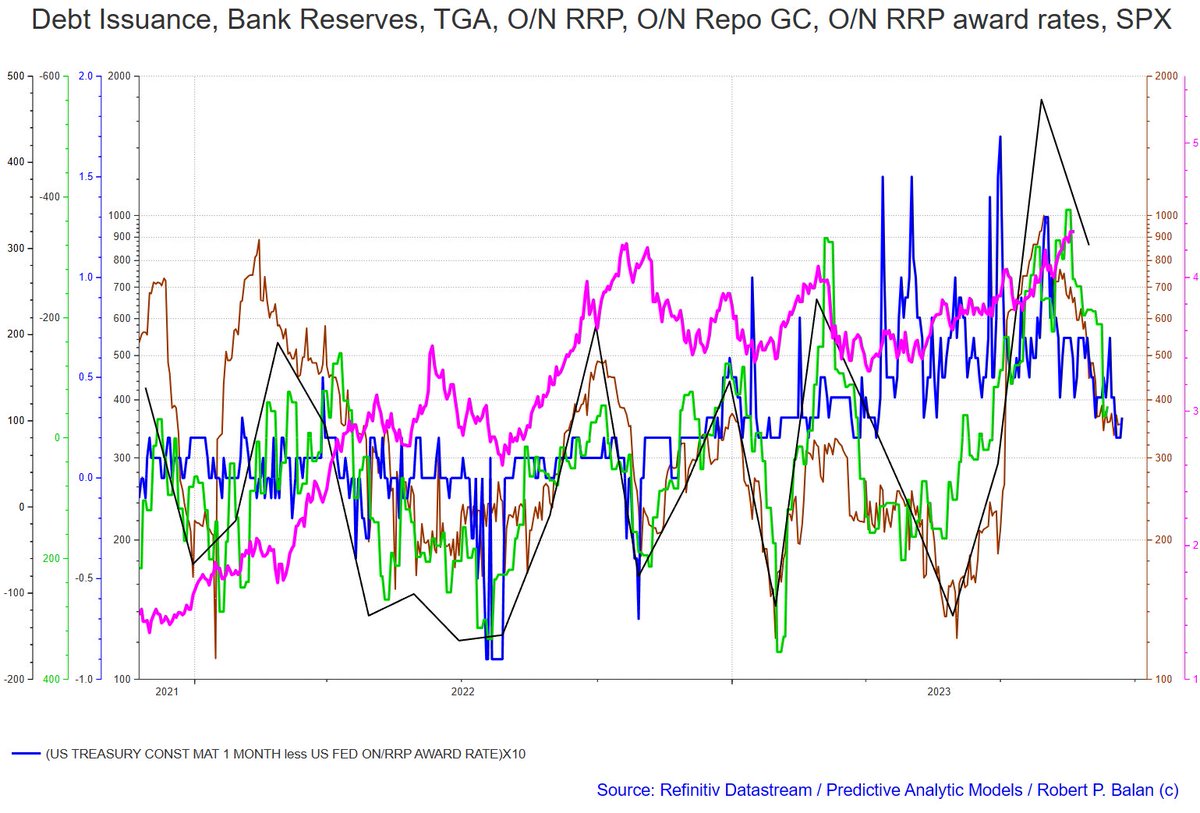

RB do u have the net liquidity chart which u used to show when there is a rise or fall over the next few weeks etc

Robert P. Balan

Aug 23, 2023 4:23 PM

User 58668107 -- This is a better reference -- it is in the PAM Analytics Channel, so it is available, 24 X 7.

User 58668107

Aug 22, 2023 11:28 PM

RB do u have the net liquidity chart which u used to show when there is a rise or fall over the next few weeks etc

Robert P. Balan

Aug 23, 2023 4:23 PM

User 58668107 -- This is a better reference -- it is in the PAM Analytics Channel, so it is available, 24 X 7.

7/X

gosume

Aug 23, 2023 5:09 PM

Robert P. Balan can we get an updated EWP chart for the 10Y? You think we fall to July lows into Mid Sep?

Robert P. Balan

Aug 23, 2023 5:38 PM

I have more confidence in this model than in my EWP schematics at this time.

First huge support Sept 11, and then after a small rebound, the Yield falls again until at least Sept 21.

gosume

Aug 23, 2023 5:09 PM

Robert P. Balan can we get an updated EWP chart for the 10Y? You think we fall to July lows into Mid Sep?

Robert P. Balan

Aug 23, 2023 5:38 PM

I have more confidence in this model than in my EWP schematics at this time.

First huge support Sept 11, and then after a small rebound, the Yield falls again until at least Sept 21.

8/X

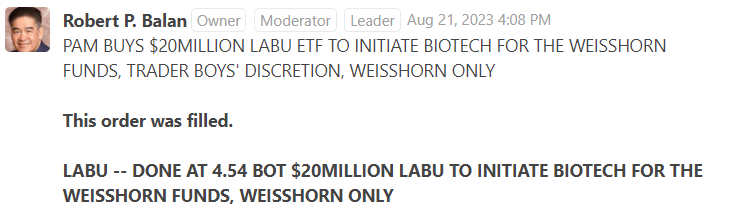

Robert P. Balan

Aug 23, 2023 5:08 PM

Mr. TK suggests that we should offload the first LABU trade if we get to see it above 5.10 -- just to make sure first trade does well. We will do that . . . this has been a phenom trade, and I am happy to oblige. 😃

Robert P. Balan

Aug 23, 2023 5:08 PM

Mr. TK suggests that we should offload the first LABU trade if we get to see it above 5.10 -- just to make sure first trade does well. We will do that . . . this has been a phenom trade, and I am happy to oblige. 😃

• • •

Missing some Tweet in this thread? You can try to

force a refresh