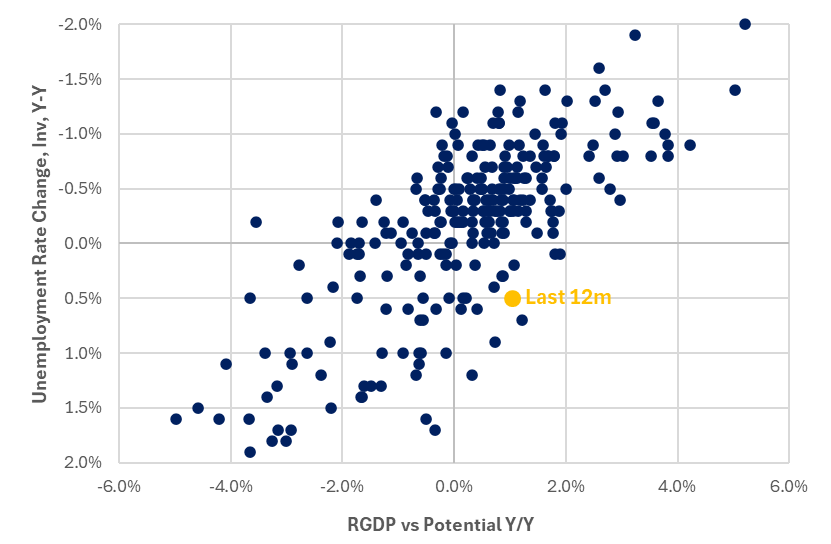

Broader employment data suggests the swift rise in the UE rate is an outlier and that the labor market remains pretty tight with only very gradually cooling.

If labor markets aren't weakening fast, the Fed has little urgency to deliver all those expected cuts.

Thread.

If labor markets aren't weakening fast, the Fed has little urgency to deliver all those expected cuts.

Thread.

While the UE rate gets a lot of attention, it by no means the only read on employment conditions. By this point, we have a pretty good set of data thru Jul.

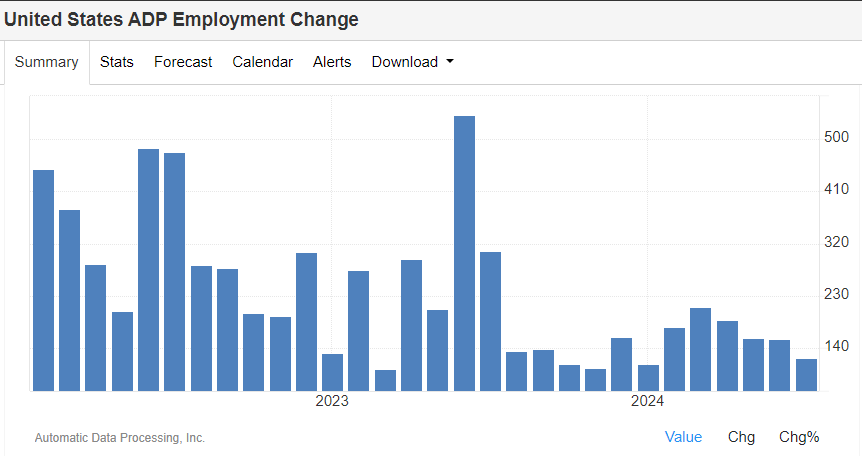

ADP private jobs data has been in roughly the same range for a year and recent data in line with last summer.

ADP private jobs data has been in roughly the same range for a year and recent data in line with last summer.

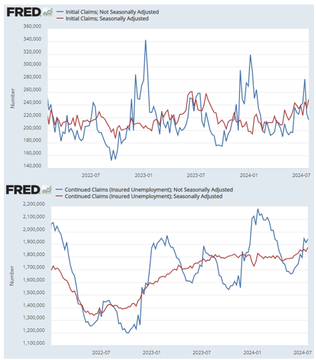

For all the noise about an uptick in claims measures, IC is basically at the same level as last summer and CC is 6bps of labor force higher. This may also be overstated by one-off issues not well captured by seasonal adj (TX hurricane, late MI retooling, MN ed).

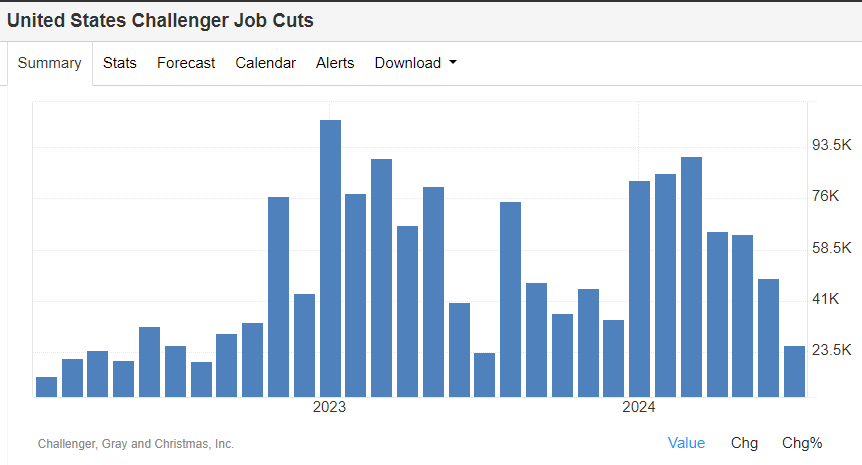

Challenger job layoff announcements posted their lowest numbers in a while (and very low on an outright basis).

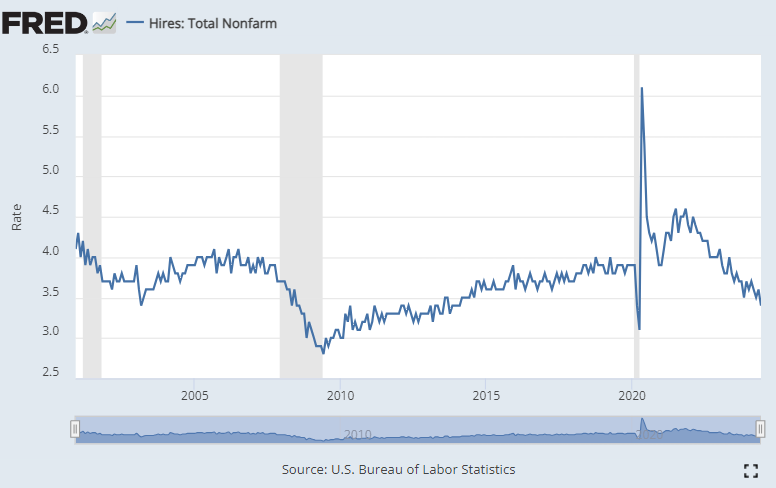

That's consistent with the layoffs figures that we've seen from JOLTS (a month lagged thru Jun) which moved down to multi-year lows.

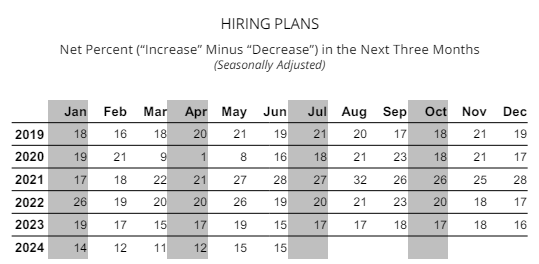

And in line with hiring plans from NFIB (thru June) are pretty stable over the last year and ticked up a tad in recent months.

This stability contrasts with other measures of hiring which suggests a bit more weakness. Though if the hiring rate was really this poor, we'd expect to see a much greater rise in continuing claims than we have so far.

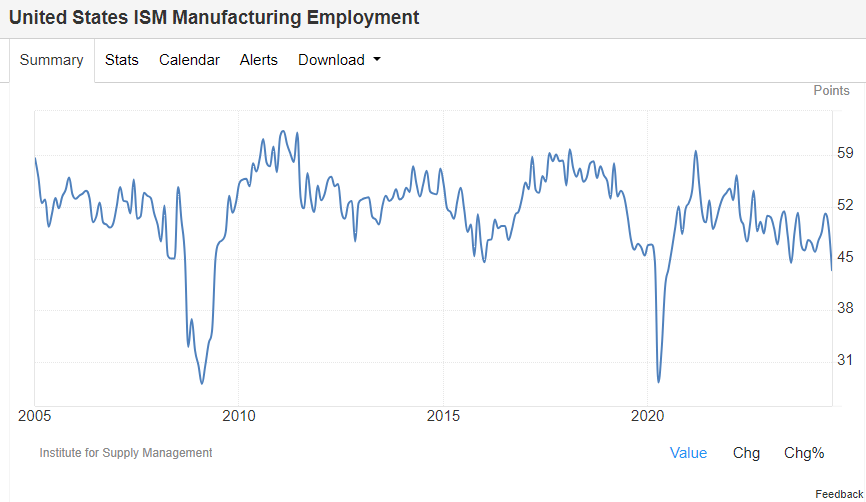

Mega bears love the ISM manufacturing employment gauge being down to Sept 2008 levels. While they take it as a true sign of collapse, anyone who lived through '08 knows that this just indicates that the survey doesn't pass the common sense test and should be ignored.

Overall we are also seeing signs of some modest easing of pressure on wages as the incremental bid for employment has slowed. But across most measures, demand and wage growth remains elevated vs. pre-covid levels.

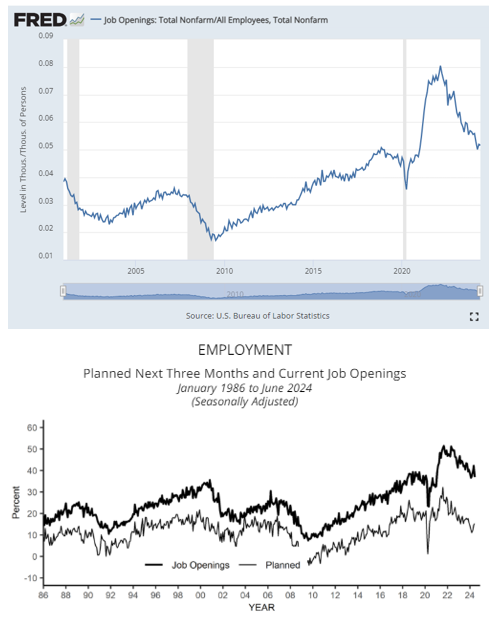

Openings have come down but are above '20 and for a few months:

Openings have come down but are above '20 and for a few months:

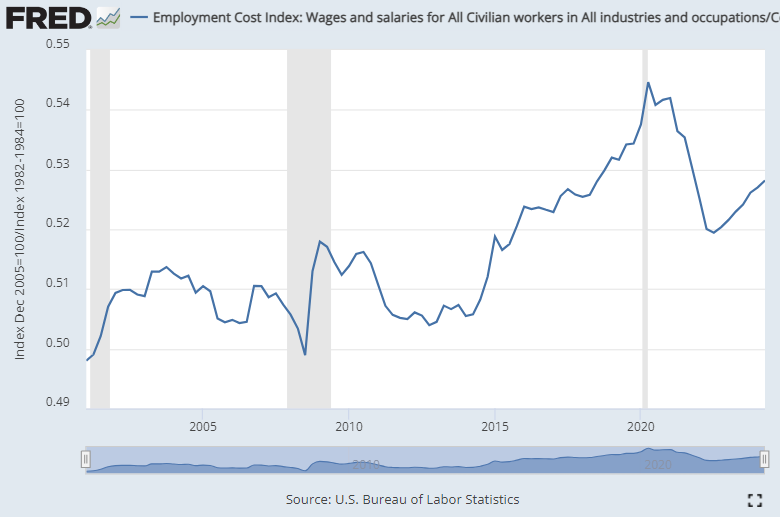

The most comprehensive measure of wage growth - ECI - had a soft print for 2Q for the important wages and salaries line (most spending happens from income), though its a bit of an outlier relative to stronger quarters before. Either way, clearly above pre-covid.

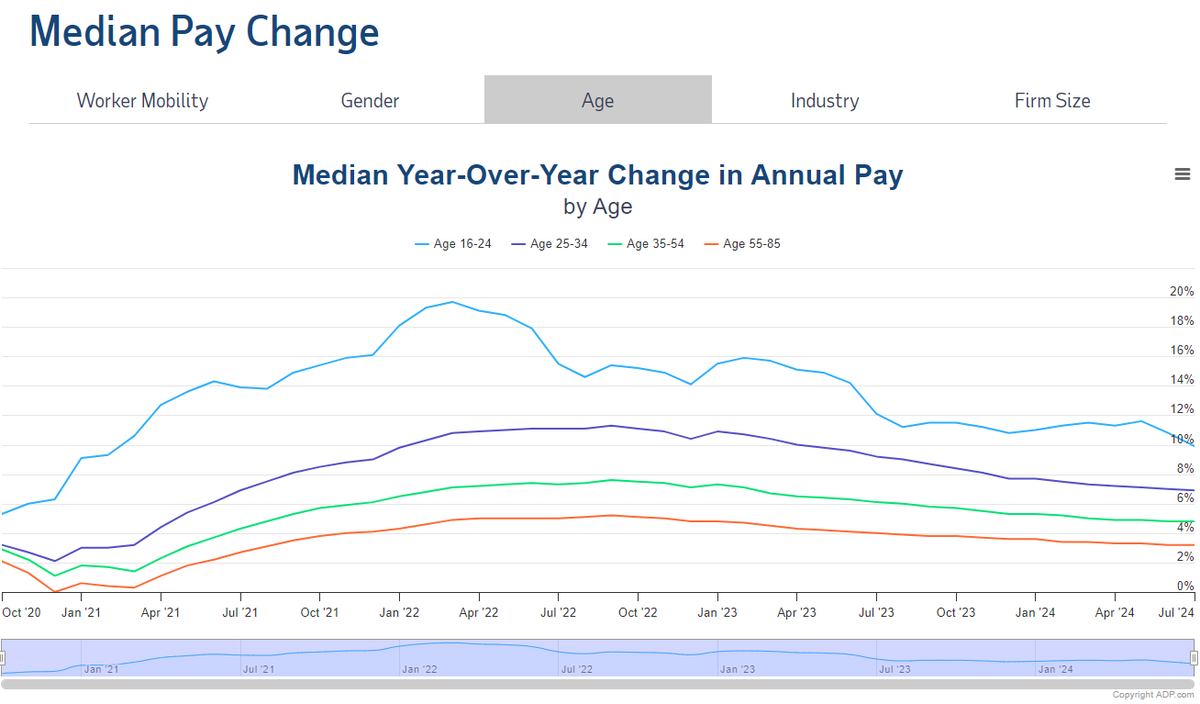

The ADP pay insights numbers suggest very gradual slowing, with a bit of a tick down in July particularly with lower-income cohorts (here proxied by age). Still above pre-covid levels of growth, particularly for lower income earners.

This suggests that even though labor market demand may be in the ballpark of pre-covid levels, pressures on nominal wage growth may persist given that wage income remains pretty depressed in real terms relative to pre-covid levels. Aways to go on this "catch up" for workers:

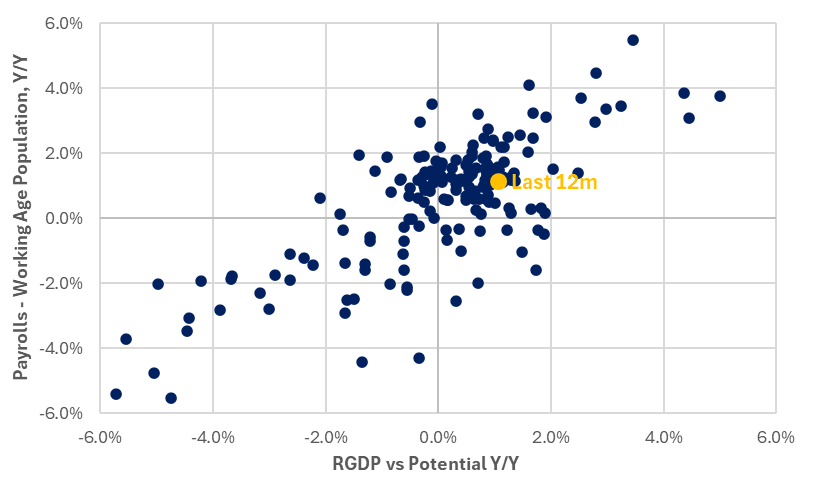

Reports today are just one lens into what is going on with labor market conditions and these other reports help triangulate the picture. Like the overall growth measures, most employment measures show only modest cooling. The UE rate may be the outlier:

https://x.com/BobEUnlimited/status/1818966188426461189

The Fed responds to the macro data, and typically aggressive easing cycles only come when there is (or a relatively extreme expectation of) deterioration in the labor market. The broad set of data looks consistent with JP's views of gradual cooling and normalization.

Hopes that swift cuts are coming because of a fast labor market deterioration are unlikely to come true given the data and likely trajectory at this point.

And for many investors, hopes of those fast cuts are all that is propping up the stock market at this point.

And for many investors, hopes of those fast cuts are all that is propping up the stock market at this point.

• • •

Missing some Tweet in this thread? You can try to

force a refresh