1/2025 Forecast Thread

This thread will cover the entirely of my 2025 Tesla forecast. I will cover all the individual elements that contribute to each of Tesla’s businesses.

This analysis was originally shared with subscribers on Oct 27.

First, let’s take a look at the key findings from the model. There are 4 scenarios, each with an estimated average probability of occurring:

- Base Case (40% probability)

- Bear Case (30% probability)

- Bull Case (29.5% probability)

- Uber Bull Case (0.5% probability)

Each of these scenarios leads to a unique EPS calculation. The weighted average of each scenario is what is used to provide the 2025 FC of $3.99/shr in adjusted earnings per share. This compares to the estimated 2024 eps target of $2.47 and estimated 2025 eps target of $3.24 – both of these from Yahoo Finance.

Please note: Cells shaded in yellow are INPUTS, while cells shaded in white are results from calculations/formulas which derive from one of the other inputs either on the main table, or from other tables.

Overall, we can see that I think Tesla has a higher probability of over-achieving in 2025 vs the market expectations. Key assumptions driving this:

- Surging energy volume and sales at a healthy gross margin.

- Expansion of operating leverage as revenue growth outpaces growth in operating expenses.

- Stabilizing automotive gross margin due to:

1. Model Y refresh spurring organic demand and limiting need for future price cuts (above and beyond what we see in Q4-24).

2. Interest rates declining globally which will help Tesla reduce its financing costs to maintain aggressive vehicle financing rates.

3. Cost/vehicle decline mostly driven by much better factory utilization – especially in Austin and Berlin.

4. Still high regulatory credit sales.

I will first cover my assumptions for Energy since Energy volume and sales remain the same in all scenarios.

This thread will cover the entirely of my 2025 Tesla forecast. I will cover all the individual elements that contribute to each of Tesla’s businesses.

This analysis was originally shared with subscribers on Oct 27.

First, let’s take a look at the key findings from the model. There are 4 scenarios, each with an estimated average probability of occurring:

- Base Case (40% probability)

- Bear Case (30% probability)

- Bull Case (29.5% probability)

- Uber Bull Case (0.5% probability)

Each of these scenarios leads to a unique EPS calculation. The weighted average of each scenario is what is used to provide the 2025 FC of $3.99/shr in adjusted earnings per share. This compares to the estimated 2024 eps target of $2.47 and estimated 2025 eps target of $3.24 – both of these from Yahoo Finance.

Please note: Cells shaded in yellow are INPUTS, while cells shaded in white are results from calculations/formulas which derive from one of the other inputs either on the main table, or from other tables.

Overall, we can see that I think Tesla has a higher probability of over-achieving in 2025 vs the market expectations. Key assumptions driving this:

- Surging energy volume and sales at a healthy gross margin.

- Expansion of operating leverage as revenue growth outpaces growth in operating expenses.

- Stabilizing automotive gross margin due to:

1. Model Y refresh spurring organic demand and limiting need for future price cuts (above and beyond what we see in Q4-24).

2. Interest rates declining globally which will help Tesla reduce its financing costs to maintain aggressive vehicle financing rates.

3. Cost/vehicle decline mostly driven by much better factory utilization – especially in Austin and Berlin.

4. Still high regulatory credit sales.

I will first cover my assumptions for Energy since Energy volume and sales remain the same in all scenarios.

2/ENERGY

Powerwall

I used 260k for sales in 2025 because Tesla is currently installing Powerwall at a rate of 260k/year (company post). This means sales probably exceed 260k/yr since Powerwall is sold to 3rd parties that carry a small inventory. 260k is therefore conservative because it doesn’t account for the inventory and it assumes no growth in sales rate, when Tesla has consistently shown growth in sales rate over the years (see screenshot of my post).

$9,300 is what Tesla currently sells Powerwall for. This yields 3.51 GWh of storage and ~$2.4B in sales for the year.

Megapack

Lathrop hit maximum production capacity in Q3-24 and is now building close to ~10k Megapacks/year. But while Tesla may be building 10k/yr, I am assuming they will only fully recognize the sale of 8.5k Megapacks in 2025 to account for the fact that revenue is recognized in stages and they probably won’t reach a perfect steady state where production = sales, because there is a lag time between sale and revenue. I also assumed a further 10% decrease in Megapack price on average for 2025.

Shanghai is expected to begin operations in Q1-25 and the factory is targeting a production rate of ~5k Megapacks/year to start. China is exceptional at ramping production and they may even exceed this. However, I am assuming – probably conservatively – that over the course of 2025, they will only sell 4k Megapacks.

At 3.9 MWh per Megapack, Tesla is projected to install 48.8 GWh of Megapack for $12.7B in 2025.

Where my Energy forecast differs between scenarios is in the margin assumption. My gross margin assumptions are as follows:

- Base case = 27.5%

- Bear case = 23%

- Bulls case = 30%

- Uber bull case = 30%

Given the excess battery supply in China, the falling battery component costs, the expanded factory utilization in Lathrop, and the high ongoing demand for battery storage globally, I think we should expect energy margin to stay high. My base case may even be conservative given that gross margin exceeded 30% in Q3 and I wouldn’t be shocked to see it increase further in Q4.

Solar sales are irrelevant to the analysis because they are small and I assume gross margin is either 0 or low single digit negative.

Powerwall

I used 260k for sales in 2025 because Tesla is currently installing Powerwall at a rate of 260k/year (company post). This means sales probably exceed 260k/yr since Powerwall is sold to 3rd parties that carry a small inventory. 260k is therefore conservative because it doesn’t account for the inventory and it assumes no growth in sales rate, when Tesla has consistently shown growth in sales rate over the years (see screenshot of my post).

$9,300 is what Tesla currently sells Powerwall for. This yields 3.51 GWh of storage and ~$2.4B in sales for the year.

Megapack

Lathrop hit maximum production capacity in Q3-24 and is now building close to ~10k Megapacks/year. But while Tesla may be building 10k/yr, I am assuming they will only fully recognize the sale of 8.5k Megapacks in 2025 to account for the fact that revenue is recognized in stages and they probably won’t reach a perfect steady state where production = sales, because there is a lag time between sale and revenue. I also assumed a further 10% decrease in Megapack price on average for 2025.

Shanghai is expected to begin operations in Q1-25 and the factory is targeting a production rate of ~5k Megapacks/year to start. China is exceptional at ramping production and they may even exceed this. However, I am assuming – probably conservatively – that over the course of 2025, they will only sell 4k Megapacks.

At 3.9 MWh per Megapack, Tesla is projected to install 48.8 GWh of Megapack for $12.7B in 2025.

Where my Energy forecast differs between scenarios is in the margin assumption. My gross margin assumptions are as follows:

- Base case = 27.5%

- Bear case = 23%

- Bulls case = 30%

- Uber bull case = 30%

Given the excess battery supply in China, the falling battery component costs, the expanded factory utilization in Lathrop, and the high ongoing demand for battery storage globally, I think we should expect energy margin to stay high. My base case may even be conservative given that gross margin exceeded 30% in Q3 and I wouldn’t be shocked to see it increase further in Q4.

Solar sales are irrelevant to the analysis because they are small and I assume gross margin is either 0 or low single digit negative.

3/SERVICES AND OTHER

Next, let’s cover the assumptions for Services and Other. Here too, the revenue assumption is the same but the margin assumption changes by scenario. If we look at the Services and Other segment by quarter, you will notice fairly linear growth every quarter. This makes sense when we consider which revenue items go into this segment: supercharging, service sales, used-car sales, merchandise, etc. As Tesla continues to grow its vehicle fleet, the fleet will steadily require more service…lease returns and follow-up sales are also growing consistently because Tesla’s supply of lease returns is growing consistently. So overall, I think this line will grow steadily every quarter in 2025 and we should land somewhere near $13.6B for the year.

Where my Services and Other forecast differs between scenarios is in the margin assumption. My gross margin assumptions are as follows:

- Base case = 8%

- Bear case = 7%

- Bulls case = 10%

- Uber bull case = 10%

Last quarter’s print was 8.8%, so my 8% is not only realistic, but it is probably conservative. While Tesla isn’t looking to make a substantial profit off this revenue segment, they’re also trying to make sure they manage it well and aren’t bleeding from it.

Next, let’s cover the assumptions for Services and Other. Here too, the revenue assumption is the same but the margin assumption changes by scenario. If we look at the Services and Other segment by quarter, you will notice fairly linear growth every quarter. This makes sense when we consider which revenue items go into this segment: supercharging, service sales, used-car sales, merchandise, etc. As Tesla continues to grow its vehicle fleet, the fleet will steadily require more service…lease returns and follow-up sales are also growing consistently because Tesla’s supply of lease returns is growing consistently. So overall, I think this line will grow steadily every quarter in 2025 and we should land somewhere near $13.6B for the year.

Where my Services and Other forecast differs between scenarios is in the margin assumption. My gross margin assumptions are as follows:

- Base case = 8%

- Bear case = 7%

- Bulls case = 10%

- Uber bull case = 10%

Last quarter’s print was 8.8%, so my 8% is not only realistic, but it is probably conservative. While Tesla isn’t looking to make a substantial profit off this revenue segment, they’re also trying to make sure they manage it well and aren’t bleeding from it.

4/REGULATORY CREDIT SALES

The assumption for 2025 is an average of $700M/quarter. Recall that in the last 2 quarters, Tesla regulatory credit sales were $890M in Q2 and $739M in Q3, respectively. I think $700M/quarter is very reasonable considering that legacy auto appears not to be following through on their EV plans and/or are cutting back. This will only mean more credit sales for Tesla. There is risk in this number, however, if President Trump waters down the EPA emission limits however the bulk of that risk would probably only be materialized in 2026+.

Recall that regulatory credit sales carry no cost to Tesla and are therefore recognized at a 100% gross margin.

The assumption for 2025 is an average of $700M/quarter. Recall that in the last 2 quarters, Tesla regulatory credit sales were $890M in Q2 and $739M in Q3, respectively. I think $700M/quarter is very reasonable considering that legacy auto appears not to be following through on their EV plans and/or are cutting back. This will only mean more credit sales for Tesla. There is risk in this number, however, if President Trump waters down the EPA emission limits however the bulk of that risk would probably only be materialized in 2026+.

Recall that regulatory credit sales carry no cost to Tesla and are therefore recognized at a 100% gross margin.

5/AUTOMOTIVE SALES

The biggest component of automotive is obviously vehicle volume sales, so let’s start there. Elon’s guidance on the Q3-24 call was for 20-30% growth in 2024 over a 1.8M vehicle number. 20% growth over 1.8M is 2.16M. 30% growth over 1.8M is 2.34M. My scenarios assume the following delivery numbers:

- Base case = 2.1M

- Bear case = 1.985M

- Bulls case = 2.262M

- Uber bull case = 2.262M

I would prefer to take a conservative approach on volume since I think a lot of it will depend greatly on how well Tesla executes in bringing new models to market…and their track record for bringing new vehicles and/or refreshes of existing vehicles to market suggests that they’re often late. Also, I would rather be conservative in my assumptions and be surprised to the upside. That said, since this is Tesla’s biggest revenue segment, this is the part of my forecast model with the most diversity. The base case, bear case and bull case each have different assumptions for model mix, volume, price and cost. Let’s cover the base case scenario first.

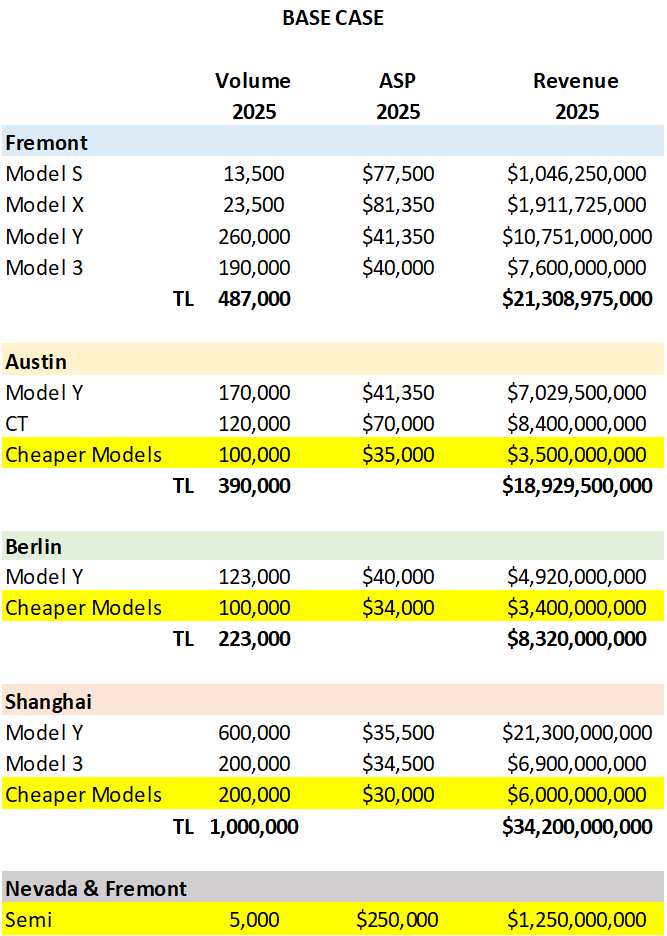

BASE CASE SCENARIO

· Model S/X/3/Y ASP will be stable with Q4-24 (which I expect will decline sequentially from Q3-24). I think higher demand for Model Y refresh and ongoing interest rate cuts from central banks will allow Tesla to maintain ASP with Q4 levels.

· CT ASP to decline to $70k but volume grows to 120k deliveries on the year.

· Tesla Semi sells 5k units at an ASP of $250k/truck. A new class 8 diesel truck costs between $150-270k; assume (conservatively) that Tesla prices it at $250k and lets the customer keep the $40k IRA credit), which would make Semi very reasonably-priced even if the ASP is $250k.

· I have assumed that “cheaper models” – of which I expect there to be several, launch at the beginning of July 2025. Since they are cheaper, I assume the ASP of these vehicles would be ~$4-5k cheaper than the ASP of a Model 3 today…so starting at $35k in the US, $34k in Europe and $30k in China. I am also forecasting that Tesla will build these models in Austin, Shanghai and Berlin – and that Shanghai production/sales will outpace the other 2.

On overall deliveries, I do expect some cannibalization of current versions of 3/Y from the cheaper models, and all of the volume growth in 2025 comes from the launch of these vehicles and CT.

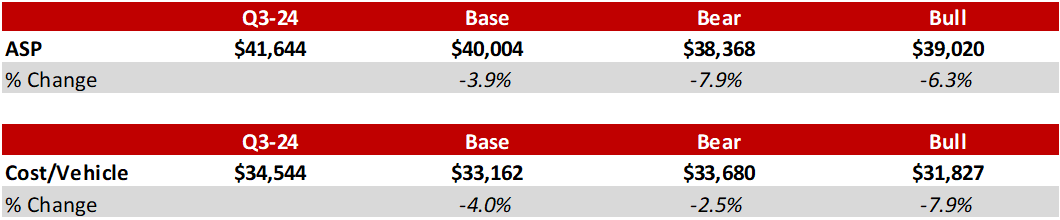

Given these changes, I forecast a ~4% decline in ASP vs Q3-24 levels on a full-year basis. However, given that Tesla’s existing factories are going to be much more productive and that the cheaper models should cost Tesla less to build, I also expect significant cost reductions in 2025. My base case assumes a ~4% decline here as well. When combining both, I see 2025 auto margin excluding credits land exactly at 17.1% - which is in line with the latest Q3-24 print.

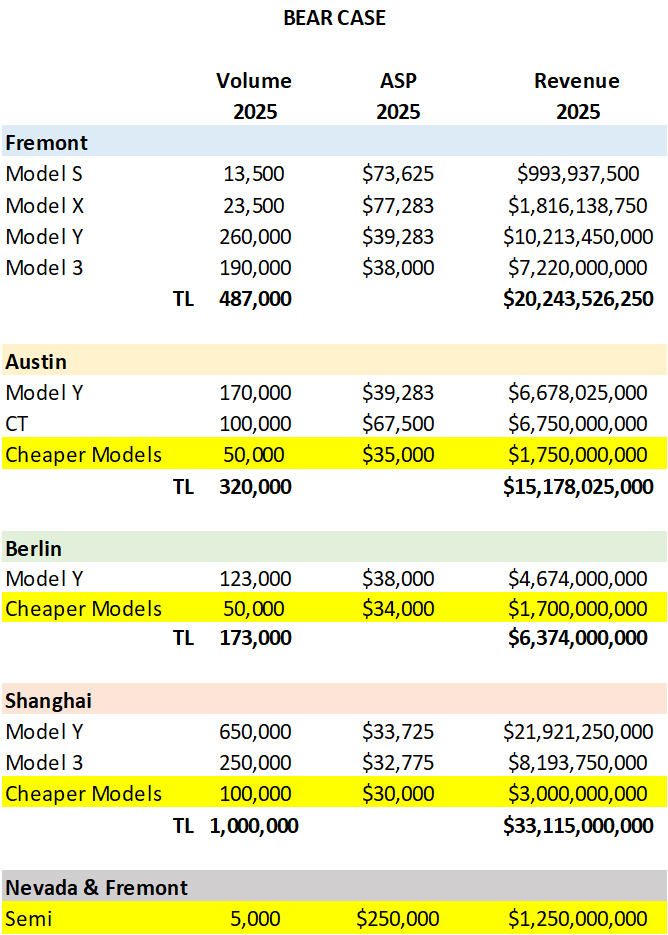

BEAR CASE SCENARIO

The main differences in the auto bear case vs the base case are as follows:

· Slightly higher 3/Y volume case base case, but requiring an additional 5% price cut to achieve it.

· Lower “cheaper model” sales, as Tesla is late in bringing these to market and/or the ramp is very slow.

· Lower CT sales at a slightly lower ASP.

Given the above mentioned scenarios on the revenue side, this yields an ASP decline of ~8% vs Q3-24. Another difference: since Tesla would be selling less volume and less cheaper models than the base case, it is reasonable to assume that costs won’t fall as much. This scenario assumes a -2.5% decline vs Q3-24. When we put both of these factors together, we see auto margin excluding credits to land at 12.2%.

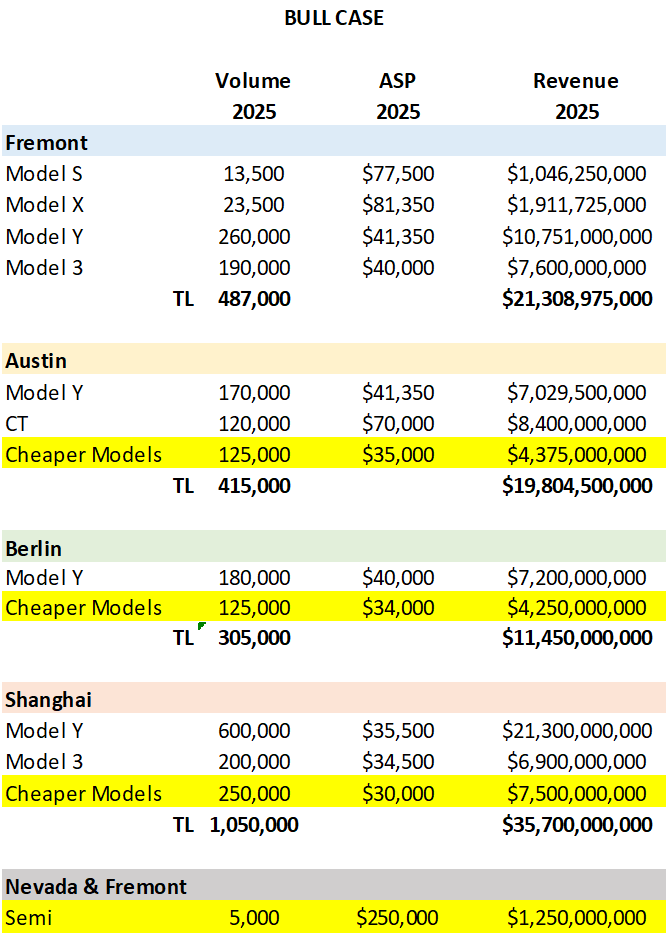

BULL CASE SCENARIO

The main differences in auto bull case vs the base are as follows:

· Slightly higher “cheaper models” sales of 500k vs 400k.

· Less cannibalization of Model Y, so higher Model Y volume sales.

· This model also assumes that 50% of Model Ys and all “cheaper models” made in Austin include Tesla’s made-in-house 4680 battery packs, which unlocks additional value in the form of IRA battery manufacturing credits ($45k/kWh) which directly reduces the cost for Tesla to build these vehicles by ~$3.6k/vehicle.

Given the above mentioned scenarios on the revenue side, this yields an ASP decline of ~6.3% vs Q3-24. However, the 4680 credits and higher volume allows Tesla to bring costs down further, -8% vs Q3-24. Putting both of these together and Tesla would achieve a 18.4% auto margin excluding regulatory credit sales.

The biggest component of automotive is obviously vehicle volume sales, so let’s start there. Elon’s guidance on the Q3-24 call was for 20-30% growth in 2024 over a 1.8M vehicle number. 20% growth over 1.8M is 2.16M. 30% growth over 1.8M is 2.34M. My scenarios assume the following delivery numbers:

- Base case = 2.1M

- Bear case = 1.985M

- Bulls case = 2.262M

- Uber bull case = 2.262M

I would prefer to take a conservative approach on volume since I think a lot of it will depend greatly on how well Tesla executes in bringing new models to market…and their track record for bringing new vehicles and/or refreshes of existing vehicles to market suggests that they’re often late. Also, I would rather be conservative in my assumptions and be surprised to the upside. That said, since this is Tesla’s biggest revenue segment, this is the part of my forecast model with the most diversity. The base case, bear case and bull case each have different assumptions for model mix, volume, price and cost. Let’s cover the base case scenario first.

BASE CASE SCENARIO

· Model S/X/3/Y ASP will be stable with Q4-24 (which I expect will decline sequentially from Q3-24). I think higher demand for Model Y refresh and ongoing interest rate cuts from central banks will allow Tesla to maintain ASP with Q4 levels.

· CT ASP to decline to $70k but volume grows to 120k deliveries on the year.

· Tesla Semi sells 5k units at an ASP of $250k/truck. A new class 8 diesel truck costs between $150-270k; assume (conservatively) that Tesla prices it at $250k and lets the customer keep the $40k IRA credit), which would make Semi very reasonably-priced even if the ASP is $250k.

· I have assumed that “cheaper models” – of which I expect there to be several, launch at the beginning of July 2025. Since they are cheaper, I assume the ASP of these vehicles would be ~$4-5k cheaper than the ASP of a Model 3 today…so starting at $35k in the US, $34k in Europe and $30k in China. I am also forecasting that Tesla will build these models in Austin, Shanghai and Berlin – and that Shanghai production/sales will outpace the other 2.

On overall deliveries, I do expect some cannibalization of current versions of 3/Y from the cheaper models, and all of the volume growth in 2025 comes from the launch of these vehicles and CT.

Given these changes, I forecast a ~4% decline in ASP vs Q3-24 levels on a full-year basis. However, given that Tesla’s existing factories are going to be much more productive and that the cheaper models should cost Tesla less to build, I also expect significant cost reductions in 2025. My base case assumes a ~4% decline here as well. When combining both, I see 2025 auto margin excluding credits land exactly at 17.1% - which is in line with the latest Q3-24 print.

BEAR CASE SCENARIO

The main differences in the auto bear case vs the base case are as follows:

· Slightly higher 3/Y volume case base case, but requiring an additional 5% price cut to achieve it.

· Lower “cheaper model” sales, as Tesla is late in bringing these to market and/or the ramp is very slow.

· Lower CT sales at a slightly lower ASP.

Given the above mentioned scenarios on the revenue side, this yields an ASP decline of ~8% vs Q3-24. Another difference: since Tesla would be selling less volume and less cheaper models than the base case, it is reasonable to assume that costs won’t fall as much. This scenario assumes a -2.5% decline vs Q3-24. When we put both of these factors together, we see auto margin excluding credits to land at 12.2%.

BULL CASE SCENARIO

The main differences in auto bull case vs the base are as follows:

· Slightly higher “cheaper models” sales of 500k vs 400k.

· Less cannibalization of Model Y, so higher Model Y volume sales.

· This model also assumes that 50% of Model Ys and all “cheaper models” made in Austin include Tesla’s made-in-house 4680 battery packs, which unlocks additional value in the form of IRA battery manufacturing credits ($45k/kWh) which directly reduces the cost for Tesla to build these vehicles by ~$3.6k/vehicle.

Given the above mentioned scenarios on the revenue side, this yields an ASP decline of ~6.3% vs Q3-24. However, the 4680 credits and higher volume allows Tesla to bring costs down further, -8% vs Q3-24. Putting both of these together and Tesla would achieve a 18.4% auto margin excluding regulatory credit sales.

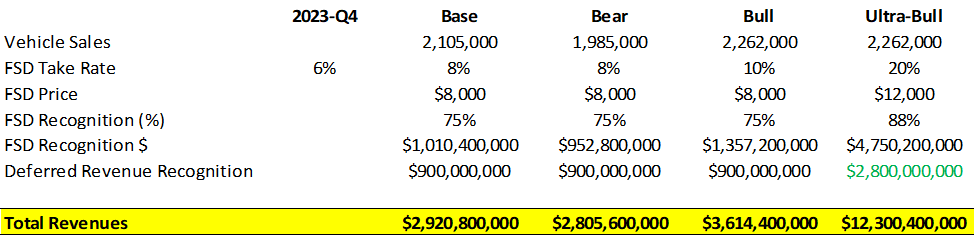

6/FULL SELF-DRIVING (FSD)

In this analysis, Tesla generates FSD revenue from 2 sources:

1. Sale of new vehicles

2. Recognition of deferred revenue

Since volume in the base/bear/bull scenarios are different, the FSD component of each scenario will also differ. Higher volume at the same conversion rate = higher FSD revenue. The other things to consider are FSD conversion rate, and FSD price. The bull case assumes a slightly higher FSD conversion rate than the base and bear cases, at 10% vs 8%. But each of these scenarios assumes that FSD is basically where it is today: supervised FSD with marginal improvements in performance every few weeks.

The standout here is the uber-bull case, and I will explain the assumptions:

1. Tesla launches unsupervised FSD on July 1, 2025.

2. FSD conversion rate increases from 10% in the first half of 2025, to 30% in the second half of 2025.

3. FSD price increases from $8k in the first half of 2025, to $16k in the second half of 2025.

4. Since unsupervised FSD is launched, Tesla recognizes considerably more deferred revenue.

In this analysis, Tesla generates FSD revenue from 2 sources:

1. Sale of new vehicles

2. Recognition of deferred revenue

Since volume in the base/bear/bull scenarios are different, the FSD component of each scenario will also differ. Higher volume at the same conversion rate = higher FSD revenue. The other things to consider are FSD conversion rate, and FSD price. The bull case assumes a slightly higher FSD conversion rate than the base and bear cases, at 10% vs 8%. But each of these scenarios assumes that FSD is basically where it is today: supervised FSD with marginal improvements in performance every few weeks.

The standout here is the uber-bull case, and I will explain the assumptions:

1. Tesla launches unsupervised FSD on July 1, 2025.

2. FSD conversion rate increases from 10% in the first half of 2025, to 30% in the second half of 2025.

3. FSD price increases from $8k in the first half of 2025, to $16k in the second half of 2025.

4. Since unsupervised FSD is launched, Tesla recognizes considerably more deferred revenue.

7. RISKS

While I did try and make conservation assumptions throughout, I would be remiss not to mention any risk associated with the model. Here are some things that could impact my base case assumptions:

1. IRA $7.5k point-of sale credit is eliminated under the Trump administration. This would require Tesla to lower prices to achieve the same level of sales, or it would reduce volume sales.

2. Further fallout from Elon’s role in politics. California is by far Tesla’s US biggest market and any additional demand erosion in the state will be felt.

3. Delays in introducing the “cheaper models.”

4. A rebound in inflation; particularly costs of commodities or labor. This would make it more difficult for Tesla to achieve my cost reduction targets.

While I did try and make conservation assumptions throughout, I would be remiss not to mention any risk associated with the model. Here are some things that could impact my base case assumptions:

1. IRA $7.5k point-of sale credit is eliminated under the Trump administration. This would require Tesla to lower prices to achieve the same level of sales, or it would reduce volume sales.

2. Further fallout from Elon’s role in politics. California is by far Tesla’s US biggest market and any additional demand erosion in the state will be felt.

3. Delays in introducing the “cheaper models.”

4. A rebound in inflation; particularly costs of commodities or labor. This would make it more difficult for Tesla to achieve my cost reduction targets.

8. SUMMARY

2025 is shaping up to be a very strong year which should see volume growth accelerate, margins stabilize and operating leverage expand.

Given the 4 scenarios presented, I expect Tesla to generate ~$4/shr in earnings in 2025 on revenues of ~$120B.

2025 is shaping up to be a very strong year which should see volume growth accelerate, margins stabilize and operating leverage expand.

Given the 4 scenarios presented, I expect Tesla to generate ~$4/shr in earnings in 2025 on revenues of ~$120B.

• • •

Missing some Tweet in this thread? You can try to

force a refresh