Good morning

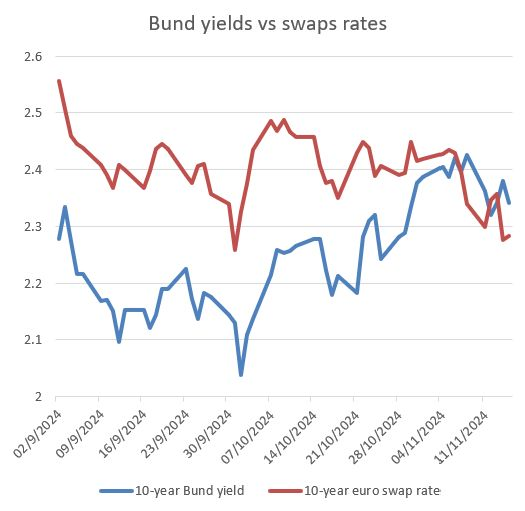

We wrote about 10-year German swap spreads turning negative for the first time in history

What's driving it and why it matters 🧵

ifre.com/story/4954876/…

We wrote about 10-year German swap spreads turning negative for the first time in history

What's driving it and why it matters 🧵

ifre.com/story/4954876/…

Conventional wisdom holds government bonds trade at a premium to swap bc of the higher credit risk facing a bank as swap counterparty

But market dynamics play an important role too

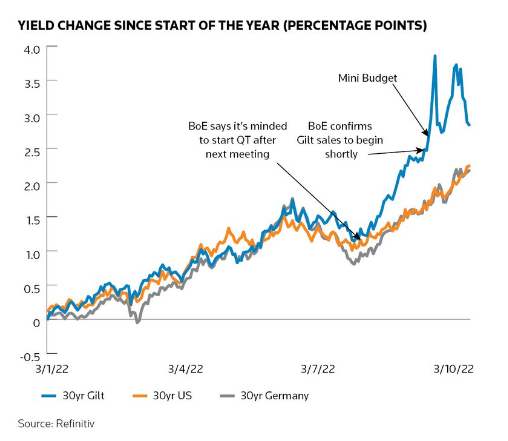

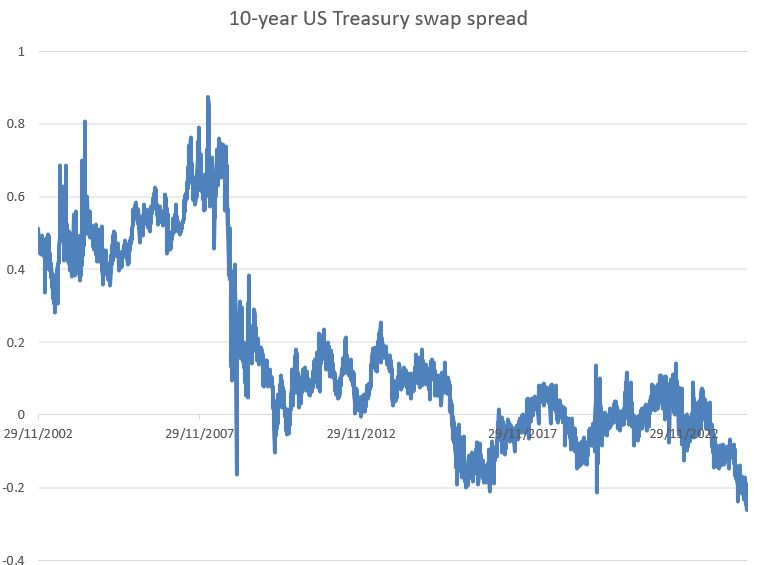

US and UK swap spreads first dipped below zero in the aftermath of the 2008 crisis

But market dynamics play an important role too

US and UK swap spreads first dipped below zero in the aftermath of the 2008 crisis

German bunds proved immune to these pressures thank to a chronic shortage of these securities

1) Germany keeping a tight rein on spending constrained bond supply

and 2) the ECB was buying huge amounts of bonds

Remember stories like this?

wsj.com/articles/ecb-f…

1) Germany keeping a tight rein on spending constrained bond supply

and 2) the ECB was buying huge amounts of bonds

Remember stories like this?

wsj.com/articles/ecb-f…

Fast forward a few years and everything has changed

Inflation has forced central banks to tighten policy and start to unwind QE

And governments have had to loosen the purse strings

In Germany, this triggered the collapse of its ruling coalition

politico.eu/article/german…

Inflation has forced central banks to tighten policy and start to unwind QE

And governments have had to loosen the purse strings

In Germany, this triggered the collapse of its ruling coalition

politico.eu/article/german…

That means more debt issuance when buyers are stepping back - and not just the ECB

Also sovereign wealth funds + bank treasuries (who are nursing paper losses on bond holdings)

Meanwhile, hedging demand remains high from pensions + corporates, pushing swap rates down

Also sovereign wealth funds + bank treasuries (who are nursing paper losses on bond holdings)

Meanwhile, hedging demand remains high from pensions + corporates, pushing swap rates down

Traders report other factors driving swap spreads

Most notably: changing dynamics in repo markets as Bunds become more readily available

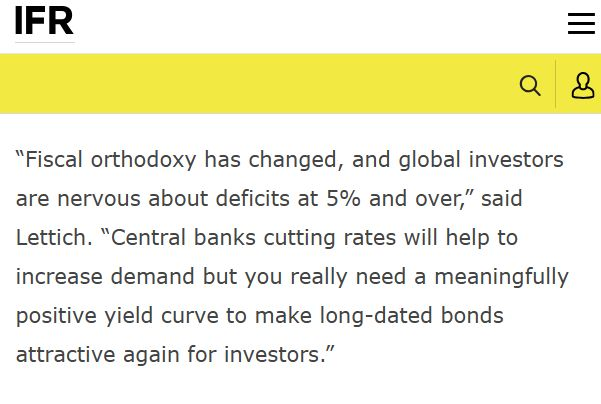

Some are concerned these tensions could deter would-be buyers of government bonds

Most notably: changing dynamics in repo markets as Bunds become more readily available

Some are concerned these tensions could deter would-be buyers of government bonds

Overall, negative swap spreads underline how we're in a new era for government debt w/ wider fiscal deficits + tighter monetary policy

It's no coincidence that US and UK swap spreads have also become more negative since Donald Trump's election victory earlier this month //

It's no coincidence that US and UK swap spreads have also become more negative since Donald Trump's election victory earlier this month //

• • •

Missing some Tweet in this thread? You can try to

force a refresh