This is a long thread about Square Enix, the Microsoft layoffs, AI, and Metcalfe's law.

Fifteen years ago I used to work on the translation of our Annual Reports at Square Enix into English.

One area that often required editing was the word "content." It was a commonly used word in all our IR materials.

The Japanese write コンテンツ (Kontentsu) which is plural ("contents") and I would have to re-edit non-native speaker's edits of "contents" back to the correct "content" because otherwise the report would go out saying Engrish like, "Square Enix provides high quality contents.”

One area that often required editing was the word "content." It was a commonly used word in all our IR materials.

The Japanese write コンテンツ (Kontentsu) which is plural ("contents") and I would have to re-edit non-native speaker's edits of "contents" back to the correct "content" because otherwise the report would go out saying Engrish like, "Square Enix provides high quality contents.”

We used the word “content” a lot because we were in the content business.

We made myriad content: games, manga, anime. Starting in 2004 my boss, CEO Yoichi Wada, began writing in his annual letter to shareholders about the “Network” being the future rather than content. People assumed at the time it was about MMOs.

Of course, that future was years off. In the meantime, we just made content.

We made myriad content: games, manga, anime. Starting in 2004 my boss, CEO Yoichi Wada, began writing in his annual letter to shareholders about the “Network” being the future rather than content. People assumed at the time it was about MMOs.

Of course, that future was years off. In the meantime, we just made content.

In 2004, the word “content” appeared in the Annual Report 90 times. Over time, this went down. In 2024, the word content appeared in the Annual Report a mere 28 times.

Square Enix has spent two decades slowly moving away from being a content business. Not just Square Enix, but every publisher.

Wada-san was right.

The future of games was the Network (here is page 2 of his 2004 Annual Report!).

But the Network business he imagined isn’t about games being online, it’s about the social network of games (Metcalfe’s law) replacing the content business.

Wada-san was right.

The future of games was the Network (here is page 2 of his 2004 Annual Report!).

But the Network business he imagined isn’t about games being online, it’s about the social network of games (Metcalfe’s law) replacing the content business.

The game industry is facing a fundamental realignment. This is not a passing storm. It is a change in the forces that stitched the industry together.

The industry was once defined by scarcity of content. You would consume a game (finish "Super Mario Bros") and move onto the next (start "Legend of Zelda").

Even as the industry transitioned toward richer mediums and even MMOs, it was taken as a basic tenet that games were content: consumers would purchase new games thus building good content and marketing that content would lead to a profitable outcome.

The industry was once defined by scarcity of content. You would consume a game (finish "Super Mario Bros") and move onto the next (start "Legend of Zelda").

Even as the industry transitioned toward richer mediums and even MMOs, it was taken as a basic tenet that games were content: consumers would purchase new games thus building good content and marketing that content would lead to a profitable outcome.

This is the reason why release dates for the biggest titles were set in the fall (best time to sell content into Christmas), and why there was a constant hustle for getting a unique date that didn’t have something like a Call of Duty or Assassin’s Creed also launching that week.

It was similar to the movie business: the movie is named, the date is set (ideally summer), then the content (movie) is made. And studios are constantly jostling to ensure that they didn’t schedule a movie at the same time as direct quadrant competition because the audience’s time was finite.

A portion of the game business still remains this way, but it is crumbling. As I argued last year, the issue with the Final Fantasy series was not that its costs were too high, but that it could not generate the revenue needed.

The audiences expected to play did not come, or were not willing to pay to spend their time. x.com/JNavok/status/…

It was similar to the movie business: the movie is named, the date is set (ideally summer), then the content (movie) is made. And studios are constantly jostling to ensure that they didn’t schedule a movie at the same time as direct quadrant competition because the audience’s time was finite.

A portion of the game business still remains this way, but it is crumbling. As I argued last year, the issue with the Final Fantasy series was not that its costs were too high, but that it could not generate the revenue needed.

The audiences expected to play did not come, or were not willing to pay to spend their time. x.com/JNavok/status/…

To understand why, we have to take a short detour.

Concurrent to the growth of this business was another new market that opened an expanded games: it began with the casuals who first picked up a Wii controller, who then moved onto F2P mobile titles.

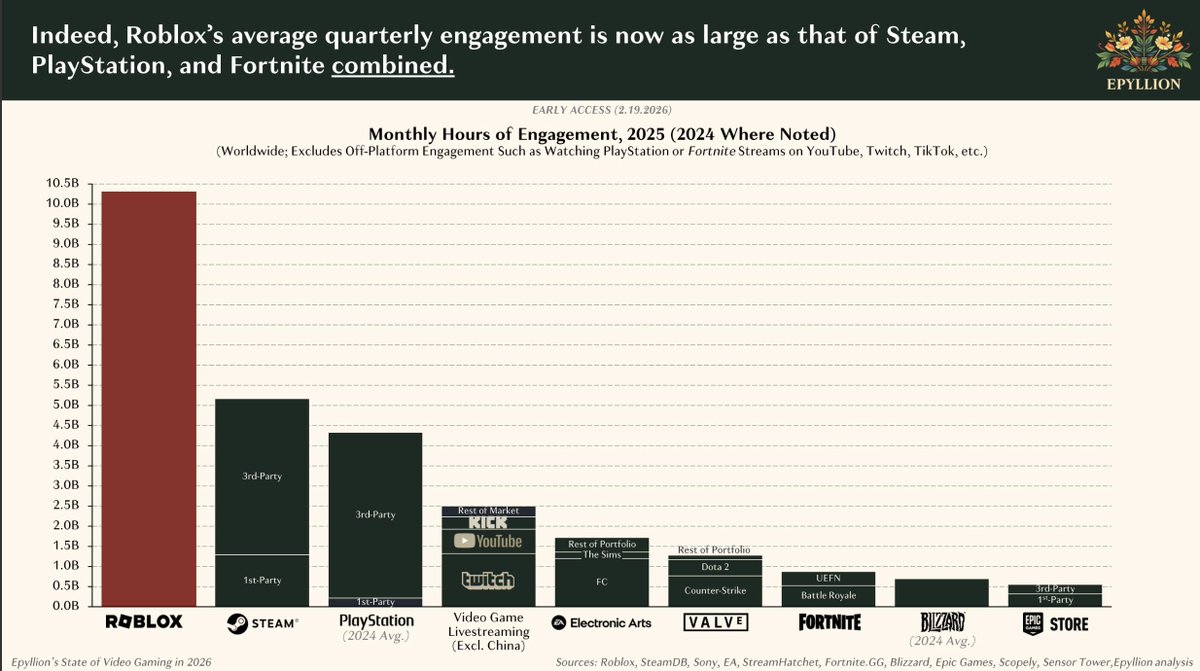

Meanwhile, younger consumers (who in their teens or 20s should be aging into traditional gamers) began engaging with content very differently than the generation of players who grew up with $50 packaged cartridges and then discs. (See chart from @ballmatthew)

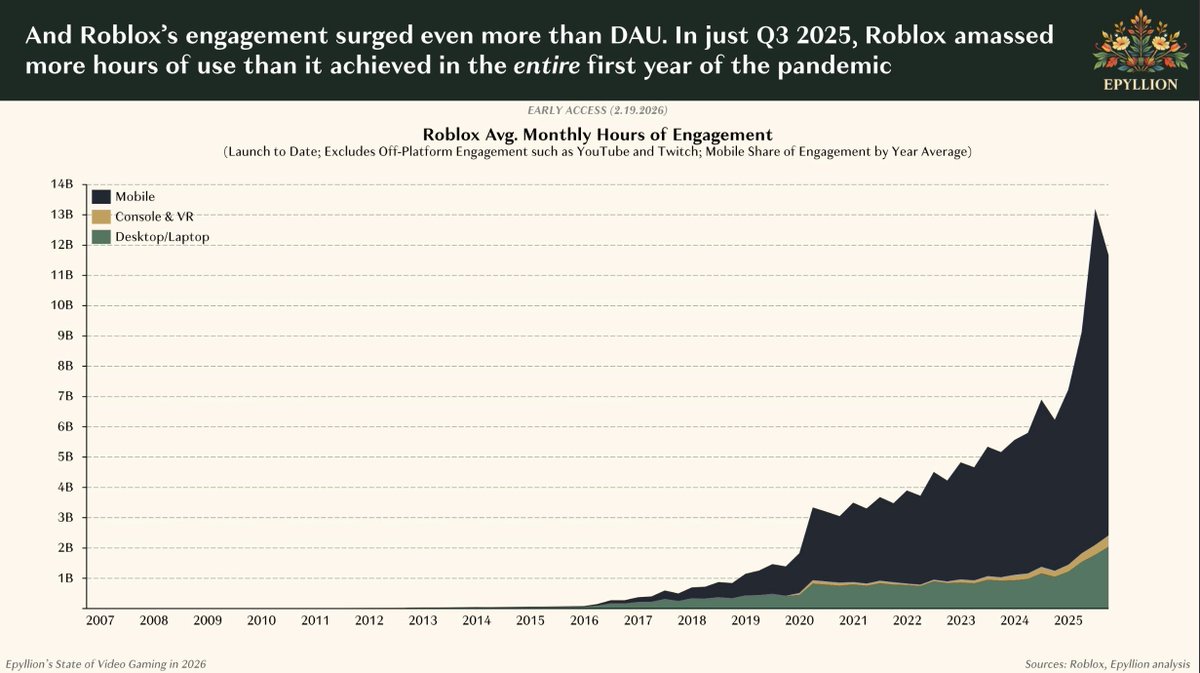

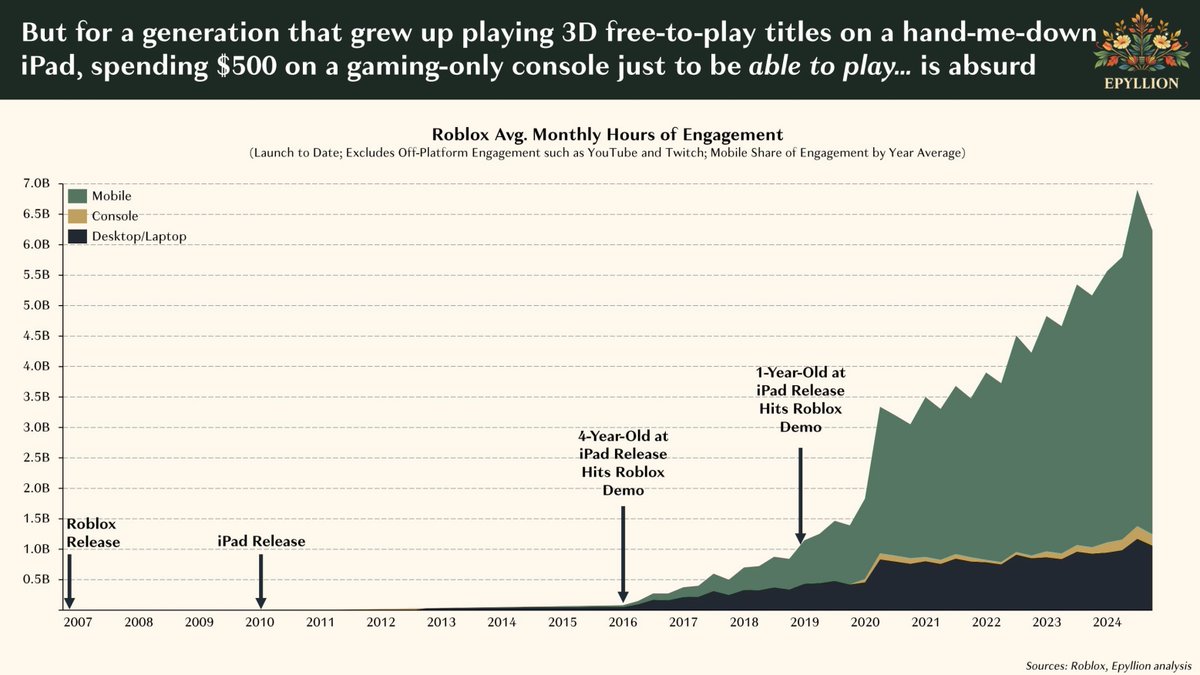

They began with always on titles like Minecraft, and then grew even further with Roblox. The generation of Roblox players have no sense of games as individual pieces of content. Roblox is a platform, and on that platform is an infinite number of experiences. There is no need to leave the platform.

Concurrent to the growth of this business was another new market that opened an expanded games: it began with the casuals who first picked up a Wii controller, who then moved onto F2P mobile titles.

Meanwhile, younger consumers (who in their teens or 20s should be aging into traditional gamers) began engaging with content very differently than the generation of players who grew up with $50 packaged cartridges and then discs. (See chart from @ballmatthew)

They began with always on titles like Minecraft, and then grew even further with Roblox. The generation of Roblox players have no sense of games as individual pieces of content. Roblox is a platform, and on that platform is an infinite number of experiences. There is no need to leave the platform.

The younger generation has stayed with platform titles, graduating in some cases from Roblox to Fortnite, but still staying within ecosystems. Meanwhile the casual business that had shifted to mobile started to stick with dominant forever games (Candy Crush, Clash Royale) that were now acting closer to platforms themselves than pieces of content. (Fortnite is content. It's also a platform. It's also a social network. It's also a tool.)

On top of this came TikTok, nipping at the heels of times spent on console and mobile titles alike.

There is finite time in the day. If TikTok and gambling are growing, something needs to be reduced.

The TikTok feed scratches the same itch as many hyper casual games. Watch, swipe, watch swipe. And the algorithm feeds you a thing that either stimulates you, or doesn’t, and then gets even better at serving you stimulus the more you feed it input.

On top of this came TikTok, nipping at the heels of times spent on console and mobile titles alike.

There is finite time in the day. If TikTok and gambling are growing, something needs to be reduced.

The TikTok feed scratches the same itch as many hyper casual games. Watch, swipe, watch swipe. And the algorithm feeds you a thing that either stimulates you, or doesn’t, and then gets even better at serving you stimulus the more you feed it input.

With competition on time looming and the biggest games becoming platforms, we are left with only the traditional packaged business continuing to function as content. But the number of hours in a day has not changed, and the amount of freely available distraction has. Scarcity is gone; experiences are abundant.

The more platforms (whether Fortnite, CoD, Roblox, Candy Crush, GTA Online, etc.) dominate time spent, the less time there is for traditional, fixed-time content like an Assassin’s Creed: Shadows.

In 2019 the a16z team wrote a piece about trends revolutionizing games, highlighting how games had network effects similar to the best social networking platforms. They were spot on, but these effects benefited the incumbents, not new entrants. (And a16z placed a smart bet on pre-IPO Roblox.) a16z.com/state-of-play-…

The more platforms (whether Fortnite, CoD, Roblox, Candy Crush, GTA Online, etc.) dominate time spent, the less time there is for traditional, fixed-time content like an Assassin’s Creed: Shadows.

In 2019 the a16z team wrote a piece about trends revolutionizing games, highlighting how games had network effects similar to the best social networking platforms. They were spot on, but these effects benefited the incumbents, not new entrants. (And a16z placed a smart bet on pre-IPO Roblox.) a16z.com/state-of-play-…

Games had indeed reached their Network era; but there are very few successful new social networks. In the last decade, the only one that has grown to any prominence to rival Facebook’s blue app and Instagram has been TikTok, with Snapchat having remained relatively small. This means that if games became social networks, there would be few winners.

Basic economics explains this well. Earlier this year, Zynga's "Star Wars: Hunters" shut down.

Let’s say they had 1m players and generated $1m in revenue. (These are nonsense numbers, I’m just making a simple example.)

Let’s say they intended to invest their revenue back into content and thus had a plan to deliver $1m worth of content more in live operations.

Meanwhile, let’s say Fortnite has 100m players and generates $100m in revenue. They can deliver $100m worth of content more in live operations.

My friend who had been playing Star Wars: Hunters said that he ran out of content quickly and thus gave up after a few weeks. He has not stopped playing Fortnite.

With a larger player base and thus revenue base, Fortnite can outspend 99% of developers in the market.

Basic economics explains this well. Earlier this year, Zynga's "Star Wars: Hunters" shut down.

Let’s say they had 1m players and generated $1m in revenue. (These are nonsense numbers, I’m just making a simple example.)

Let’s say they intended to invest their revenue back into content and thus had a plan to deliver $1m worth of content more in live operations.

Meanwhile, let’s say Fortnite has 100m players and generates $100m in revenue. They can deliver $100m worth of content more in live operations.

My friend who had been playing Star Wars: Hunters said that he ran out of content quickly and thus gave up after a few weeks. He has not stopped playing Fortnite.

With a larger player base and thus revenue base, Fortnite can outspend 99% of developers in the market.

You cannot beat the basic economics that their cost of development is covered by much higher demand, enabling them to build more content. This is the transition point: we have moved from a content based business to a social media business based on platforms that can constantly improve thanks to scale.

You used to consume content and move on to the next. Now, content is platform based. This is the difference between a movie (e.g. this week’s upcoming Superman) and YouTube (e.g. this week’s latest Mr. Beast video.) When it comes to digital video platforms, there are only a handful of winners (YouTube, TikTok)- everyone else is simply a creator.

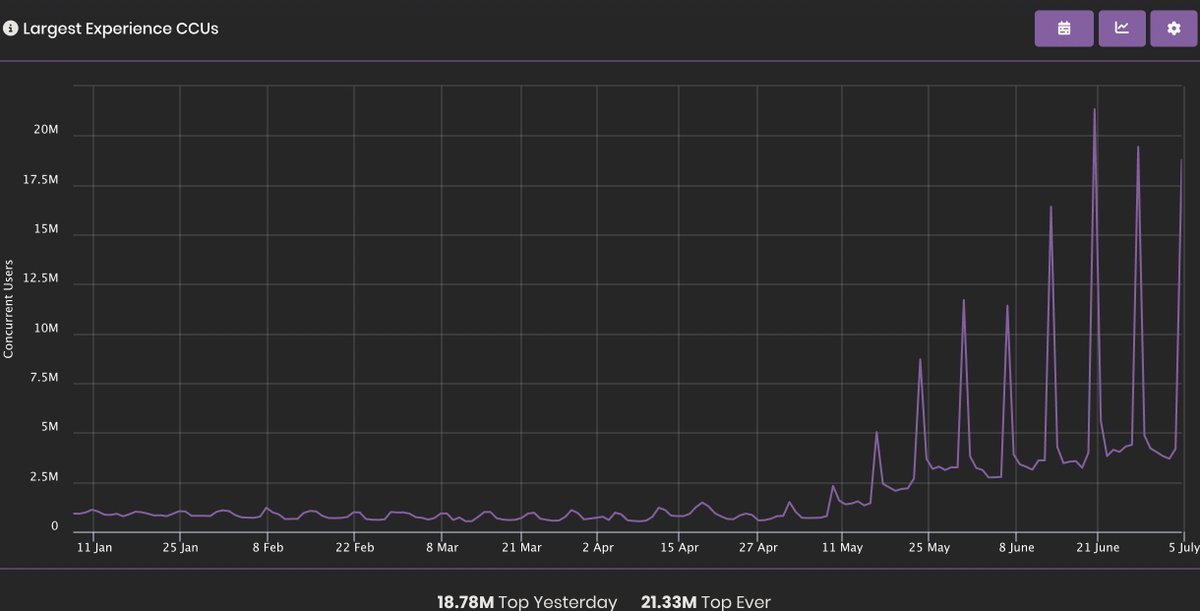

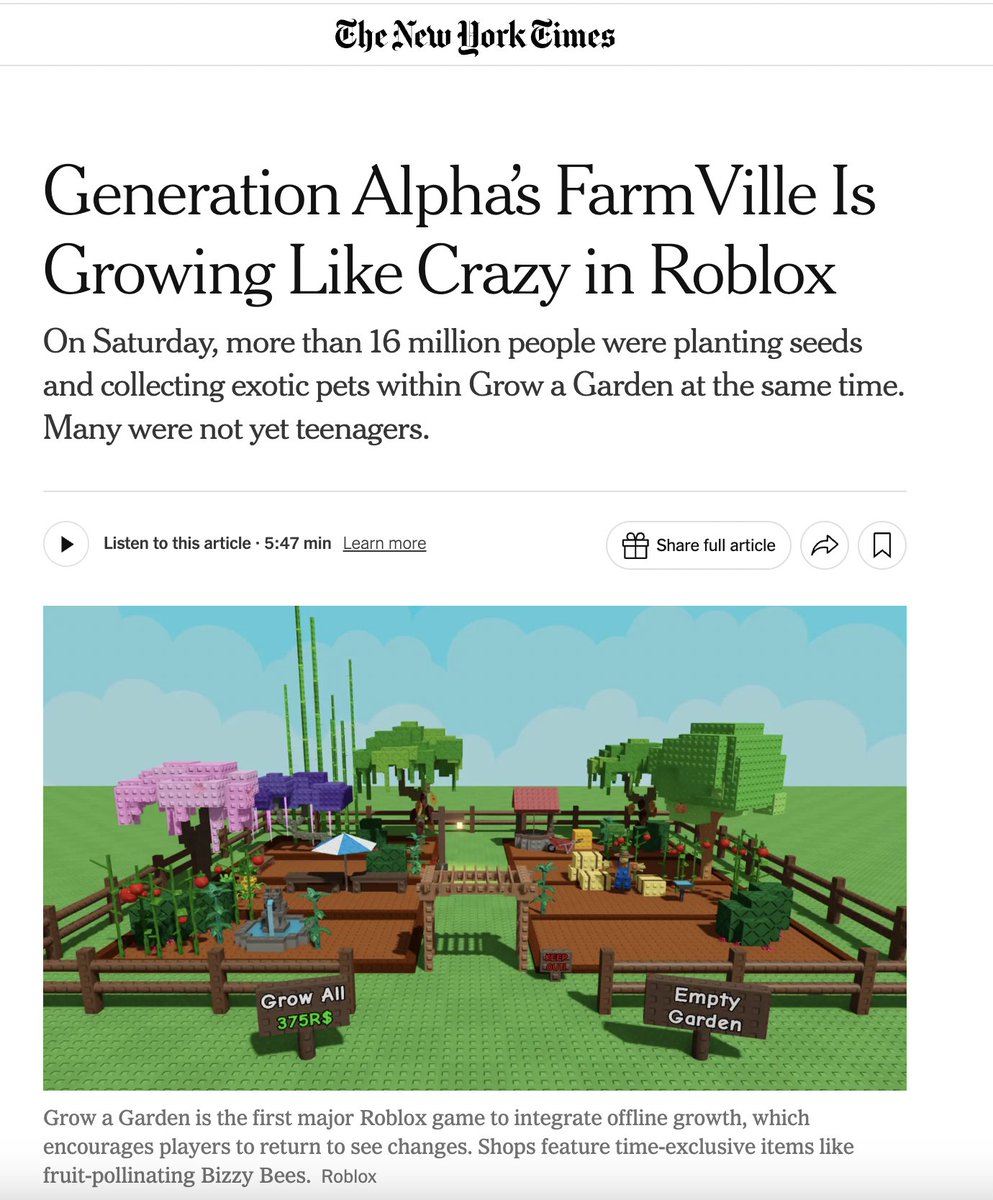

See "Grow a Garden." This Roblox game, in a matter of months, has far surpassed the concurrents of any western game in history, even Fortnite. It may not sustain this, it doesn’t need to. It grew Roblox as a platform tremendously. It made Roblox sticker, enabled more creators to build on Roblox, and brought more users to play Roblox games. Here is Roblox's CCU growth this year.

You used to consume content and move on to the next. Now, content is platform based. This is the difference between a movie (e.g. this week’s upcoming Superman) and YouTube (e.g. this week’s latest Mr. Beast video.) When it comes to digital video platforms, there are only a handful of winners (YouTube, TikTok)- everyone else is simply a creator.

See "Grow a Garden." This Roblox game, in a matter of months, has far surpassed the concurrents of any western game in history, even Fortnite. It may not sustain this, it doesn’t need to. It grew Roblox as a platform tremendously. It made Roblox sticker, enabled more creators to build on Roblox, and brought more users to play Roblox games. Here is Roblox's CCU growth this year.

This does not mean games go away, in the same way that movies or television did not go away with the advent of YouTube.

But we are fighting for time; time does not increase. Tiktok increasingly taking up time that once belonged to more casual play. Hardcore players are aging out, and young players are drawn to Roblox.

This is the problem Microsoft faced in 2025. Phil Spencer is staring down the barrel of an industry that’s changed drastically since he greenlit Perfect Dark’s reboot.

It’s changed drastically even in the few years since they made the case to acquire Activision-Blizzard for $68bn.

The symptoms are becoming clearer.

But we are fighting for time; time does not increase. Tiktok increasingly taking up time that once belonged to more casual play. Hardcore players are aging out, and young players are drawn to Roblox.

This is the problem Microsoft faced in 2025. Phil Spencer is staring down the barrel of an industry that’s changed drastically since he greenlit Perfect Dark’s reboot.

It’s changed drastically even in the few years since they made the case to acquire Activision-Blizzard for $68bn.

The symptoms are becoming clearer.

Prior to 2024, a situation like Concord had never occurred. $400m and eight years of people’s lives gone permanently in two weeks. Zero revenue generated, every sale was refunded.

This is astonishing.

We’d had Duke Nukem Forever incidents before (and Duke Nukem Forever wasn't refunded!), but never something at the scale of Concord.

We have still, as an industry, not truly processed what Concord’s utter collapse meant. We were quick to sweep it under the rug, thinking it was endemic to the quirks of a Hero Shooter.

We cannot ignore what happened to Concord, because it’s about to become the norm.

This is astonishing.

We’d had Duke Nukem Forever incidents before (and Duke Nukem Forever wasn't refunded!), but never something at the scale of Concord.

We have still, as an industry, not truly processed what Concord’s utter collapse meant. We were quick to sweep it under the rug, thinking it was endemic to the quirks of a Hero Shooter.

We cannot ignore what happened to Concord, because it’s about to become the norm.

June 2025 was in fact a critical month for the game industry, though few have written about it.

Nearly $1bn in game investment went into the following games: $400m for Mindseye, $100m for Splitgate 2, hundreds of millions more for Marathon, and tens of millions more for FBC: Firebreak.

These are just four titles that in June announced that their launches or betas had not gone as planned.

All of them plan to make fixes, but how many of us really believe that the market can sustain or expand for these four titles? Again, that’s nearly $1bn in investment between them.

Nearly $1bn in game investment went into the following games: $400m for Mindseye, $100m for Splitgate 2, hundreds of millions more for Marathon, and tens of millions more for FBC: Firebreak.

These are just four titles that in June announced that their launches or betas had not gone as planned.

All of them plan to make fixes, but how many of us really believe that the market can sustain or expand for these four titles? Again, that’s nearly $1bn in investment between them.

Sidenote: FBC: Firebreak was available for free to Gamepass and PS+ subscribers. Splitgate 2 was also free. Don’t be misled by articles like the one in the image below that the industry's problems can be chalked up to Gamepass, a service with barely any growth the last few years.

Gamepass didn’t save FBC, and the competition with Roblox, Fortnite et all. The real problem for FBC is people are playing the wildly successful free games that are driving tens of billions in revenue relative to Gamepass’ more paltry user base and revenue numbers.

Gamepass didn’t save FBC, and the competition with Roblox, Fortnite et all. The real problem for FBC is people are playing the wildly successful free games that are driving tens of billions in revenue relative to Gamepass’ more paltry user base and revenue numbers.

Many have argued that this is a cost problem, saying that we can resolve industry problems by fixing the cost base. Fewer assets, smaller worlds, etc.!

However, thats for AAA and fixing the cost base does not resolve for lack of players. A shorter FF17 is not going to make more demand. We have a serious demand problem, which I argued a few days ago. x.com/JNavok/status/…

I’m going to take a detour here. I’ve seen people shocked at the cost of games. GTAVI will likely cost $2.5bn to develop by the time it is released. Salaries have gone up, crunch has gone down, and team sizes are huge. You have one shot to get an audience- see the June 2025 titles. You need an exceptional title at launch to not be Cyberpunk’d. And so the money is spent.

It can only be this way- the middle is gone. You are either an indie (and I include Clair Obscur as an indie) or you are nine figures.

However, thats for AAA and fixing the cost base does not resolve for lack of players. A shorter FF17 is not going to make more demand. We have a serious demand problem, which I argued a few days ago. x.com/JNavok/status/…

I’m going to take a detour here. I’ve seen people shocked at the cost of games. GTAVI will likely cost $2.5bn to develop by the time it is released. Salaries have gone up, crunch has gone down, and team sizes are huge. You have one shot to get an audience- see the June 2025 titles. You need an exceptional title at launch to not be Cyberpunk’d. And so the money is spent.

It can only be this way- the middle is gone. You are either an indie (and I include Clair Obscur as an indie) or you are nine figures.

Again, this is what the audience wants. It’s silly to blame “suits” at publishers when any flaw in a title is magnified by a thousand YouTubers and Gaming websites saying “Look at this snarky reddit post” gamingbible.com/news/batman-ar…

Management cannot infinitely invest, and the chickens either come home to roost, or the title gets cancelled. (Foreshadowing the MS cancellations last week.)

To that end, we cannot both argue that developers need to be trusted to make games but also realize that it is not management making day to day content decisions in games where there are 100+ people working.

Management did not design a giant yellow trashcan as a main character in Concord. When you spend years to make a game, mistakes get made, and then get compounded.

Management are then asked for more money and time. Eventually the threshold gets passed and this becomes a fool’s errand because demand will never come. Battlefield has this problem too. arstechnica.com/gaming/2025/07…

Management cannot infinitely invest, and the chickens either come home to roost, or the title gets cancelled. (Foreshadowing the MS cancellations last week.)

To that end, we cannot both argue that developers need to be trusted to make games but also realize that it is not management making day to day content decisions in games where there are 100+ people working.

Management did not design a giant yellow trashcan as a main character in Concord. When you spend years to make a game, mistakes get made, and then get compounded.

Management are then asked for more money and time. Eventually the threshold gets passed and this becomes a fool’s errand because demand will never come. Battlefield has this problem too. arstechnica.com/gaming/2025/07…

Additionally, if you think that $400m for Battlefield is too high, or $2.5bn for GTA6 is insane, by definition you are saying those people working on it should not have had jobs.

We cannot expect that everyone should be employed, games can be developed perfectly, and no flaws will be accepted.

That is a completely inconsistent set of arguments yet appears frequently.

We cannot expect that everyone should be employed, games can be developed perfectly, and no flaws will be accepted.

That is a completely inconsistent set of arguments yet appears frequently.

Enter AI.

There are many misunderstandings here. But we should not misconstrue the Microsoft layoffs with them replacing studios with AI.

What happened with Microsoft was clear: AI is a one-in-a-generation change in the entire digital order. MS must either get on board, or perish.

Microsoft lost mobile. Microsoft thrived in cloud because it threw the kitchen sink at Azure. Microsoft cannot lose at AI. I don't mean making game art. I mean in that it will replace many methods of communication and impact all facets of human life.

Based on Xbox profitability over the last 20 years, it is guaranteed that a dollar spent by Satya on Xbox would either be burned or gained a few cents.

A dollar spent on AI will either net 100x back in the future, or all is lost. Satya made his choice, and it was the rational one.

There are many misunderstandings here. But we should not misconstrue the Microsoft layoffs with them replacing studios with AI.

What happened with Microsoft was clear: AI is a one-in-a-generation change in the entire digital order. MS must either get on board, or perish.

Microsoft lost mobile. Microsoft thrived in cloud because it threw the kitchen sink at Azure. Microsoft cannot lose at AI. I don't mean making game art. I mean in that it will replace many methods of communication and impact all facets of human life.

Based on Xbox profitability over the last 20 years, it is guaranteed that a dollar spent by Satya on Xbox would either be burned or gained a few cents.

A dollar spent on AI will either net 100x back in the future, or all is lost. Satya made his choice, and it was the rational one.

What choice does Phil Spencer have when Satya’s decided it for him? MS isn’t a games-only company that needs to live or die by Xbox.

Meanwhile, Phil is a smart guy- he can see that alternatives like the smartphone or PC market is shut out. Mobile is a UA game- Scopely spends billions to buy its customers.

And no one wants to switch from Steam- it has a complete lock on the industry and it is nearly impossible to compete with. (The only opportunity is for Chinese companies, if the Chinese government breaks the greyzone and bans it.)

Phil's market, AAA, is increasingly dominated by an unchanging amount of time spent in the top 5 titles, and GTA6 will only exacerbate this. He had to ask himself, "Would Perfect Dark's Reboot take any measurable amount of time away from Fortnite, GTA6 or CoD? Will it grow the market? If not, should I still spend on it?"

Meanwhile, Phil is a smart guy- he can see that alternatives like the smartphone or PC market is shut out. Mobile is a UA game- Scopely spends billions to buy its customers.

And no one wants to switch from Steam- it has a complete lock on the industry and it is nearly impossible to compete with. (The only opportunity is for Chinese companies, if the Chinese government breaks the greyzone and bans it.)

Phil's market, AAA, is increasingly dominated by an unchanging amount of time spent in the top 5 titles, and GTA6 will only exacerbate this. He had to ask himself, "Would Perfect Dark's Reboot take any measurable amount of time away from Fortnite, GTA6 or CoD? Will it grow the market? If not, should I still spend on it?"

The ultimate ticking time bomb is Roblox and UEFN as the generations that grow up with it continue to stay. I return to the Grow a Garden growth.

This is not coincidence. Gamers who are happy with Roblox and UEFN will stay with it, just as the YouTube generation of kids continues to watch YouTube. This platform effect, Metcalfe’s law, is the future of games, and will continue to grow.

Death Stranding 2 sales, meanwhile, barely passed Clair Obscur in its first three days, and that’s if you generously discount the fact that Clair was free on Gamepass on D1 and grew massively faster shortly after due to good word of mouth (hitting 3.3M copies in its first month, whereas it would normally taper.)

A dollar spent on Death Stranding 2 in this industry is better spent on trying to make a Fortnite (see Phil's dilemma above), which is why Sony will keep trying to make something out of its Bungie acquisition. Marathon will release, but won't solve the problem.

Roblox and Epic already have forever platforms. Sony needs its own, or it will still be in the Content business in a Network business era.

Nintendo may be happy to stay forever as a content business, but I suspect Sony isn't able to say the same.

This is not coincidence. Gamers who are happy with Roblox and UEFN will stay with it, just as the YouTube generation of kids continues to watch YouTube. This platform effect, Metcalfe’s law, is the future of games, and will continue to grow.

Death Stranding 2 sales, meanwhile, barely passed Clair Obscur in its first three days, and that’s if you generously discount the fact that Clair was free on Gamepass on D1 and grew massively faster shortly after due to good word of mouth (hitting 3.3M copies in its first month, whereas it would normally taper.)

A dollar spent on Death Stranding 2 in this industry is better spent on trying to make a Fortnite (see Phil's dilemma above), which is why Sony will keep trying to make something out of its Bungie acquisition. Marathon will release, but won't solve the problem.

Roblox and Epic already have forever platforms. Sony needs its own, or it will still be in the Content business in a Network business era.

Nintendo may be happy to stay forever as a content business, but I suspect Sony isn't able to say the same.

This is where AI comes in -> Tiktok is already a game run by an AI.

The next step is Roblox-like platforms built with AI prompts where kids just enter the type of entertainment they want. They will be build a Matrix-like world in five to ten years. Epic will as well.

These companies have already won, for the same reason that Facebook still prints money 20 years later. People have been distracted by the surface stories about AI and jobs and are missing where the real intersection of games and AI are going.

Replacing an artist with Midjourney does not fix the demand problem. It exacerbates it through more garbage content vying for attention.

The layoffs in the industry are because demand either went away to TikTok, or sat with the platforms, or has an incredibly high bar to get people interested in purchasing. (With the exception of Indies, who are really closer to YouTubers that make it big on Steam as a platform.) What can convince me to play Splitgate 2 over Fortnite, doom scrolling, or Clair Obscur?

You don’t see Strauss Zelnick, CEO of T2, talking about how he’s going to slash his costs on GTA6 by 75% replacing workers with AI, even though he would be handsomely rewarded by Wall Street, not because he doesn’t like being rewarded by Wall Street, but because cost isn’t what keeps him up at night.

It’s the sales of the upcoming title, to which cost is a function. He needs GTA6 to make its own gravity, and be one of those titles rewarded by Metcalfe’s law. He needs to be on the shortlist of winners, cost be damned.

The next step is Roblox-like platforms built with AI prompts where kids just enter the type of entertainment they want. They will be build a Matrix-like world in five to ten years. Epic will as well.

These companies have already won, for the same reason that Facebook still prints money 20 years later. People have been distracted by the surface stories about AI and jobs and are missing where the real intersection of games and AI are going.

Replacing an artist with Midjourney does not fix the demand problem. It exacerbates it through more garbage content vying for attention.

The layoffs in the industry are because demand either went away to TikTok, or sat with the platforms, or has an incredibly high bar to get people interested in purchasing. (With the exception of Indies, who are really closer to YouTubers that make it big on Steam as a platform.) What can convince me to play Splitgate 2 over Fortnite, doom scrolling, or Clair Obscur?

You don’t see Strauss Zelnick, CEO of T2, talking about how he’s going to slash his costs on GTA6 by 75% replacing workers with AI, even though he would be handsomely rewarded by Wall Street, not because he doesn’t like being rewarded by Wall Street, but because cost isn’t what keeps him up at night.

It’s the sales of the upcoming title, to which cost is a function. He needs GTA6 to make its own gravity, and be one of those titles rewarded by Metcalfe’s law. He needs to be on the shortlist of winners, cost be damned.

This is what I think many have failed to grasp. T2, Epic, Roblox’s competition is going to be OpenAI, xAI, etc.

The big tech companies are already making interactive world models that will compete with game experiences.

This is why Mark Zuckerberg moved his bets away from XR and into AI.

That is the battlefield where cutting edge tech and the network effect will merge.

Games, AI, and tech are really part of the same network effect. Metcalfe’s law states that the value of a network is proportional to the square of the number of its users. In other words, the platforms with the most creators and players generate the most value.

When Wada-san predicted in 2004 that Networks will transform the game industry, he meant it from a technical perspective. But he knew, and I know because I spent a decade with him, that ultimately it was about the Network of players.

And so we return to the start. Games are no longer a content business. Square Enix knows it too, but the sun set on their opportunity to transition to a Network business. There were a few million players of Final Fantasy 16.

There have been 14.45bn lifetime plays of Grow a Garden so far, with 21m+ peak CONCURRENTS (meaning lifetime players substantially higher). Microsoft sees this too, which is why Everything (and thus Nothing) is an Xbox.

The future is unfolding before us, and given that we’re all free to spend our time as we wish (and are apparently spending it watching TikTok and playing Grow a Garden)

Metcalfe’s law is the future the majority of the audience have already decided with their wallets and time that they want for games. Apparently that's growing gardens on Roblox.

The big tech companies are already making interactive world models that will compete with game experiences.

This is why Mark Zuckerberg moved his bets away from XR and into AI.

That is the battlefield where cutting edge tech and the network effect will merge.

Games, AI, and tech are really part of the same network effect. Metcalfe’s law states that the value of a network is proportional to the square of the number of its users. In other words, the platforms with the most creators and players generate the most value.

When Wada-san predicted in 2004 that Networks will transform the game industry, he meant it from a technical perspective. But he knew, and I know because I spent a decade with him, that ultimately it was about the Network of players.

And so we return to the start. Games are no longer a content business. Square Enix knows it too, but the sun set on their opportunity to transition to a Network business. There were a few million players of Final Fantasy 16.

There have been 14.45bn lifetime plays of Grow a Garden so far, with 21m+ peak CONCURRENTS (meaning lifetime players substantially higher). Microsoft sees this too, which is why Everything (and thus Nothing) is an Xbox.

The future is unfolding before us, and given that we’re all free to spend our time as we wish (and are apparently spending it watching TikTok and playing Grow a Garden)

Metcalfe’s law is the future the majority of the audience have already decided with their wallets and time that they want for games. Apparently that's growing gardens on Roblox.

• • •

Missing some Tweet in this thread? You can try to

force a refresh