🚨#GSMFoils Q1FY26 concall notes -

👉About the company : GSM Foils is a quality-focused manufacturing of aluminium foil based on primary packaging materials, specifically blister foil and strip foil, which is used for packing tablets and capsules in the pharmaceutical industries.

A thread 🧵 (1/n)👇

👉About the company : GSM Foils is a quality-focused manufacturing of aluminium foil based on primary packaging materials, specifically blister foil and strip foil, which is used for packing tablets and capsules in the pharmaceutical industries.

A thread 🧵 (1/n)👇

👉Clients & Manufacturing capacity : With more than 65 active pharmaceutical clients across 14 states in India, we have built a reputation for customization, quality, and reliability. We operate from the state-of-the-art facility in Vasai, Maharashtra, certified by an ISO 9001-2015, with an installed capacity of over 10,000 metric tons per annum.

(2/n)

(2/n)

👉Sector size : Indian pharma sector is expected to grow from almost $65 billion in 2024 to $130 billion by 2030. Along this, the Indian packaging sector is also witnessing a strong momentum and is projected to reach almost a USD dollar of $205 billion by 2025 ending.

(3/n)

(3/n)

👉Govt. policy support : As a part of its efforts to strengthen the sector, the Government of India has recently imposed a five-year anti-dumping duty on aluminum foil from imports from China and Thailand, aiming to corrupt the low-cost inflow and promoting market stability.

(4/n)

(4/n)

👉Backward Integration : We have recently ventured into the trading of aluminum-based foil in Lamitubes, with a strategic step to broaden our product portfolio and cater to the existing segment with the same pharmaceutical packaging sector that we are. As a part of our long-term vision, we also intend to extend the manufacturing facility of Lamitubes by the end of this financial year to ensure value addition and improved margin control. These capex align with the goal of creating a backward integration in a value-accelerated business that reduces external dependency and strengthens our internal capacity

(5/n)

(5/n)

👉EBITDA guidance for FY26 : So we are certainly looking at, if you're talking about gross margin, then roughly around 11% to 12%, which is quite sustainable. We'll try a more 100 to 200 basis points if everything goes well, yes. For now, we are quite confident of sustaining 11% to 12%.

(6/n)

(6/n)

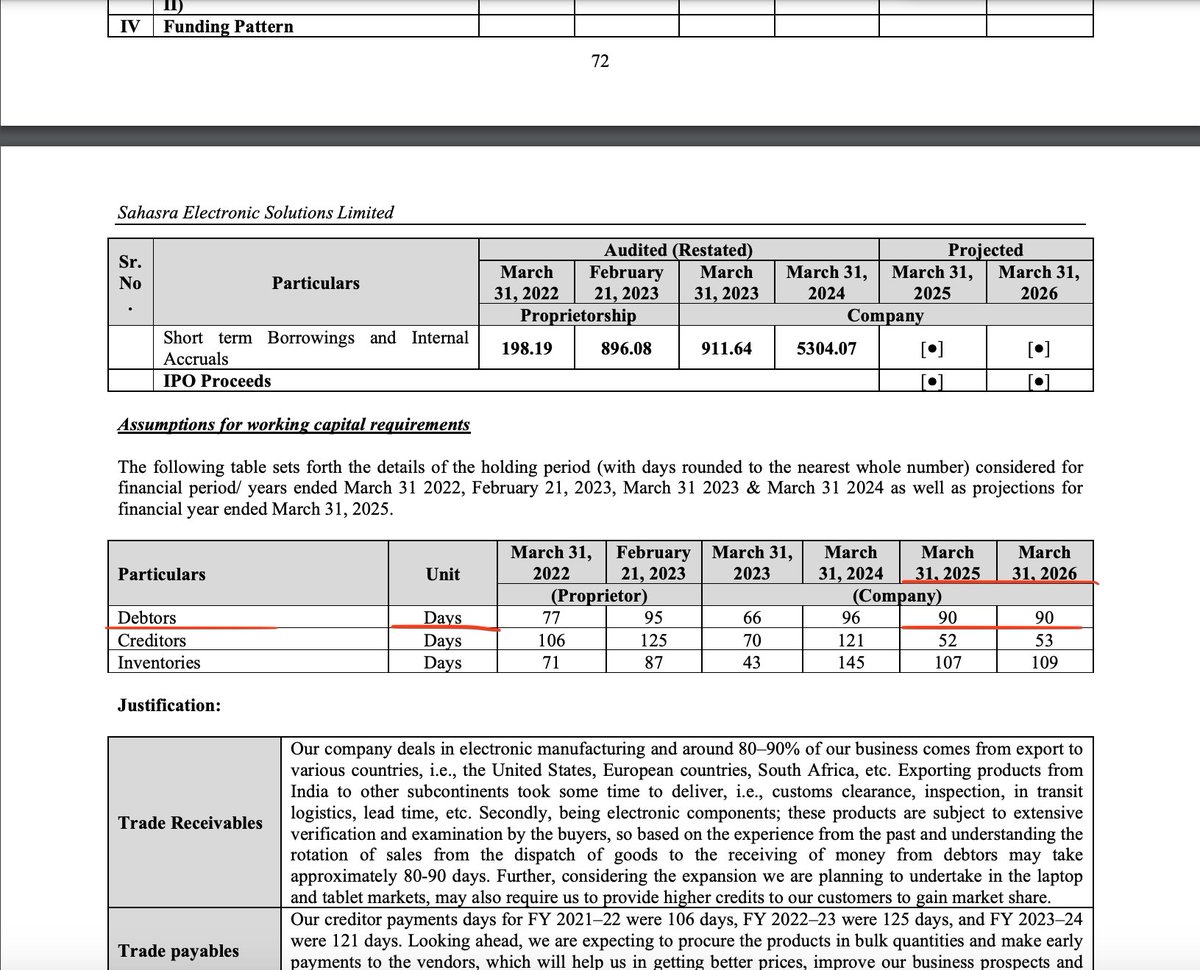

👉Working Capital Days : Working capital right now is 71 days, we are trying to bring that to around 60 to 65 days. So it won't go above that.

(7/n)

(7/n)

👉Ahmedabad plant capex : firstly would be machinery capex of around INR4 crores to INR5 crores, then the working capital also. So debt of around INR12 crores to INR15 crores we are planning.

(8/n)

(8/n)

👉Lamitube segment : Currently, we are doing around turnover of 1-1.5 per month and let's suppose this expansion and capex, we can aim at a very nominal figure I am telling about INR8 crores to INR10 crores can be easily achieved. This in FY27. Even Lamitube are very big markets.

👉Debt : Approx. 35cr after 10-12cr further raise

(9/n)

👉Debt : Approx. 35cr after 10-12cr further raise

(9/n)

👉Client Payment default : There are zero bad debts in the last 5 years that I'm working in this industry. There are ifs and buts like payment normally get delays like from 60 to 70, 75 days, but there are no payment default in pharma industry

(10/n)

(10/n)

👉Risks in the business : So the only major risk factor is like, I told you, the plus point is we are able to manage working capital well. So vis-a-vis the risk is also that once we are not able to manage that well, you will see a sales figure going down. You will see a tremendous rise in our debtors days. Debtors figures will go up. Inventories would go down. Effectively, the cycle would slow down. We won't be able to buy more material. And eventually, sales would go down. So that is your benefit. And eventually, that is your risk also. So the entire game depends upon how well you churn your fund. Like if you're doing it 5x to 6x in the entire year, you're doing it really well. You're doing 6x to 7x, then you're doing excellent. But once you're able to do that like 3x to 4x, then definitely there's a risk in your industry, in your company.

(n/n)

(n/n)

• • •

Missing some Tweet in this thread? You can try to

force a refresh