We are short $STRL, a poster child for the AI bubble. Data center exposure appears exaggerated. Backlog growth is not supported by contract win data. Margins look inflated. The stock is expensive even vs AI darlings like $NVDA. We see 60-80% downside.

Report at snowcapresearch.com

Report at snowcapresearch.com

1/ Sterling Infrastructure is not a data center infrastructure company. It owns a collection of regional contractors that specialize in site preparation and excavation services – clearing and grading land before foundations are laid.

2/ In 2022, Sterling rebranded one of its segments as “E-Infrastructure” and began positioning itself to investors as a “picks-and-shovels” play on the AI boom. Since then, its stock has increased nearly twenty-fold, outperforming even marquee AI beneficiaries like $NVDA.

3/ Management is coy in its disclosures, but the implication is unmistakable: data centers make up the bulk of Sterling’s E-Infrastructure business, and the remainder consists of high-margin “mission critical” customers such as chip fabrication plants.

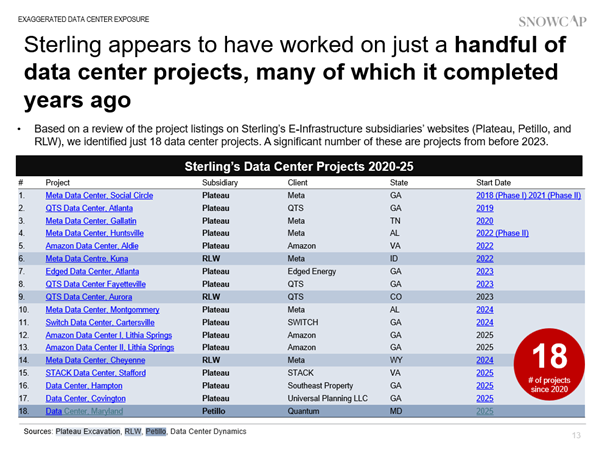

4/ We undertook a detailed review of hundreds of individual projects showcased on the websites of Sterling’s subsidiaries. In total, we counted just 18 data center projects since 2020 – a far cry from the “100 or so” implied by management.

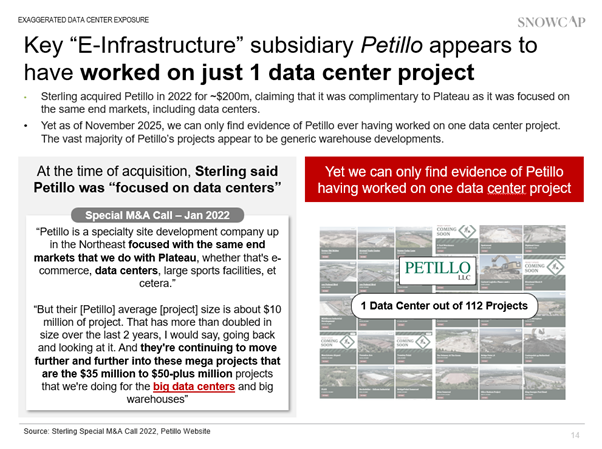

5/ Most strikingly, the second largest subsidiary in Sterling’s E-Infrastructure segment - Petillo - appears to have worked on just one data center project since it was acquired in 2021.

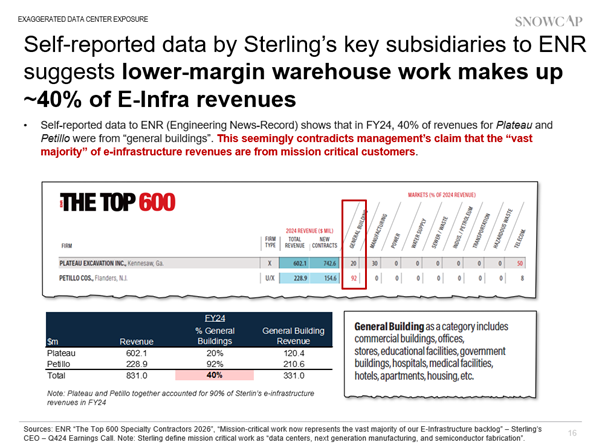

6/ We uncovered recently published data from Sterling’s flagship E-Infra subsidiaries - which indicates 40% of their revenues are from lower-margin warehouses. This contradicts management’s claim that the “vast majority” of E-Infra revenues are mission critical.

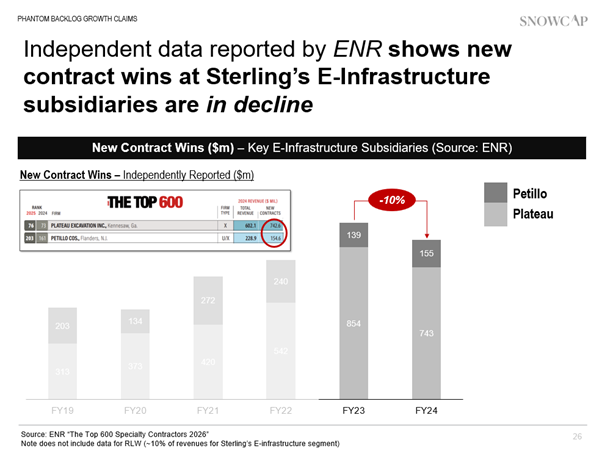

7/ Despite supposedly soaring demand from data center projects, Sterling’s flagship e-infrastructure revenues have been remarkably stagnant. Instead, the Company’s growth narrative hinges entirely on its backlog, which it claims has grown at a 40% CAGR.

8/ We are skeptical. Self-reported data to ENR shows that new contract wins at Sterling‘s flagship subsidiaries are in decline and have also barely eclipsed revenues in recent years. By our calculation, ~75% of claimed backlog growth since 2022 is unexplained.

9/ Sterling's margins look implausibly high. If half of E-infra revenues are lower-margin work (~15% gross margins by our estimate), the implied data center margins are 45%+. Competitors told us 30% was best-case and expressed skepticism over the sustainability of $STRL’s margins.

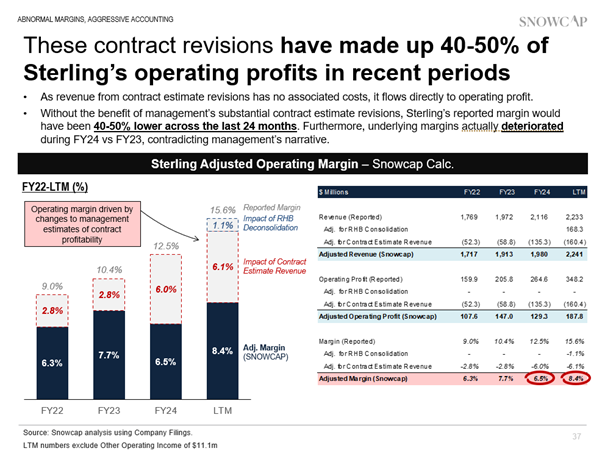

10/ Buried deep in its 10-K, Sterling reveals that a staggering ~45% of EBIT since 2023 has been driven by abnormally large accounting revisions – which essentially relate to estimates of future profitability. Sterling’s auditor flagged the revisions as a key area of uncertainty.

11/ Particularly troubling, given the extraordinary degree of discretion embedded in Sterling's accounting, is the instability in the CFO role. Since May 2024, the Company has seen two CFO departures in quick succession — the most recent lasting less than a year.

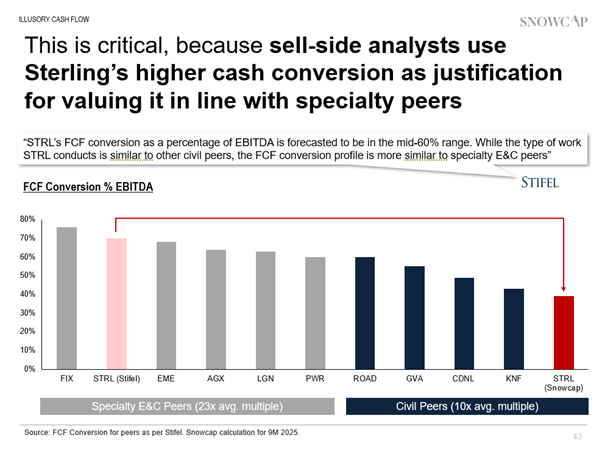

12/ Investors have likely overlooked this, taking comfort in Sterling’s cash flow. This is a mistake. Sterling’s cash flow has been propped up by a one-time benefit from advanced billings. Strip these out and Sterling’s cash conversion collapses to just 40% in 9M25.

13/ This is also critical because sell-side analysts use Sterling’s higher cash conversion as crucial justification for valuing it in line with specialty peers - which trade at much higher multiples.

14/ In the past year, Sterling’s stock has undergone a dramatic re-rating. At ~23x NTM EV/EBITDA, the stock now trades well above traditional contractor peers and approaching valuations typically reserved for specialty service providers like Quanta Services.

15/ Even if investors believe Sterling’s margins are sustainable, a re-rating in line with civil contractor peers implies 60% downside to its stock price alone. We see even further downside should Sterling’s margins normalize in line with industry peers.

16/ For added context, by our calculation, Sterling’s E-Infrastructure segment is trading at an implied valuation of nearly ~29x EV/EBITDA – which is a significant premium to $NVDA, and on par $VRT – a pure play data center infrastructure business with vastly superior EBITDA growth.

• • •

Missing some Tweet in this thread? You can try to

force a refresh