It is still early, but the energy market response to war in the Persian Gulf has been moderate with Brent oil up to $83/barrel. While much of the focus has been on oil markets, natural gas seems the bigger upside risk. 1/5

Some oil flows can be redirected if the Strait of Hormuz is closed. Countries like the US and China can draw down on strategic reserves, and China seems have significantly increased its reserves recently. More Russian barrels may be allowed to reach market. 2/5

LNG from Qatar (20% of global exports), on the other hand, cannot be easily redirected. The US is constrained by export capacity to further increase LNG exports. Closure of the strait or damage to Qatar LNG production could greatly reduce export volumes. 3/5

The US economy is likely somewhat insulated from events in the Gulf given constraints on natural gas export capacity, strategic reserves, and favorable terms of trade effect. 4/5

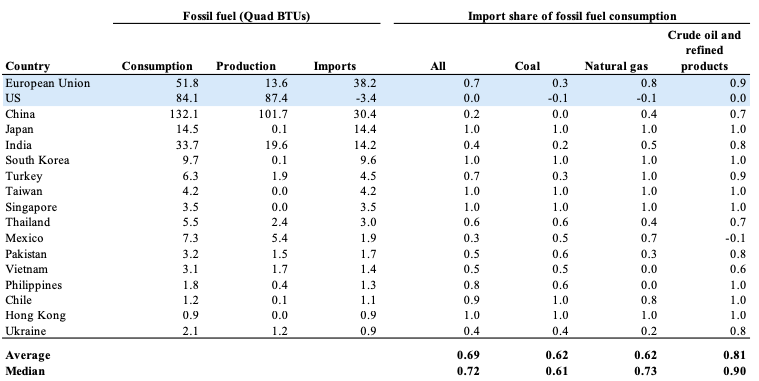

Most other countries are not. The table below shows the 15 largest fossil fuel importers and the US and EU for comparison. The median country imports 73% of its natural gas consumption and 90% of it oil and refined products consumption: 5/5

• • •

Missing some Tweet in this thread? You can try to

force a refresh