"AI is hiking your energy bill" is the most popular political talking point of 2026. The data doesn't support it. A thread:

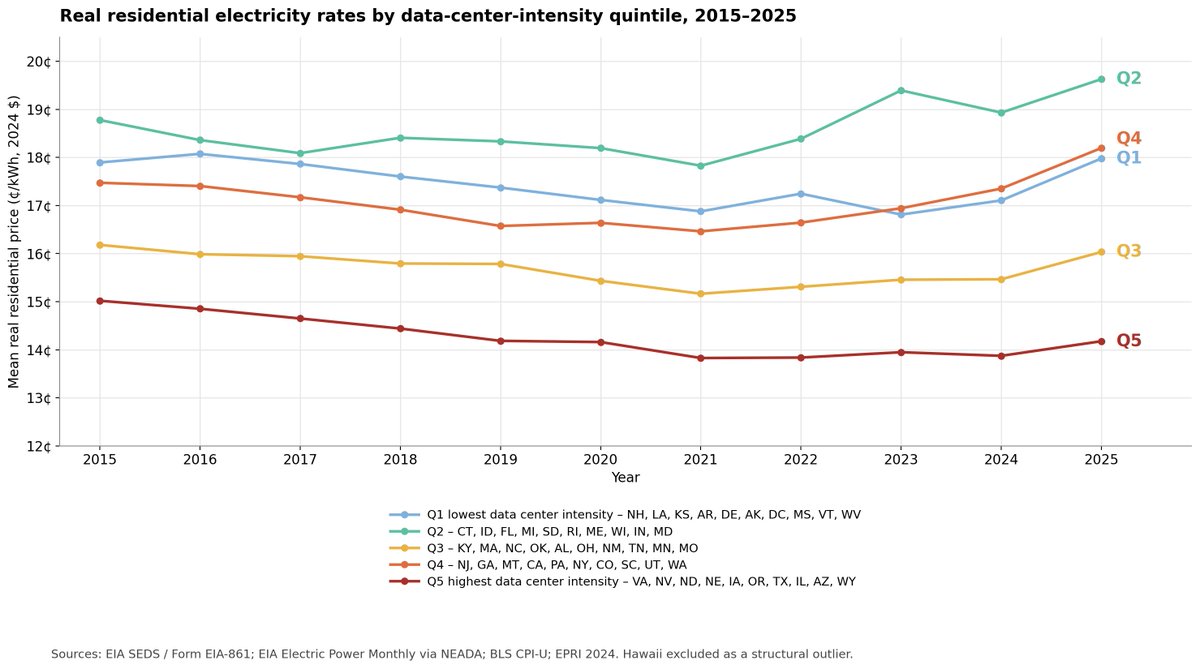

I sorted 50 states into data center intensity quintiles. States with the highest datacenter energy share (Q5) VA, TX, NV, IA, OR, AZ... collectively have the lowest and slowest rising mean residential energy prices

"but I live in one of those states and my bill went up" – in nominal dollars. in real terms, bills are down in the most datacenter-intense states.

it's inflation, not AI, which is driving up energy prices.

it's inflation, not AI, which is driving up energy prices.

Case study: Texas

ERCOT's large flexible load capacity went from ~1.2 GW (2018) to ~9.5 GW (2025) – a gargantuan AI + crypto buildout.

Real residential prices barely moved. Cheap natgas, huge solar/wind/battery additions, and behind-the-meter campuses absorbed almost all of it.

ERCOT's large flexible load capacity went from ~1.2 GW (2018) to ~9.5 GW (2025) – a gargantuan AI + crypto buildout.

Real residential prices barely moved. Cheap natgas, huge solar/wind/battery additions, and behind-the-meter campuses absorbed almost all of it.

Now zoom into the top 10 AI datacenter states.

Real rates ARE ticking up in 2025 – especially in PJM (OH, VA). That's where the buildout is finally starting to bite.

But the magnitude is small, and most of these states still sit well below the US average.

Real rates ARE ticking up in 2025 – especially in PJM (OH, VA). That's where the buildout is finally starting to bite.

But the magnitude is small, and most of these states still sit well below the US average.

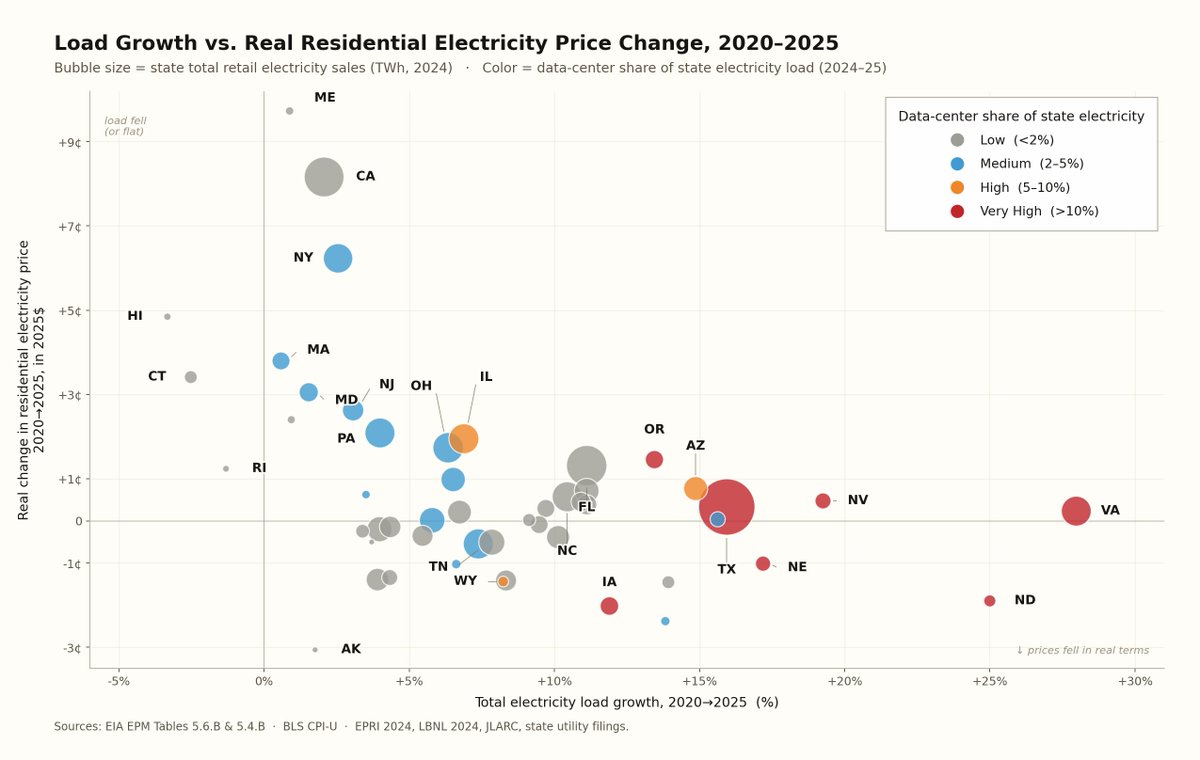

This is the single most important chart.

If AI were driving prices, you'd see a cluster top-right. You don't.

States with huge load growth (VA, TX, NV, ND, IA) sit at ~0c change in 5y. States with massive price hikes (CA, NY, MA, CT) have basically NO load growth.

If AI were driving prices, you'd see a cluster top-right. You don't.

States with huge load growth (VA, TX, NV, ND, IA) sit at ~0c change in 5y. States with massive price hikes (CA, NY, MA, CT) have basically NO load growth.

AI is also getting more efficient.

For a fixed unit of intelligence, energy per query has fallen ~200x in 3.5 years (conservative estimate)

Aggregate demand is still climbing, yes. (cc Jevons) But intelligence is getting cheaper faster than any commodity in modern history.

For a fixed unit of intelligence, energy per query has fallen ~200x in 3.5 years (conservative estimate)

Aggregate demand is still climbing, yes. (cc Jevons) But intelligence is getting cheaper faster than any commodity in modern history.

If not AI, then what?

Politics.

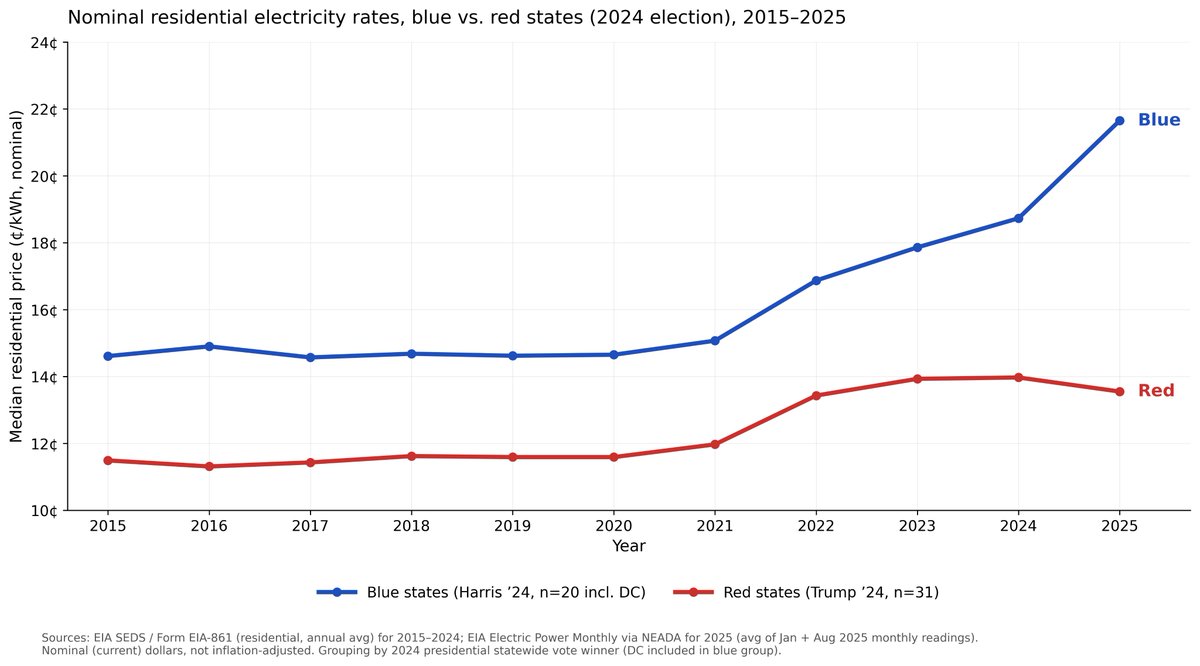

Blue states pay ~6c/kWh more than red states, and the gap is widening.

Denuclearization, blocked pipelines, rigid renewable mandates, NIMBYism, expensive union labor – these are stated policies, not market forces and not AI.

Politics.

Blue states pay ~6c/kWh more than red states, and the gap is widening.

Denuclearization, blocked pipelines, rigid renewable mandates, NIMBYism, expensive union labor – these are stated policies, not market forces and not AI.

States with lots of datacenters have cheap power, and datacenters go to cheap states.

Blue states have costly power because they are pursuing climate transitions, have NIMBY dynamics, and don't build pipelines & deprecate nuclear.

Blue states have costly power because they are pursuing climate transitions, have NIMBY dynamics, and don't build pipelines & deprecate nuclear.

Biggest real price hikes since 2019: CA, RI, DC, CT, ME, NY, MD, MA. All blue. All low data-center exposure.

Falling real prices: mostly red, many with heavy data centers.

AI isn't (yet) the villain. Policymakers complaining about AI might be.

Falling real prices: mostly red, many with heavy data centers.

AI isn't (yet) the villain. Policymakers complaining about AI might be.

Full writeup and complete methodological information for every chart available here:

murmurationstwo.substack.com/p/ai-is-not-hi…

murmurationstwo.substack.com/p/ai-is-not-hi…

• • •

Missing some Tweet in this thread? You can try to

force a refresh