UK inflation was down in April, but will soon surge to 5pc and beyond – which will have seismic economic and political consequences

The consumer price index (CPI) grew 2.8pc during the year to last month, down from 3.3pc in March.

“We have the right economic plan,” opined Rachel Reeves, as the figures were released last week. “To change course now would risk our economic stability”. If only that were true.

Last month’s headline inflation drop was a blip, driven by one-off price adjustments detached from economic realities. Those factors will soon be reversed.

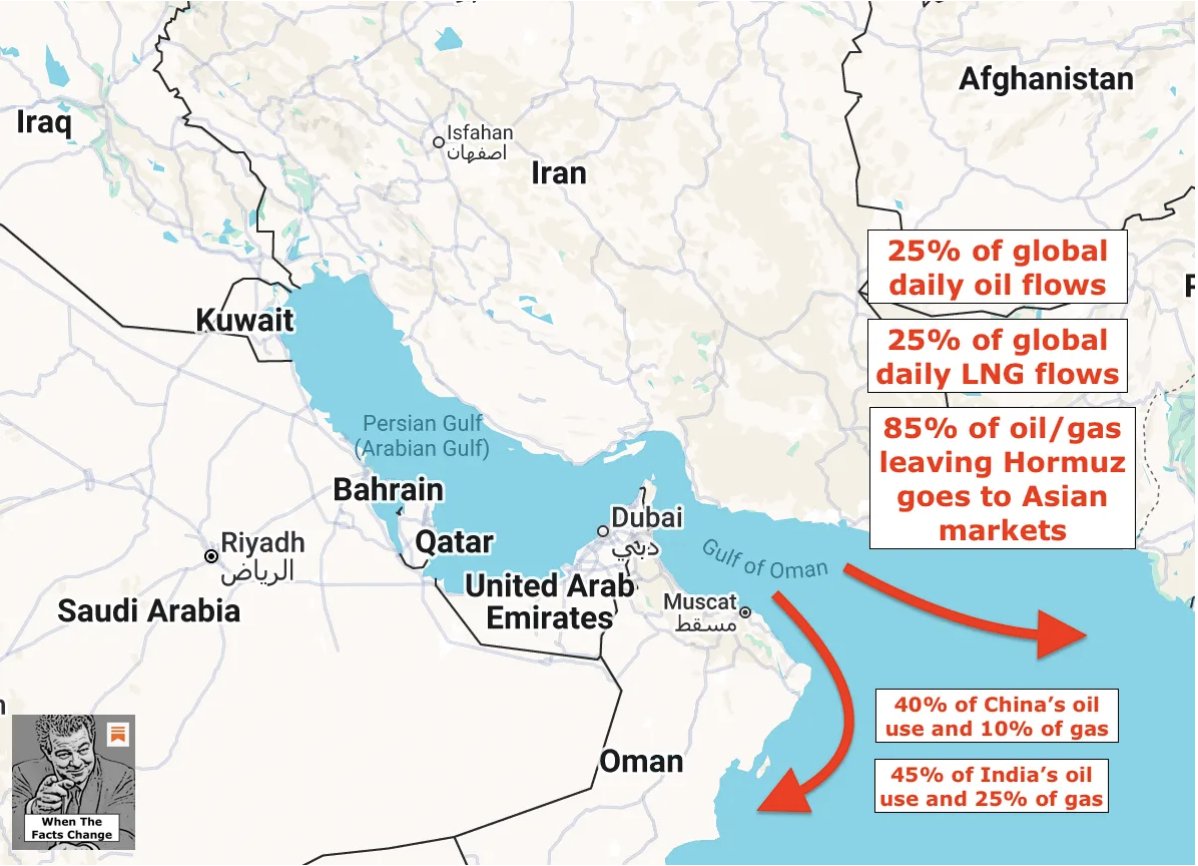

Growing price pressures will drive CPI inflation up over the coming months, in my view above 5pc. And if the Strait of Hormuz stays closed beyond the summer, blocking exports of oil, gas and fertiliser feedstocks from the Middle East, inflation could go much higher still.

My latest "Economic Agenda" column in @Telegraph

🧵1/6

telegraph.co.uk/business/2026/…

The consumer price index (CPI) grew 2.8pc during the year to last month, down from 3.3pc in March.

“We have the right economic plan,” opined Rachel Reeves, as the figures were released last week. “To change course now would risk our economic stability”. If only that were true.

Last month’s headline inflation drop was a blip, driven by one-off price adjustments detached from economic realities. Those factors will soon be reversed.

Growing price pressures will drive CPI inflation up over the coming months, in my view above 5pc. And if the Strait of Hormuz stays closed beyond the summer, blocking exports of oil, gas and fertiliser feedstocks from the Middle East, inflation could go much higher still.

My latest "Economic Agenda" column in @Telegraph

🧵1/6

telegraph.co.uk/business/2026/…

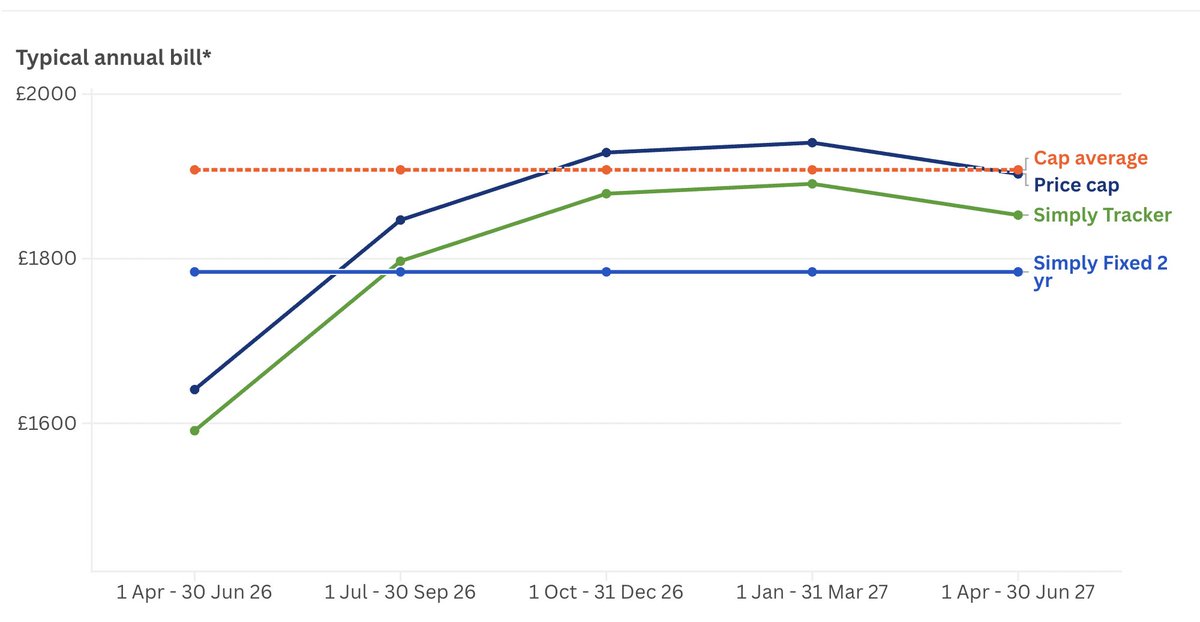

The April inflation dip to 2.8pc was partly due to a lowering of the Ofgem energy price cap – after the government shifted structural “green levies” and “policy costs” out of household bills and into general taxation.

The impact of that sneaky move will soon reverse, with the cap then reflecting recent surges in wholesale energy prices. Industry insiders point to a 12pc cap increase on 1st July, pushing typical household gas and electricity bills up almost £200 per year.

Last month’s inflation fallback was also caused by a particularly nasty “Awful April” in 2025 – with unusually sharp start-of-the-tax-year rises in council tax, broadband and mobile charges, TV licence and car tax and some other prices imposed by firms and the state. This year’s rises were still steep, but less so – lowering headline CPI.

Yet prices pressures are building, with an array of forecasters – from the Bank of England to the International Monetary Fund and countless City firms – all agreed that, despite this April number, UK inflation will soon significantly rise.

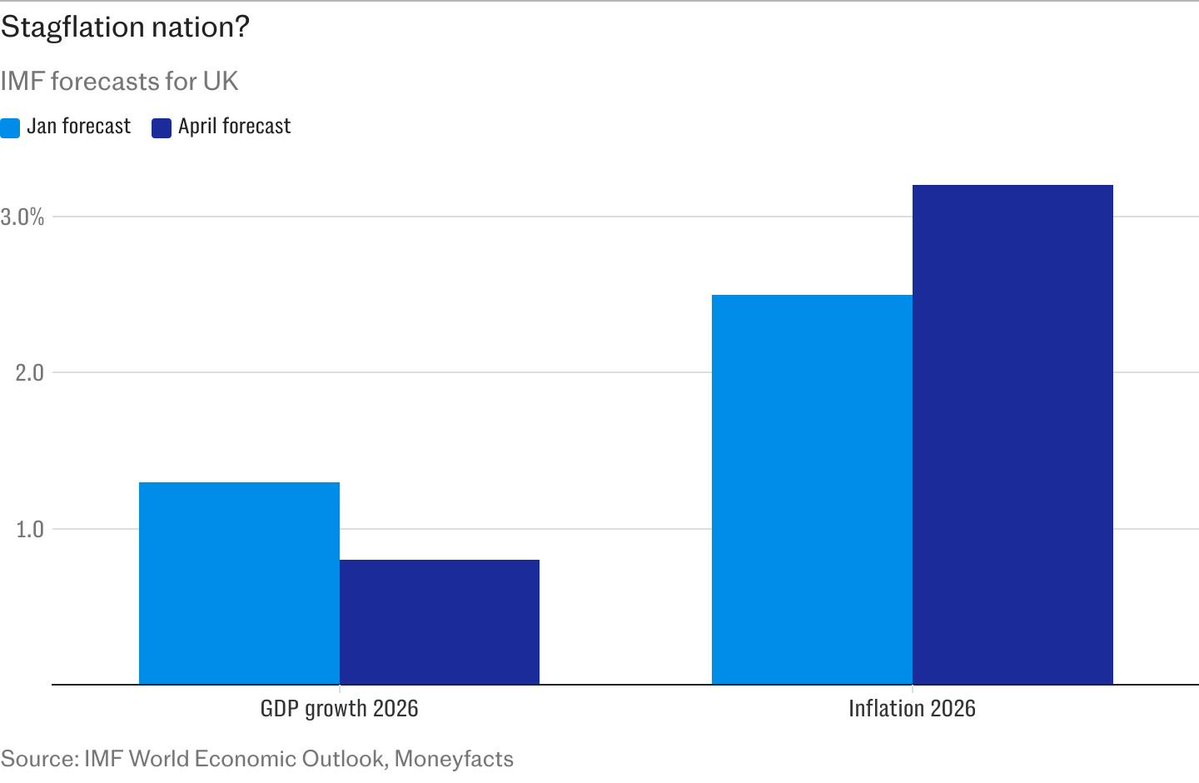

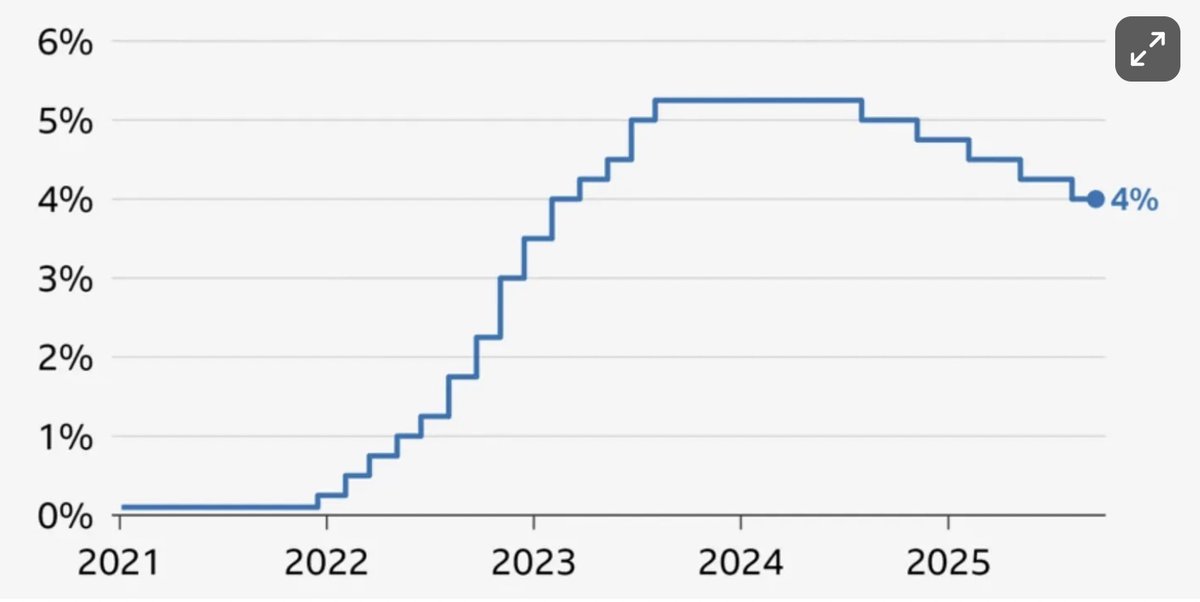

The IMF is looking at a 4pc peak, while the Bank of England, in its “worst-case scenario” of the US/Iran conflict intensifying, foresees 6pc inflation by early 2027. Under those circumstances, I’d say that’s too low.

🧵2/6

The impact of that sneaky move will soon reverse, with the cap then reflecting recent surges in wholesale energy prices. Industry insiders point to a 12pc cap increase on 1st July, pushing typical household gas and electricity bills up almost £200 per year.

Last month’s inflation fallback was also caused by a particularly nasty “Awful April” in 2025 – with unusually sharp start-of-the-tax-year rises in council tax, broadband and mobile charges, TV licence and car tax and some other prices imposed by firms and the state. This year’s rises were still steep, but less so – lowering headline CPI.

Yet prices pressures are building, with an array of forecasters – from the Bank of England to the International Monetary Fund and countless City firms – all agreed that, despite this April number, UK inflation will soon significantly rise.

The IMF is looking at a 4pc peak, while the Bank of England, in its “worst-case scenario” of the US/Iran conflict intensifying, foresees 6pc inflation by early 2027. Under those circumstances, I’d say that’s too low.

🧵2/6

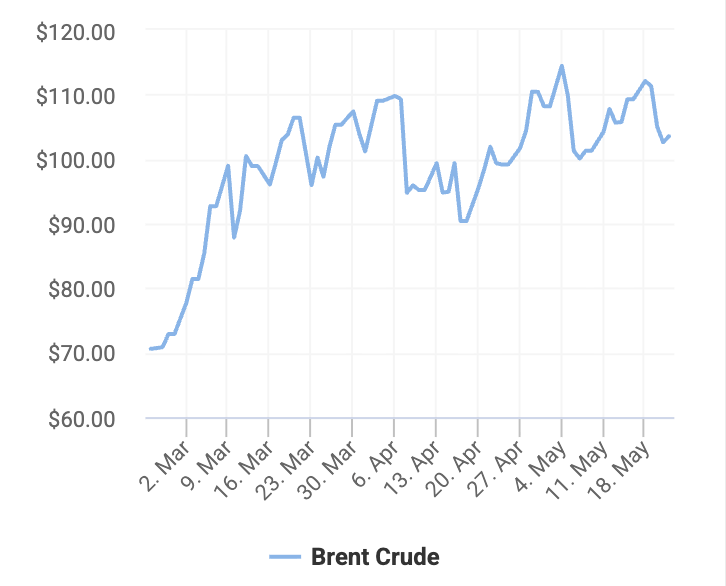

Oil prices have already ballooned from $70 a barrel in mid-February, before the escalation this Middle East conflict, to $107 now – more than 50pc up. But even if the US and Iran declared peace tomorrow, and the mouth of the Persian Gulf reopened, energy production and export facilities across the region have been seriously damaged.

During the last three months of war, US/Israeli strikes on Iran and Tehran’s counter-strikes have damaged infrastructure previously delivering 10-15pc of global oil and gas output – much of which will remain inoperable for months, in some cases years, to come. With global strategic petroleum reserves drained to a 40-year low, it strikes me energy prices will go much higher.

Already, UK petrol prices rose 17p on average last month to 159p per litre, with diesel soaring 30p to 191p – increases of 12pc and 18pc respectively. That’s caused a sharp 10pc drop in fuel sales, as motorists have cut back on travel. Expect more of this in the coming months, as high fuel prices slow GDP growth, while pushing headline inflation up.

🧵3/6

During the last three months of war, US/Israeli strikes on Iran and Tehran’s counter-strikes have damaged infrastructure previously delivering 10-15pc of global oil and gas output – much of which will remain inoperable for months, in some cases years, to come. With global strategic petroleum reserves drained to a 40-year low, it strikes me energy prices will go much higher.

Already, UK petrol prices rose 17p on average last month to 159p per litre, with diesel soaring 30p to 191p – increases of 12pc and 18pc respectively. That’s caused a sharp 10pc drop in fuel sales, as motorists have cut back on travel. Expect more of this in the coming months, as high fuel prices slow GDP growth, while pushing headline inflation up.

🧵3/6

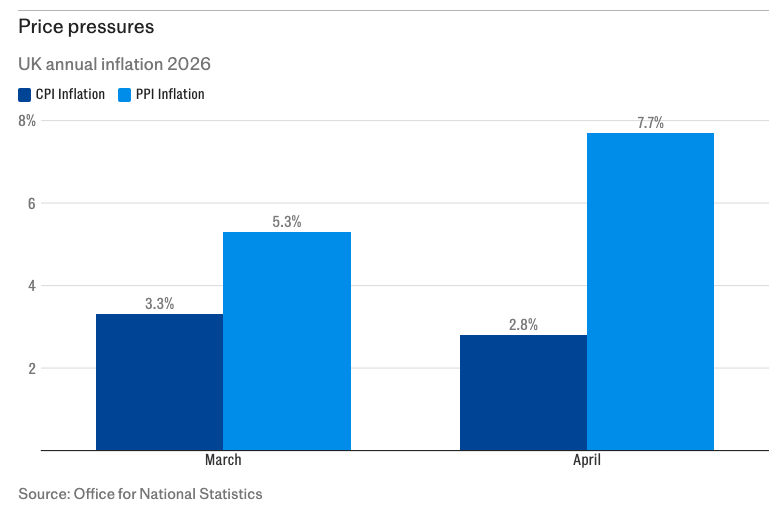

Rising fuel prices are also inflating costs across manufacturing, transport and the price of other raw materials. That’s why, while April saw the CPI measure fall, inflation as gauged by the Producer Price Index (PPI) rose from 5.3pc in March to no less than 7.7pc last month.

A leading indicator of where CPI inflation is going, PPI inflation points to significantly higher prices soon for ordinary shoppers.

While ministers can’t be blamed for Middle Eastern conflict, successive governments have left Britain vulnerable to soaring energy prices – given our lack of gas storage capacity and chronic dependence on energy imports.

But Labour’s decisions to tax North Sea oil and gas production even more than the Tories, and ban new North Sea drilling – in contrast to Norwegian and Danish operators – have made Britain’s energy crunch even worse.

Labour can also be blamed for the inflationary impact of the rise in firms’ hiring costs – not least the sharp increase in national insurance contributions and successive inflation-busting rises in the minimum wage, not least for younger workers.

🧵4/6

A leading indicator of where CPI inflation is going, PPI inflation points to significantly higher prices soon for ordinary shoppers.

While ministers can’t be blamed for Middle Eastern conflict, successive governments have left Britain vulnerable to soaring energy prices – given our lack of gas storage capacity and chronic dependence on energy imports.

But Labour’s decisions to tax North Sea oil and gas production even more than the Tories, and ban new North Sea drilling – in contrast to Norwegian and Danish operators – have made Britain’s energy crunch even worse.

Labour can also be blamed for the inflationary impact of the rise in firms’ hiring costs – not least the sharp increase in national insurance contributions and successive inflation-busting rises in the minimum wage, not least for younger workers.

🧵4/6

No wonder unemployment hit 5.5pc in March, up from 4.2pc when Labour took office in July 2024, with youth unemployment at an 11-year high.

And no wonder the Bank of England is now warning of “second-round effects” from higher wage costs and employment taxes. Struggling with increased overheads, firms are passing higher staff costs on to consumers, with workers demanding higher wages in turn.

We’re on the cusp of a 1970s-style “wage-price-spiral”, which would turbocharge UK inflation – and that is largely this government’s fault.

Britain’s cost-of-living crisis is unfortunately about to intensify, with food price inflation soaring to 8-10pc by the end of this year according to Food and Drink Federation, as the lagged impact of disruptions to energy and fertiliser supplies, as well as global shipping, hit worldwide markets.

That will do serious political damage, given that poorer households spend a higher share of their income on food, while trying to cope with increasingly expensive fuel.

And yet higher inflation also means that government borrowing costs will rise further, as Britain’s international creditors demand higher yields to lend, just as Labour’s increasingly indulgent leadership contest pushes the party further to the left.

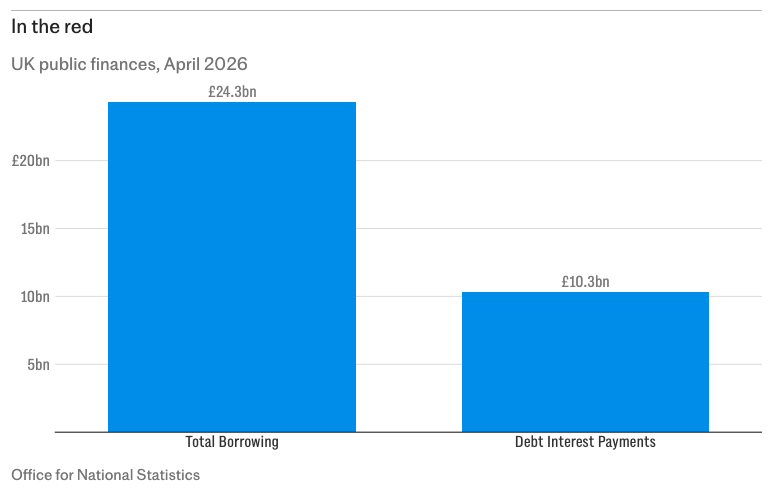

Yet the government already borrowed £24.3bn last month – the highest April borrowing figure ever, outside of the Covid pandemic.

That's equivalent to roughly half the entire amount of council tax collected across the UK during the last fiscal year – and, amidst runaway welfare spending, that's been put on tick, in a single month, adding to our already huge national debt.

Yet faced with increasing public discontent due to spiralling food and energy prices, Labour will find it even harder to borrow and spend over the coming months, in a bid to keep voters onside.

🧵5/6

And no wonder the Bank of England is now warning of “second-round effects” from higher wage costs and employment taxes. Struggling with increased overheads, firms are passing higher staff costs on to consumers, with workers demanding higher wages in turn.

We’re on the cusp of a 1970s-style “wage-price-spiral”, which would turbocharge UK inflation – and that is largely this government’s fault.

Britain’s cost-of-living crisis is unfortunately about to intensify, with food price inflation soaring to 8-10pc by the end of this year according to Food and Drink Federation, as the lagged impact of disruptions to energy and fertiliser supplies, as well as global shipping, hit worldwide markets.

That will do serious political damage, given that poorer households spend a higher share of their income on food, while trying to cope with increasingly expensive fuel.

And yet higher inflation also means that government borrowing costs will rise further, as Britain’s international creditors demand higher yields to lend, just as Labour’s increasingly indulgent leadership contest pushes the party further to the left.

Yet the government already borrowed £24.3bn last month – the highest April borrowing figure ever, outside of the Covid pandemic.

That's equivalent to roughly half the entire amount of council tax collected across the UK during the last fiscal year – and, amidst runaway welfare spending, that's been put on tick, in a single month, adding to our already huge national debt.

Yet faced with increasing public discontent due to spiralling food and energy prices, Labour will find it even harder to borrow and spend over the coming months, in a bid to keep voters onside.

🧵5/6

When Labour took office, headline inflation was 2pc. That same figure has since averaged 3.1pc, compared to 2.7pc in the US over the same period, 2.2pc in Germany and 1.9pc in France.

“We promised to cut inflation – and we have”, said Reeves last week. That statement is arrant nonsense, despite last month's one-off inflation fall – as will soon become painfully clear.

🧵6/6

telegraph.co.uk/business/2026/…

“We promised to cut inflation – and we have”, said Reeves last week. That statement is arrant nonsense, despite last month's one-off inflation fall – as will soon become painfully clear.

🧵6/6

telegraph.co.uk/business/2026/…

• • •

Missing some Tweet in this thread? You can try to

force a refresh