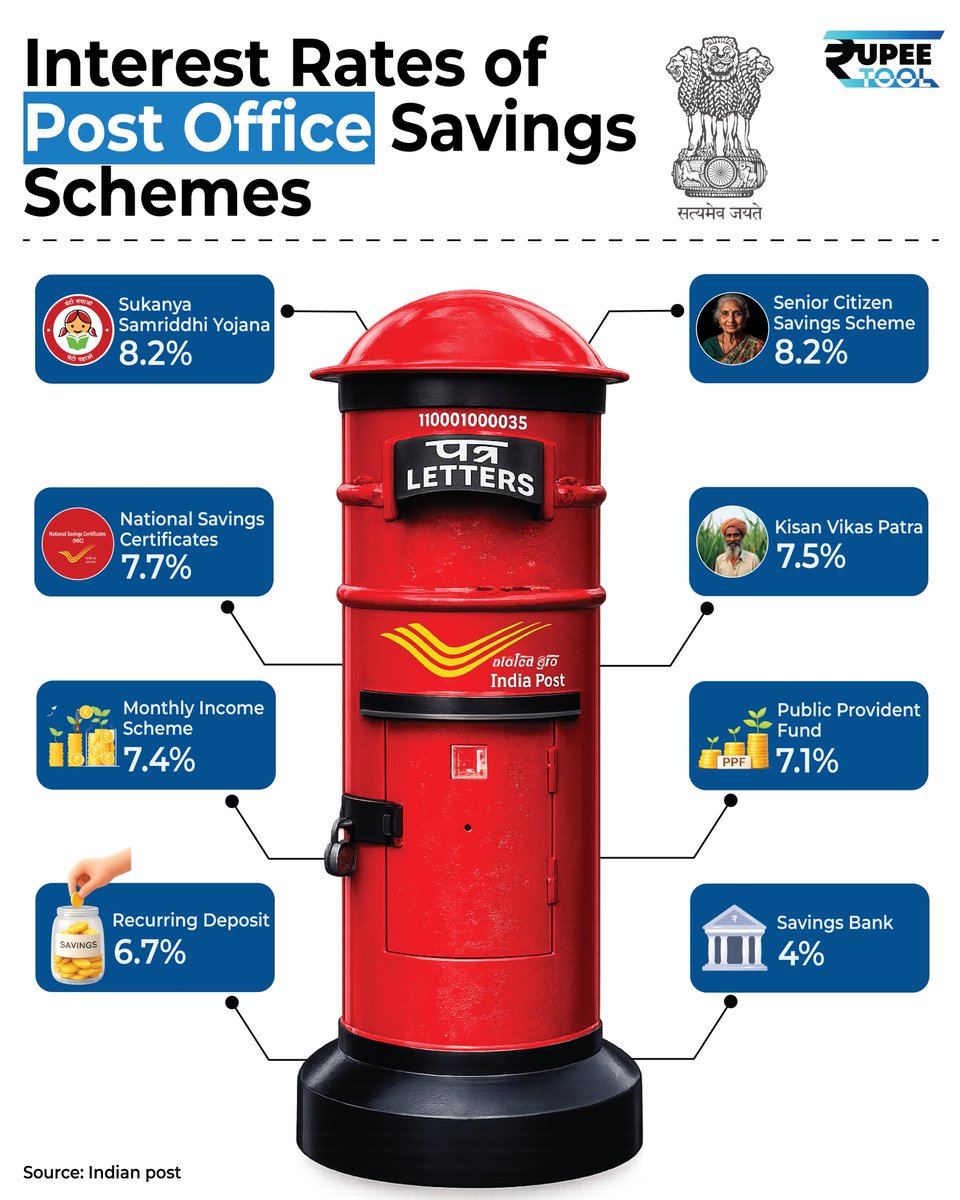

8.2%. That is what a Post Office scheme pays you today, fully government-backed.

Nifty 50, last 12 months: -5.4%.

Most Indians do not know there are 8 such schemes.

Here are all of them. 🧵👇

Nifty 50, last 12 months: -5.4%.

Most Indians do not know there are 8 such schemes.

Here are all of them. 🧵👇

[1] The basics

🔸 Small savings schemes are set by the Finance Ministry

🔸 Reviewed every quarter (Jan, Apr, Jul, Oct)

🔸 Backed by the Government of India

🔸 Current rates have stayed unchanged for 8 straight quarters

🔸 Latest reset: April-June 2026

🔸 Small savings schemes are set by the Finance Ministry

🔸 Reviewed every quarter (Jan, Apr, Jul, Oct)

🔸 Backed by the Government of India

🔸 Current rates have stayed unchanged for 8 straight quarters

🔸 Latest reset: April-June 2026

[2] Sukanya Samriddhi Yojana: 8.2%

For a daughter under 10 years.

🔸 Min: ₹250/year. Max: ₹1.5 lakh/year

🔸 Deposits for 15 years

🔸 Matures when she turns 21

🔸 Tax-free interest and 80C deduction (EEE)

The highest rate in this list, locked for your daughter's future.

For a daughter under 10 years.

🔸 Min: ₹250/year. Max: ₹1.5 lakh/year

🔸 Deposits for 15 years

🔸 Matures when she turns 21

🔸 Tax-free interest and 80C deduction (EEE)

The highest rate in this list, locked for your daughter's future.

[3] Senior Citizen Savings Scheme: 8.2%

For Indians 60+, or 55+ if retired/VRS.

🔸 Max: ₹30 lakh per individual

🔸 5 years, extendable by 3

🔸 Interest paid every quarter

🔸 80C deduction available

🔸 Interest taxable at slab

Highest-rate retirement income scheme.

For Indians 60+, or 55+ if retired/VRS.

🔸 Max: ₹30 lakh per individual

🔸 5 years, extendable by 3

🔸 Interest paid every quarter

🔸 80C deduction available

🔸 Interest taxable at slab

Highest-rate retirement income scheme.

[4] National Savings Certificate: 7.7%

A 5-year FD alternative.

🔸 Min ₹1,000. No maximum

🔸 Interest compounds annually, paid at maturity

🔸 80C on the principal

🔸 Reinvested interest also gets 80C

🔸 Interest taxable at exit

Best for a 5-yr lock-in with tax shelter.

A 5-year FD alternative.

🔸 Min ₹1,000. No maximum

🔸 Interest compounds annually, paid at maturity

🔸 80C on the principal

🔸 Reinvested interest also gets 80C

🔸 Interest taxable at exit

Best for a 5-yr lock-in with tax shelter.

[5] Kisan Vikas Patra: 7.5%

The "doubles your money" scheme.

🔸 Min: ₹1,000. No maximum

🔸 Maturity: 115 months (~9 years 7 months) at current rate

🔸 No 80C benefit

🔸 Interest fully taxable

🔸 Transferable

Simple, but the post-tax return is modest.

The "doubles your money" scheme.

🔸 Min: ₹1,000. No maximum

🔸 Maturity: 115 months (~9 years 7 months) at current rate

🔸 No 80C benefit

🔸 Interest fully taxable

🔸 Transferable

Simple, but the post-tax return is modest.

[6] Monthly Income Scheme: 7.4%

For a steady monthly cheque.

🔸 Tenure: 5 years

🔸 Max: ₹9L single / ₹15L joint

🔸 Interest paid monthly into savings account

🔸 No 80C benefit

🔸 Interest taxable

A low-risk income layer in retirement.

For a steady monthly cheque.

🔸 Tenure: 5 years

🔸 Max: ₹9L single / ₹15L joint

🔸 Interest paid monthly into savings account

🔸 No 80C benefit

🔸 Interest taxable

A low-risk income layer in retirement.

[7] Public Provident Fund: 7.1%

The long-term workhorse.

🔸 Tenure: 15 years (extendable in 5-yr blocks)

🔸 Max: ₹1.5 lakh/year

🔸 Interest tax-free

🔸 Principal qualifies for 80C

🔸 Maturity tax-free (full EEE)

Lower headline rate, highest post-tax effectiveness.

The long-term workhorse.

🔸 Tenure: 15 years (extendable in 5-yr blocks)

🔸 Max: ₹1.5 lakh/year

🔸 Interest tax-free

🔸 Principal qualifies for 80C

🔸 Maturity tax-free (full EEE)

Lower headline rate, highest post-tax effectiveness.

[8] Recurring Deposit: 6.7%

Small monthly habit.

🔸 Tenure: 5 years

🔸 Min: ₹100/month

🔸 Interest compounded quarterly

🔸 No 80C benefit

🔸 Interest taxable

Best for first-time savers building a discipline.

Small monthly habit.

🔸 Tenure: 5 years

🔸 Min: ₹100/month

🔸 Interest compounded quarterly

🔸 No 80C benefit

🔸 Interest taxable

Best for first-time savers building a discipline.

[9] Savings Bank Account: 4%

The default Post Office account.

🔸 Min balance: ₹500

🔸 Use for parking small balances

🔸 Up to ₹10,000 interest is tax-deductible under 80TTA

🔸 Not a wealth-building tool

Use for liquidity, not returns.

The default Post Office account.

🔸 Min balance: ₹500

🔸 Use for parking small balances

🔸 Up to ₹10,000 interest is tax-deductible under 80TTA

🔸 Not a wealth-building tool

Use for liquidity, not returns.

[10] Which one for which goal?

🔸 Daughter's future: SSY

🔸 Retirement income: SCSS + MIS

🔸 Long-term wealth + tax: PPF

🔸 5-year tax-saver: NSC

🔸 Lump-sum doubling: KVP

🔸 Monthly habit: RD

🔸 Liquidity: Savings Account

🔸 Daughter's future: SSY

🔸 Retirement income: SCSS + MIS

🔸 Long-term wealth + tax: PPF

🔸 5-year tax-saver: NSC

🔸 Lump-sum doubling: KVP

🔸 Monthly habit: RD

🔸 Liquidity: Savings Account

[11] We are also on Substack

For long-form deep-dives on Indian markets, tax and finance.

rupeetoolbyfgm.substack.com

For long-form deep-dives on Indian markets, tax and finance.

rupeetoolbyfgm.substack.com

If this thread helped you:

RT the first tweet to share it

Follow @RupeetoolByFGM for more finance breakdowns

RT the first tweet to share it

Follow @RupeetoolByFGM for more finance breakdowns

https://x.com/RupeetoolByFGM/status/2063228631472808255?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh