India has 7,500 km of coastline and 1.4 billion people.

Yet until 2021, you couldn't take an overnight ocean cruise without flying to Singapore or the Mediterranean first.

One company spotted that void. Built a near-monopoly inside it. And is now asking the public markets to fund what comes next.

A thread on Waterways Leisure Tourism (Cordelia Cruises) IPO 🧵

Yet until 2021, you couldn't take an overnight ocean cruise without flying to Singapore or the Mediterranean first.

One company spotted that void. Built a near-monopoly inside it. And is now asking the public markets to fund what comes next.

A thread on Waterways Leisure Tourism (Cordelia Cruises) IPO 🧵

The company didn't start from scratch. It started from someone else's wreckage.

In 2018, the Essel Group (Subhash Chandra) launched Jalesh Cruises with great fanfare. The ship was named Karnika, after a mythological apsara.

By November 2020, Karnika was sailing to Alang's shipbreaking yards.

COVID + Essel Group's broader financial collapse = complete implosion.

In 2018, the Essel Group (Subhash Chandra) launched Jalesh Cruises with great fanfare. The ship was named Karnika, after a mythological apsara.

By November 2020, Karnika was sailing to Alang's shipbreaking yards.

COVID + Essel Group's broader financial collapse = complete implosion.

Here's where it gets interesting.

Waterways Leisure acquired Jalesh's brand, IP, and trade relationships from Zen Cruises for a consideration of Rs 100.

Not Rs 100 crore. Not Rs 100 lakh.

Rs. 100.

They left the distressed vessel and its liabilities behind. Took only the intangible assets.

Waterways Leisure acquired Jalesh's brand, IP, and trade relationships from Zen Cruises for a consideration of Rs 100.

Not Rs 100 crore. Not Rs 100 lakh.

Rs. 100.

They left the distressed vessel and its liabilities behind. Took only the intangible assets.

They then poached Jurgen Bailom, the former President & CEO of Jalesh Cruises, who had prior experience with Royal Caribbean brands.

Bought a secondhand 1990-built vessel (Empress of the Seas) from Royal Caribbean itself. (FYI, Royal Caribbean is top 3 global cruise lines)

Refitted it. Rebranded it as MV Empress.

First commercial sailing: Mumbai, September 2021.

Dead category → revived in under 12 months.

Bought a secondhand 1990-built vessel (Empress of the Seas) from Royal Caribbean itself. (FYI, Royal Caribbean is top 3 global cruise lines)

Refitted it. Rebranded it as MV Empress.

First commercial sailing: Mumbai, September 2021.

Dead category → revived in under 12 months.

Today, Cordelia commands ~79% market share by value in India's domestic overnight ocean cruise market.

Market share optically looks higher due to tiny market in India.

There is no listed peer on BSE or NSE. None.

Market share optically looks higher due to tiny market in India.

There is no listed peer on BSE or NSE. None.

Single ship (Cordilla). 2,005 passenger capacity.

FY26 numbers:

→ Revenue: Rs 579 Cr

→ EBITDA: Rs 117 Cr (20% margin)

→ PAT: Rs 52 Cr

→ Passenger Load Factor: 85%

→ Revenue per passenger per day: Rs 12,036

85% occupancy on a single vessel consistently is genuinely impressive.

FY26 numbers:

→ Revenue: Rs 579 Cr

→ EBITDA: Rs 117 Cr (20% margin)

→ PAT: Rs 52 Cr

→ Passenger Load Factor: 85%

→ Revenue per passenger per day: Rs 12,036

85% occupancy on a single vessel consistently is genuinely impressive.

Onboard spend (casino, spa, specialty dining, excursions) = only 8.7% of Cordelia's revenue.

For Royal Caribbean and Carnival, that number is 25-30%.

Why does this matter?

The Indian consumer today treats a cruise like an all-inclusive package, extract maximum value from the base ticket, spend nothing extra onboard. That's a cultural habit, not a permanent ceiling.

If company is able to figure out a way to shift this habit, through loyalty programs, dynamic pricing of premium experiences, better retail curation, that incremental revenue carries almost zero additional fixed cost.

It flows straight to the bottom line.

The base business at 20% EBITDA is decent. The optionality sitting inside that 8.7% onboard number could be the real story.

For Royal Caribbean and Carnival, that number is 25-30%.

Why does this matter?

The Indian consumer today treats a cruise like an all-inclusive package, extract maximum value from the base ticket, spend nothing extra onboard. That's a cultural habit, not a permanent ceiling.

If company is able to figure out a way to shift this habit, through loyalty programs, dynamic pricing of premium experiences, better retail curation, that incremental revenue carries almost zero additional fixed cost.

It flows straight to the bottom line.

The base business at 20% EBITDA is decent. The optionality sitting inside that 8.7% onboard number could be the real story.

Before you look at FY25's Rs 168 Cr PAT and 36% EBITDA margin and get excited, read this.

That was not operational excellence.

The company restructured its lease agreements and shifted vessel ownership to a new GIFT City subsidiary. This triggered a one-time derecognition of lease liabilities under Ind AS 116 — a Rs 75.58 Cr exceptional gain.

Accounting artifact. Not cash.

That was not operational excellence.

The company restructured its lease agreements and shifted vessel ownership to a new GIFT City subsidiary. This triggered a one-time derecognition of lease liabilities under Ind AS 116 — a Rs 75.58 Cr exceptional gain.

Accounting artifact. Not cash.

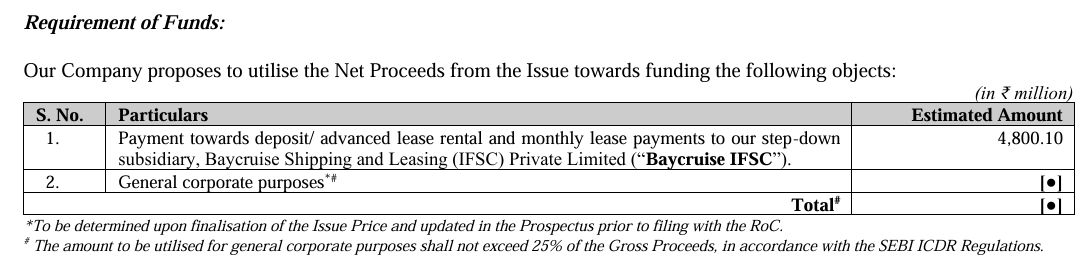

Rs 585 Crore. 100% fresh issue. Zero OFS.

No promoter is selling a single share.

Rs 480 Cr of the IPO proceeds fund advance deposits and lease rentals for the Norwegian Sky and Norwegian Sun.

Not acquisition. Not ownership. Rent on ships the company will never own.

No promoter is selling a single share.

Rs 480 Cr of the IPO proceeds fund advance deposits and lease rentals for the Norwegian Sky and Norwegian Sun.

Not acquisition. Not ownership. Rent on ships the company will never own.

Let's be precise about what investors are actually funding here.

MV Empress (currently operating): 2,005 passengers

Norwegian Sky (Sept 2026): 2,004 passengers

Norwegian Sun (Nov 2027): 1,936 passengers

Total eventual capacity: ~6,000 passengers simultaneously.

From 1 ship to 3 ships in 24 months. That's a 200% capacity jump in an unproven, nascent market.

This IPO is asking investors to fund that leap of faith/uncertainty.

MV Empress (currently operating): 2,005 passengers

Norwegian Sky (Sept 2026): 2,004 passengers

Norwegian Sun (Nov 2027): 1,936 passengers

Total eventual capacity: ~6,000 passengers simultaneously.

From 1 ship to 3 ships in 24 months. That's a 200% capacity jump in an unproven, nascent market.

This IPO is asking investors to fund that leap of faith/uncertainty.

The Norwegian vessels come on time charter at $16.16 million per ship per year for the first two years.

That's Rs ~154 Cr annually, per ship, in fixed USD-denominated outflows.

When both ships are operating, the company will owe over Rs 300 Cr a year in lease rentals alone.

At current margins, MV Empress generates ~Rs 115 Cr EBITDA annually.

Do that math slowly.

That's Rs ~154 Cr annually, per ship, in fixed USD-denominated outflows.

When both ships are operating, the company will owe over Rs 300 Cr a year in lease rentals alone.

At current margins, MV Empress generates ~Rs 115 Cr EBITDA annually.

Do that math slowly.

Until September 2026, the entire business sits on just one ship only.

One 36-year-old hull.

A single mechanical breakdown, a dry-docking requirement, a maritime incident and cash flows go to zero while lease costs, crew costs, and port fees keep running.

There is no backup. No redundancy.

This is the most uncomfortable single-point-of-failure in this company.

One 36-year-old hull.

A single mechanical breakdown, a dry-docking requirement, a maritime incident and cash flows go to zero while lease costs, crew costs, and port fees keep running.

There is no backup. No redundancy.

This is the most uncomfortable single-point-of-failure in this company.

The statutory auditors raised three flags worth noting:

Audit trail (edit log) at the database level of their SAP accounting system was not enabled, a compliance gap under the Companies (Audit & Auditors) Rules, 2014.

Inventory (food, fuel) managed by third-party vendors could not be physically verified.

None of these are deal-breakers. But they are items that deserve weight in your analysis.

Audit trail (edit log) at the database level of their SAP accounting system was not enabled, a compliance gap under the Companies (Audit & Auditors) Rules, 2014.

Inventory (food, fuel) managed by third-party vendors could not be physically verified.

None of these are deal-breakers. But they are items that deserve weight in your analysis.

The RHP compares Cordelia to Chalet Hotels (44% EBITDA margin) and Lemon Tree Hotels (48% EBITDA margin).

This comparison flatters no one. Hotels own appreciating real estate. Cruise ships are depreciating assets in corrosive saltwater requiring mandatory multi-crore dry-docking every few years.

Valuing a maritime operator at hospitality P/E multiples of 40x+ would be a category error.

The more honest comp is global cruise operators — who run on thin net margins at massive scale.

This comparison flatters no one. Hotels own appreciating real estate. Cruise ships are depreciating assets in corrosive saltwater requiring mandatory multi-crore dry-docking every few years.

Valuing a maritime operator at hospitality P/E multiples of 40x+ would be a category error.

The more honest comp is global cruise operators — who run on thin net margins at massive scale.

One underappreciated variable: the Cruise Bharat Mission.

Launched in late 2024, it's a structured three-phase government initiative to make India a global cruise hub by 2029.

Phase 1: Feasibility studies and port planning.

Phase 2: Physical terminal development, new coastal destinations unlocked.

Phase 3: Full domestic + international cruise integration.

Cordelia is the only domestic operator positioned to absorb this infrastructure build. Public policy is effectively subsidizing their market creation efforts.

Launched in late 2024, it's a structured three-phase government initiative to make India a global cruise hub by 2029.

Phase 1: Feasibility studies and port planning.

Phase 2: Physical terminal development, new coastal destinations unlocked.

Phase 3: Full domestic + international cruise integration.

Cordelia is the only domestic operator positioned to absorb this infrastructure build. Public policy is effectively subsidizing their market creation efforts.

This IPO is not a comfortable compounder. It's a high-conviction, high-risk capacity expansion play.

The bull case: Indian discretionary spending expands, cruise culture takes root, 85%+ load factors hold across three ships, and onboard spending habits mature. The operational leverage is extraordinary.

The bear case: Market can't absorb 6,000 passenger berths in 24 months. USD lease costs compound. A single bad incident, operational or reputational with no backup ship destroys an entire sailing season's cash flows.

The bull case: Indian discretionary spending expands, cruise culture takes root, 85%+ load factors hold across three ships, and onboard spending habits mature. The operational leverage is extraordinary.

The bear case: Market can't absorb 6,000 passenger berths in 24 months. USD lease costs compound. A single bad incident, operational or reputational with no backup ship destroys an entire sailing season's cash flows.

Cordelia didn't create a product. It created a category in India.

That's genuinely worth applauding for. And the management DNA, resurrecting a dead brand, acquiring an asset from Royal Caribbean, achieving 85% occupancy in a country with zero cruise culture, deserves serious credit.

But the IPO is asking you to fund a tripling of capacity in a market that's still learning what a cruise is.

The ocean is wide. The question is whether India is ready to fill it.

That's genuinely worth applauding for. And the management DNA, resurrecting a dead brand, acquiring an asset from Royal Caribbean, achieving 85% occupancy in a country with zero cruise culture, deserves serious credit.

But the IPO is asking you to fund a tripling of capacity in a market that's still learning what a cruise is.

The ocean is wide. The question is whether India is ready to fill it.

SEBI EoDI Disclosure (effective 1 May 2026)

We are SEBI Registered Research Analyst (INH000023199). BSE Enlistment No. 6747

Content shared on this handle is for informational and educational purposes only and does not constitute personalized investment advice, recommendation, or solicitation to buy or sell any security. Investments in securities markets are subject to market risks. Please read all related documents carefully before investing. Not Invested!

We are SEBI Registered Research Analyst (INH000023199). BSE Enlistment No. 6747

Content shared on this handle is for informational and educational purposes only and does not constitute personalized investment advice, recommendation, or solicitation to buy or sell any security. Investments in securities markets are subject to market risks. Please read all related documents carefully before investing. Not Invested!

• • •

Missing some Tweet in this thread? You can try to

force a refresh